How Long Does Voluntary Long Term Disability Last?

(It can be, but don't forget to explore your other options.)

Maggie Tiede is a writer and blogger based in Saint Paul, Minnesota. Maggie has worked as a freelance writer since 2013, when she began reporting on politics, local events, health, and human interest for the Grand Rapids Herald-Review.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

What would happen if you became unable to work? Government benefits aren’t a guarantee and take a long time to kick in. Voluntary disability insurance is there to bridge the gap and keep your family afloat if you become permanently disabled.

Buying voluntary insurance through your employer has a tax benefit, but it might not be the best deal for you. Once you’re ready to shop, expert independent insurance agents are here to answer your questions and find you the coverage you need at the right price.

What Is Voluntary Disability Insurance?

Voluntary disability insurance covers a percentage of your income if you become disabled. You cover the entire premium of this insurance rather than an employer chipping in part of the money. (And you can opt out of this coverage, hence the “voluntary” part.)

It may feel stingy for your employer to put the total cost on you, but there’s a tax benefit: In return for taking on this cost, you get your benefits tax-free if you ever become disabled and need to access them. That can save you money in the long run.

Group vs. Individual Voluntary Disability Insurance

Disability insurance is sold two ways: in group policies or in individual policies. Voluntary insurance is a type of group insurance.

Group policies are purchased through your employer. You’re placed in a risk pool with the other people at your company, which is to your advantage if you’re at higher risk of disability (for example, if you’re 50 or over) and to your disadvantage if you’re at lower risk.

Group vs. Individual: Which Is Better?

| Type | Benefits Offered | Benefits Period | Pros and Cons |

| Individual | Flat income amount | Short-Term: 1-5 years Long-Term: from 2 years till retirement |

Pros: Full control over the coverage; no loss of coverage when you change jobs; can shop from any company for the best offerings. Cons: Can be expensive if your risks are higher. |

| Group | Percentage of income | Short-Term: less than 1 year Long-Term: from 2 years till retirement |

Pros: If you're at high risk for disability, pooling coverage with others can be cheaper. Cons: Limited options; you lose coverage when you switch jobs. |

Source: Principles of Life and Health Insurance

Both individual and group disability insurance have their pros and cons. With voluntary insurance, since you’re taking on the full cost of the premium anyway, you may decide it’s better to shop on your own rather than stick with your company’s offering.

Whatever you end up choosing, it pays to at least check out your individual options as well as your voluntary group options. There may be unique discounts or perks you qualify for individually that you’d lose out on in a group.

Save on Disability Income Insurance

Our independent agents shop around to find you the best coverage.

How Long Does Voluntary Long-Term Disability Insurance Last?

Long-term voluntary disability insurance is designed to cover permanent or long-lasting disabilities that prevent you from working or significantly affect how much and what type of work you can do, forcing you to take a pay cut.

Long-term disability insurance typically kicks in within 2 weeks to 9 months. Once it starts, its benefits can last anywhere from 2 years until retirement (or rarely, until your death).

How Long Does Voluntary Short-Term Disability Insurance Last?

Short-term voluntary disability insurance is designed to cover temporary disabilities lasting a few months to a year or two. This could include situations like a head injury, a severe infection, or a bad flare-up of a chronic condition like migraines.

Short-term disability insurance can kick in instantly. More commonly, it has a short waiting period of 7-90 days. Once it starts, voluntary group policies typically last 6 months to 2 years.

Why Is Voluntary Long-Term Disability Insurance Important?

Long-term disabilities can happen at any time. Because they are permanent, they can wreak havoc on your finances if you drain your savings, since you’ll be unable to work to replenish them. What would you do if you lost your job or had to go on unpaid leave because of disability?

