Your quote is based on several common factors to give you a clear picture of the cost you can expect for condo insurance, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

Condo insurance is designed to cover the inside of your unit, including the walls, against numerous threats, including fire damage, vandalism, and more. Condo insurance coverage can reimburse for repairs or replacements to your personal property, like clothing if it gets stolen, damaged, lost, or destroyed. Some of your unit's built-in components, such as the flooring and cabinets, are protected against damage and destruction as well. Getting the right condo insurance policy starts with obtaining a condo insurance quote, and an independent insurance agent can help you with that. Having condo insurance can help protect you against having to pay for costs of damage or destruction to your condo out of your own pocket.

What Is Condo Insurance?

Condo insurance is essentially an agreement between the condo owner/renter and an insurance company, where the insurer agrees to cover financial losses for damage and liabilities in exchange for the premiums you pay. Condo insurance is designed to help protect owners from losing their home should disaster strike, as long as they are within the boundaries of the covered perils laid out in their policy.

What Is HO6 Insurance?

HO6 insurance is another name for condo and co-op insurance. In comparison, homeowners insurance is often referred to as HO3 insurance, and renters insurance is referred to as HO4 insurance. Condo insurance and HO6 insurance cover the interior of your unit, or the part not covered by your landlord or condo association's master policy. From the walls to your personal belongings, this coverage can reimburse for theft, damage, or destruction by listed disasters. It also covers your personal liability if you get sued by a third party.

How Is Condo Insurance Different from Home Insurance?

Condo insurance operates very similarly to homeowners insurance, but it’s customized to work specifically for the unique needs of condominiums. While the building itself is owned and insured by the condo association, your personal space needs insurance coverage in order to adequately protect you from the unexpected.

The term “condo” is a legal distinction for the type of property, and certain declarations are added to owners’ contracts to dictate what percentage of the “common elements” they’re responsible for (e.g., AC units, pools, etc.). As a condo owner, you're responsible, not only for your own personal property, but also for a few select elements of the main building and its common elements.

Obviously, since a condo owner has unique responsibilities that other homeowners don’t, the insurance policy is designed to cater more specifically to their needs. An independent insurance agent is exactly who you need to walk through your condo's contract and clear up any remaining questions you may have.

CONDO INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

What Does Condo Insurance Cover?

Beyond your personal spaces and any shared spaces you're responsible for, condo owners also need protection for friends, family, and other guests who may visit their home, which means having legal or liability coverage.

The more complex your condo and your individual responsibilities are, the more coverage you may need. But here are the three major coverage areas included in standard condo insurance policies available.

Dwelling coverage: This covers your unit’s structural components like the walls, ceilings, and floors.

Personal property coverage: This covers your personal belongings like furniture, clothing, electronics, knickknacks, silverware, etc., that are stored within the unit against perils such as fire or theft. This coverage also protects the building elements you’re responsible for, like toilets, showers, flooring, etc.

Liability coverage: This covers legal expenses, like attorney fees, court fees, and settlements, if you are sued for bodily injury or property damage to a third party.

These three components make up the core of condo insurance packages. Working together with an independent insurance agent is a great way to get the right amount of coverage in each category for your unique home.

Condo Coverage

Basic

Extra

Dwelling, walls in

Personal property actual cash value

Liability

Loss of use

Debris removal

Association loss assessment

Fire dept service charge

Medical payments to others

Ordinance or law

Sewer backup

Flood

Workers' compensation

Earthquake

Other structures

All perils

Scheduled personal property

Personal property replacement value

What Doesn't My Condo Insurance Cover?

Like every other kind of insurance out there, condo insurance comes with a list of specified covered perils as well as non-covered perils. Becoming familiar with what your condo insurance policy doesn’t cover can save you the hassle of filing claims that are bound to get denied, and in the event of certain non-covered natural disasters, help you find the right kind of policy to protect your home.

Condo insurance does not cover the following:

Certain natural disasters (i.e., floods, earthquakes, and mudslides)

Maintenance-related losses

Wear-and-tear damage (i.e., failure of the condo owner to maintain upkeep of the home)

Insect damage or infestations

Damage from war or nuclear fallout

Business-related liability

Also, if you run a business out of your condo, your insurance won’t cover any liability-related mishaps. Further, as far as natural disasters go, to protect your unit against flood or earthquake damage, you’ll need a flood insurance or earth movement policy. Flood insurance policies are only available through the National Flood Insurance Program, which is a part of FEMA. Condo owners located in areas prone to flooding may want to seriously consider getting a policy.

How Condo Insurance Rates Are Calculated

Insurance companies determine the cost of condo insurance by reviewing a few factors, including your condo's location and its unique risks. Whether you have HOA coverage will also affect your premiums, as will the construction and value of your condo. The bigger and more expensive your condo is, the higher your condo insurance premiums are likely to be.

How Much Does Condo Insurance Cost?

Many factors influence the cost of a condo insurance policy, including the size and location of your condo, the value of the structure and its contents, and any upgrades you’ve made. Condos located in areas prone to severe weather or other risks like crime will come with more expensive insurance policies than those in calmer, safer areas.

