Immediate Annuity Rates

(What do you get for your money?)

These days someone retiring at 65 can expect to live about 20 years. In fact, about a third of retirees can expect to live to age 90. Unfortunately, fewer people have traditional pensions that pay an income every year. Buying an immediate annuity is like buying a pension for yourself. How much income do you get for your money? That depends on the immediate annuity rate.

You can click here to use an independent agent matching tool to find the best insurance solution in your area. Provide a few details about what you're looking for, and the tool will recommend the best agents for you. Any information you provide will only be sent to the agent you pick.

What Is an Immediate Annuity?

Immediate annuities are also known as income annuities. That's because the insurance company begins to pay an income immediately after receiving a purchase payment, or premium. Immediate annuities have several options for income:

Life only - A payment is guaranteed for the lifetime of the annuitant. No payments are made after the annuitant's death. Life only options will pay out a higher monthly or annual income than the other options. Joint and survivor life only is available for the longer of two lives, usually spouses.

Life and period certain - A payment is guaranteed for the lifetime of the annuitant. The payments are made for at least a "certain" number of years, regardless of when the annuitant dies. The certain year options are usually 10 and 20. Joint and survivor options are available for life and period certain.

Fixed period - Payments are made for a specified number of years, regardless of when the annuitant dies.

Insurance companies calculate the payout for life and life and period certain using an annuity rate. Fixed period payouts are based strictly on interest rates.

Immediate Annuity Rates

Immediate annuity rates for each income option are calculated from the age and gender of the annuitant, based on an interest rate the insurance company chooses. The interest rate changes frequently with market conditions. That means immediate annuity rates change frequently.

The longer the insurance company predicts that you will live, the lower the payout.

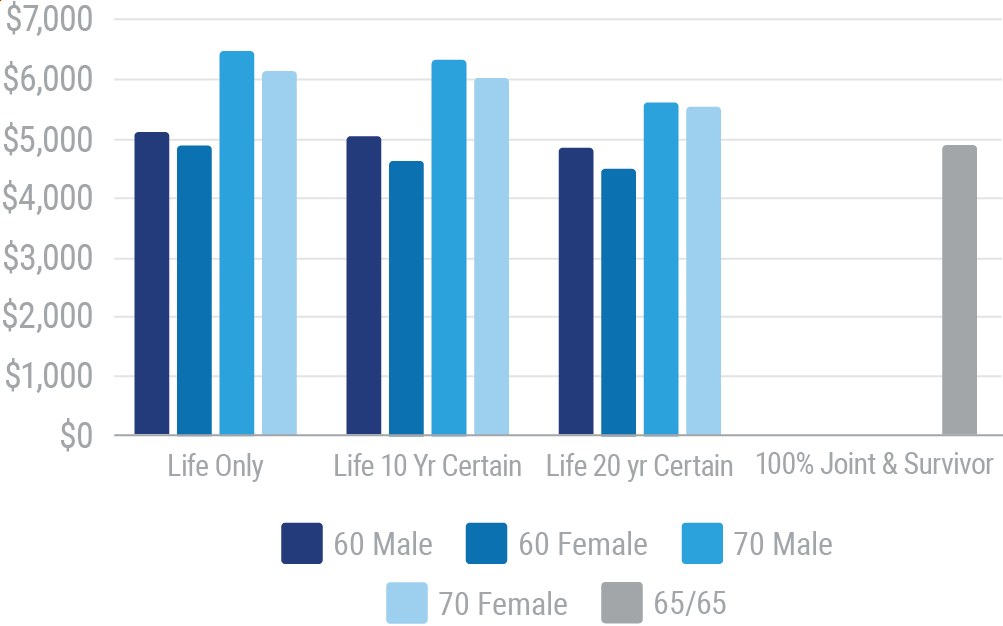

The chart below compares immediate annuity payouts at different ages for a $100,000 purchase payment.

Immediate Annuity Annual Payouts at Selected Ages | $100,000 Purchase Payment

The life only option is always the highest rate.

How To Compare Immediate Annuity Rates

Sounds simple, doesn't it? Get the quote and compare the rate. The highest one wins. All true, but consider this. The insurance company is going to be paying you for a long time. The guarantees are only as good as the financial strength of the insurance company. That's why it’s important to buy an immediate annuity from a highly rated company.

Financial strength ratings are available from A.M. Best, S&P, Moody’s, and Fitch.

Get Annuities from the Experts

Our independent agents shop around to find you the best coverage.

Immediate Annuity Rates of Return

Immediate annuities are different from other investments because you are exchanging principal for income. Once the income begins, you generally have no access to the money. On the other hand, the income is higher than you would receive on other "low-risk" investments.

Here's why. Insurance companies know that a certain percentage of annuitants will die before their life expectancy. A portion of that money, called mortality credits, is used to fund higher payouts for everyone else. In the earlier example, a $100,000 premium created $5,120 of income per year for a 60-year-old male. While the rate of income is 5.12%, the actual rate of return is considerably lower. Assuming the 60-year-old received payments for 25 years, the rate of return is 2.0%. If he lives to 95 ,the rate of return is 3.7%.

The Pros of Immediate Annuities

These days fewer people have traditional pensions that pay an income every year for life. Buying an income annuity is like buying a pension for yourself. Income annuities can also help you plan for a lifetime income for two people. Joint and survivor life expectancy can be much longer than for each individual.

Immediate annuities produce a higher income than you would get for a similar low-risk investment. A portion of the income is excluded from taxes because it is considered principal.

Finally, as people get older, it becomes more difficult to manage day-to-day finances. Immediate annuities offer a predictable long-term alternative that doesn't require hands-on attention.

The Cons of Immediate Annuities

When you purchase an immediate, or income, annuity you give up access to the principal. In doing so, you give up the opportunity for other investments in the future. Here's why that can be a problem. Interest and inflation rates change. In January 2000 you could get a 6-month CD at 6.15%. Today? A 6-month CD pays 0.60%. In 1980 inflation was running at 12%, today it is 2%. The point is that income annuities are long-term arrangements. Changes in the economic environment can make them more or less effective.

While fixed income annuities do produce a higher rate of income, it takes a long time to get your principal back. In the chart above, the 60-year-old female is 82 before she recaptures her original $100,000.

What Next?

Immediate annuities can be an important part of your retirement plan. While they have many features and benefits, they are not for everyone. Talk to an independent insurance agent. They can help you decide if an immediate annuity is right for you.

Annuityratewatch.com

St louis fed 6 month cd secondary market