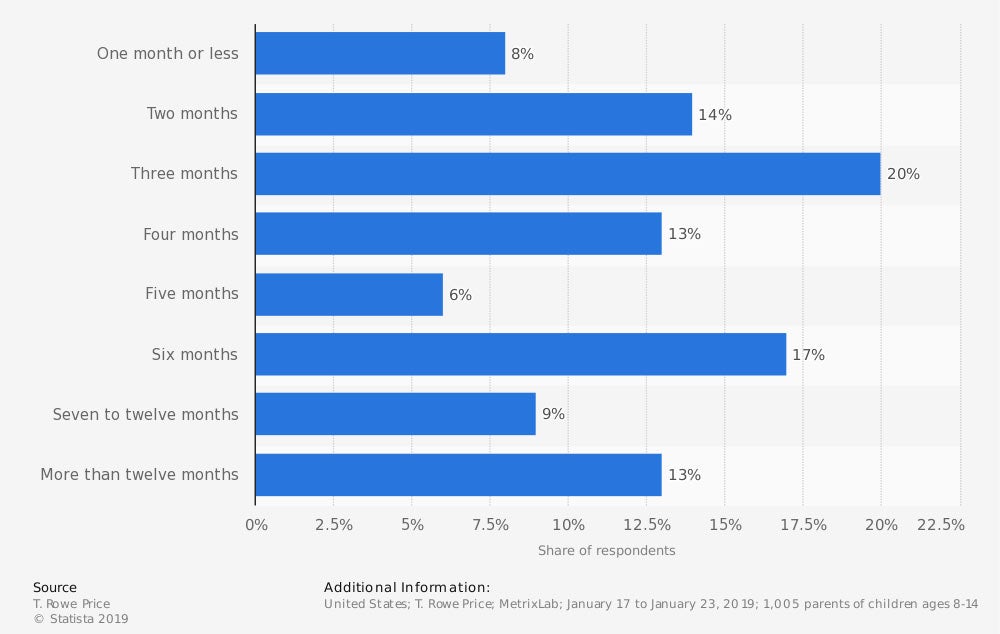

The Savings Crisis

For how many months would your emergency fund cover your family's expenses?

In 2019, fewer than half of Americans had enough in savings to carry them beyond a 6-month emergency. Nearly a quarter of Americans only had enough for less than two months.

Long-term disability insurance has a longer waiting period than short-term insurance, but it provides a steady income for many years. It helps you live comfortably with a disability instead of being constantly on the edge of financial crisis.

Save on Disability Income Insurance

Our independent agents shop around to find you the best coverage.

Do I Lose Voluntary Disability Insurance If I Quit My Job?

The prospect of losing your benefits can be one of the worst parts of changing jobs. That’s why insurance companies almost always offer you the option to continue your coverage after leaving your job.

If your employer is covering part of your premiums, this can end up being a bad deal. You will now be forced to shoulder more of a cost for the same benefit. With voluntary insurance, however, this does not affect the cost, since you were paying the whole premium to begin with.

That said, continuing your workplace’s voluntary disability insurance isn’t always the smartest thing to do. Changing jobs is a good time to reevaluate your insurance needs and find out if you could be getting better discounts elsewhere. Independent insurance agents can help.

What about Government Benefits?

If you’re currently making a middle-class salary or higher, government benefits will not help you meet your financial obligations if you become disabled. They also have strict work restrictions and require invasive legal processes to get.

There are two main government disability benefit programs for long-term disability: Supplemental Security Income (SSI) and Social Security Disability Insurance (SSDI). In 2016:

- SSI capped payments to qualifying individuals at $733 per month and to qualifying couples at $1,100. SSI is also subject to strict income and asset limits that can prevent you from saving money or ever going back to work, even if you feel up to it.

- SSDI paid disabled workers supporting a spouse and one or more children an average of $1,983 per month. That number was slightly higher for a retired disabled couple ($2,212) and much lower for a single disabled worker ($1,166).

Disability insurance can provide you with significantly more monthly benefit than government options. It also starts paying you that benefit faster.

What to Do When Voluntary Long-Term Disability Insurance Runs Out

Most long-term disability insurance policies last until your expected retirement (usually between the ages of 65 and 70). At that point, you can access Social Security retirement benefits.

However, some long-term policies may run out sooner, after 5 or 10 years. In this case, you can use government benefits or life insurance to make up the shortfall.

How Life Insurance Can Help

If you’re all out of disability-specific options, take another look at your life insurance policy. Whole life insurance policies gain cash value over time and can eventually be converted into cash value or even monthly payments (annuities) that can function like disability insurance.

If you don’t currently have a whole life insurance policy, this is another reason they’re a great financial planning tool. Whole life insurance can be used to pay for a generous retirement if you stay healthy, or it can be used to cover disability and long-term care costs if you need them.

Save on Disability Income Insurance

Our independent agents shop around to find you the best coverage.

How an Independent Insurance Agent Can Level Up Your Disability Insurance

Shopping for disability insurance yourself can be a downer. It’s hard to know where to look, how much insurance you need, or how to find a good deal. Luckily, independent insurance agents are here to handle the hard parts for you.

Independent insurance agents are industry experts who aren’t bound to any one company. They can compare quotes from multiple insurers to find you the coverage you want at the right price. Shopping for disability insurance with an independent insurance agent is shopping smart.

iii.org

SSA.gov

The Long Term Care Handbook (3rd edition) by Jeff Sadler

Nolo’s Guide to Social Security Disability: Getting and Keeping Your Benefits (8th edition) by David A. Morton III, M.D.

Principles of Life and Health Insurance (2nd edition) by Dani L. Long and Gene A. Morton