While it’s hard to offer an exact figure without knowing your unique living situation, a general range for condo insurance usually falls between $200 and $2,000 annually ($488/year being the average). Unless you’re buying a particularly expensive unit in a major city, though, you can typically expect to pay toward the lower end of the range for coverage. An independent insurance agent can help find more exact quotes for you.

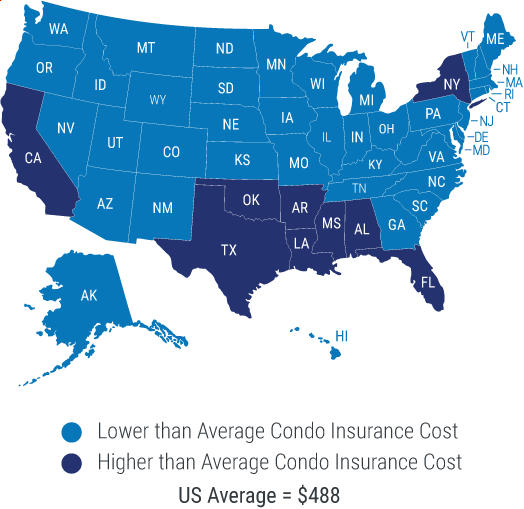

Average condo insurance rates by state

State

Monthly Insurance Rate

Annual Condo Insurance Rate

Alabama

$41

$490

Alaska

$33

$390

Arizona

$53

$640

Arkansas

$44

$530

California

$58

$690

Colorado

$32

$380

Connecticut

$41

$495

D.C.

$35

$425

Delaware

$33

$395

Florida

$117

$1,400

Georgia

$64

$765

Hawaii

$42

$505

Idaho

$31

$370

Illinois

$34

$410

Indiana

$39

$470

Iowa

$27

$325

Kansas

$35

$415

Kentucky

$30

$355

Louisiana

$59

$705

Maine

$25

$305

Maryland

$37

$445

Massachusetts

$45

$535

Michigan

$31

$370

Minnesota

$31

$375

Mississippi

$51

$610

Missouri

$37

$445

Montana

$33

$400

Nebraska

$33

$400

Nevada

$48

$575

New Hampshire

$31

$370

New Jersey

$38

$455

New Mexico

$28

$340

New York

$41

$495

North Carolina

$55

$660

North Dakota

$29

$345

Ohio

$28

$330

Oklahoma

$52

$625

Oregon

$35

$420

Pennsylvania

$30

$365

Rhode Island

$59

$710

South Carolina

$38

$460

South Dakota

$30

$360

Tennessee

$38

$455

Texas

$60

$715

Utah

$37

$440

Vermont

$21

$255

Virginia

$30

$365

Washington

$35

$425

West Virginia

$21

$255

Wisconsin

$22

$315

Wyoming

$29

$350

US Average

$38

$455

How Much Condo Insurance Do You Need?

Condo insurance provides coverage for more than just your belongings. It also protects you, your family, and your guests. To calculate how much coverage you need, you'll first consider your condo's specific protection requirements. The main coverages found in standard condo insurance policies are for the building's structure, your personal property, and your liability exposures.

Our quick quote calculator at the top of the page or an independent insurance agent can help you calculate how much condo insurance coverage you need. You'll need to go through each main coverage area and assess your needs in every category. You may need to increase coverage in one place, such as the contents section, if you have a lot of personal property.

How HOA Coverage Affects Condo Insurance Rates

If your Homeowners Association provides its own coverage for part of your building, you won't have to pay for as much coverage yourself. If your HOA offers all-in coverage, you'll pay only about 60% of what a condo owner without any HOA coverage would. If your HOA only provides bare walls coverage, you'll pay about 88% of what someone without any HOA coverage would.

How Value Affects Condo Insurance Rates

The value of your condo is also an important factor in determining your coverage rates. Owners of condos valued between $400,000 and $500,000 can pay nearly 1.4 times the average cost of coverage, while condos valued at less than $150,000 can pay about 2.25 times less. The more valuable your condo, the more expensive it is to insure.

Average Condo Insurance Rates Per Month

The current national average cost of condo insurance is $488 annually, which breaks down to about $40.67 monthly. While you can expect to pay somewhere in this general range for your coverage, the cost of your specific policy depends on many different factors. Your specific location is just one of them.

Factors Impacting Condo Insurance Costs

The cost of your coverage depends on a few factors, like your condo's location and value, your credit score, and more.

Factors that determine the cost of condo insurance and how:

Factor

Description

Impact on Condo Insurance Costs

Average annual premium

Across the US and DC

The national average cost for condo insurance is $488 annually, but rates vary by location and other factors.

Condo location

Including all 50 states and DC

Your condo's location impacts the cost of your coverage by factoring in your area's risk of crimes and storm damage and overall property values.

Condo value

The appraised value typically ranges from less than $50,000 up to $500,000

Your condo's value impacts the cost of your coverage since more expensive units would cost more to repair/replace, so insurance rates are higher.

Age of building

The building's age, measured in years

Buildings more than 30 years old have much higher premiums due to the increased risk factor.

Deductible amount

Refers to the amount you have to pay out of pocket before the insurer covers a claim, ranging from less than $2,500 to more than $7,500

Higher deductibles mean lower condo insurance premiums and vice-versa.

Type of HOA coverage

Homeowners Association Coverage varies from "bare walls" to "all in," etc.

The more comprehensive your HOA coverage, the smaller the condo insurance premium will be.

Security features

Installed security and safety features like burglar alarms, fire alarms, sprinklers systems, security arrangements with professional companies, etc.

More security/safety features can lead to lower premiums, and likewise, the absence of these features can increase premiums considerably or even lead to a rejection of a coverage application by the insurer.

Location exposures

If the property is located in a crime-prone or flood-prone area or is otherwise exposed to threats based on its location

Premiums for condo insurance can more than double if the building's location is considered hazardous.

Credit score

Your credit score, ranging from "poor" to "excellent"

Though not always a factor that impacts premiums, a "poor" credit score can lead to premiums up to double the usual amount. In contrast, "excellent" scores can reduce premiums by about 15%.

Insurance company

Condo insurance rates and premiums vary considerably by the insurer, as do the factors the insurer considers when determining premium rates

An insurance company awards additional discounts on condo insurance coverage if you have other coverages with them already.

How to Lower Condo Insurance Costs

Many insurance companies offer several discounts on condo insurance to help lower the cost of your premiums. Here are just a few standard condo insurance discounts.

Sprinklers discount: Many insurance companies will reward you with a discount on condo insurance if your unit has a built-in sprinkler system to guard against fire damage.

Bundling discount: Many insurance companies offer discounts if you bundle your condo insurance with another policy, such as auto insurance.

Protective device discount: Many insurance companies offer lower rates on condo insurance if your unit is equipped with a security device like a burglar alarm.

Claims-free discount: Many insurance companies will reward you over time if you remain claims-free through condo insurance for a couple of years.

Paid-in-full discount: Many insurance companies lower your overall premium if you pay for your entire year's coverage up-front.

Your independent insurance agent can assist in helping you find any discounts you qualify for on condo insurance, no matter where you're located.

Condo insurance isn’t required by law, but nearly every lender will require a policy to give you a loan. At a minimum, they’ll want your policy to cover the amount you owe on the loan. It’s their way of protecting their investment in you.

Your condo association has existing coverage to protect you, but that only covers the exterior and the shared spaces of your condo. When it comes to property and liability concerns inside your condo unit, you will need your own separate protection.

As you can imagine, because a condo is different from a home, the insurance coverages needed to protect each are different. With condos, you'll typically only need to insure the area within your owned walls, and not all the shared space, though this does vary. The condo insurance form reflects that limited coverage area. It doesn’t include things such as Coverage B - Other Structures that are located on your home’s property, such as a detached garage or utility shed.

An HO6 insurance form is the type of insurance that covers condos, so they are the same thing. Each type of property insurance that applies to individuals (and not businesses) has its own insurance form with different coverage sections and contractual language, such as HO1, HO2, HO3, HO4, HO5, and HO6.

Your condo insurance policy will come with some automatic coverage options, but you’ll need to work with your independent insurance agent to determine the appropriate values based on your specific needs. Typically, all condo insurance policies come with personal property and liability coverages, but you can always add on additional protections like water backup or personal cyber insurance.

The condo association’s insurance policy will typically cover the structure of the building, like the roof and walls. It typically covers any shared common areas as well, such as the lobby, pool, or exercise area. This will include both property coverage and liability coverage. It won’t, however, cover what’s located inside each condominium unit.

It's best to have your independent agent review your condo association's policy to make sure you don't overlap coverages or leave any dangerous gaps.

No, your own personal condo insurance policy will only apply to the property and space within the walls of your own condo. Other units will be covered under their owners’ insurance policies, while the common areas and base structure of the building will be covered by the condo association’s insurance policy. However, if you’re responsible for causing damage to another person’s condo unit, your liability coverage would be likely to pay for the other person’s damage.

No, condo insurance is treated the same as homeowners insurance by the IRS and isn’t tax deductible. There are other tax deductions that are similar, like mortgage insurance through the VA, FHA, or RHA, but condo insurance is not a deductible item on your taxes.

When it comes to renting your condo through Airbnb, or any other service, condo insurance protects you essentially the same way a homeowners insurance policy would while you’re away. If there was a fire at the Airbnb and your stuff got damaged or destroyed, you’d be covered under your personal property coverage the same way as you would under a homeowners insurance policy, even though you’re away from home.

Your Independent Insurance Agent Has Answers for All Your Condo Insurance Questions

Whatever you need, your agent has your back. With a brief intro into the terms, discounts, and process of your condo insurance, you now know the kinds of questions to be asking. Your agent will ask you all about your condo, its use, and your future goals to help find the perfect blend of coverage at the right cost for your budget.

Best Condo Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What Our Customers Are Saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.