Traditional Long-Term Care Insurance Cost

(Three key factors affect how much you'll pay for this essential coverage)

Maggie Tiede is a writer and blogger based in Saint Paul, Minnesota. Maggie has worked as a freelance writer since 2013, when she began reporting on politics, local events, health, and human interest for the Grand Rapids Herald-Review.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

Could you afford to enter a nursing home if you needed one? As Americans age, long-term care is more necessary than ever. Traditional long term care insurance is there to pay for it.

Traditional insurance offerings and costs vary widely from company to company. Independent insurance agents can shop them all instead of being bound to one company, saving you money and time. Here’s what you need to know about the cost of traditional long-term care insurance.

What is Long-Term Care Insurance?

Long-term care insurance pays for long-term care (usually for a nursing home, but sometimes for assisted living or a home health aide) if you ever need it. You pay monthly or yearly premiums in exchange for that coverage.

There are two main types of long-term care insurance: hybrid and traditional.

Traditional long-term care insurance is a stand-alone policy. Hybrid long term care insurance is blended with life insurance and both have their perks. A traditional policy is usually simpler and more streamlined than a hybrid policy.

What is the Cost of Long-Term Care Insurance?

The cost of long-term care insurance is based on three main factors:

- Your age: The younger you are, the cheaper it will be because you’re likely to have more years of paying premiums before filing a claim.

- The amount of daily benefit and years of coverage you choose: Less benefit and fewer years means cheaper premiums but less coverage.

- Your location: Your state and its cost of living also affect the cost of long-term care insurance.

What is the cost of long-term care insurance state to state?

The cost of traditional long-term care insurance can vary a lot from state to state. States regulate long-term care insurance differently, which means insurance companies sell and market them differently.

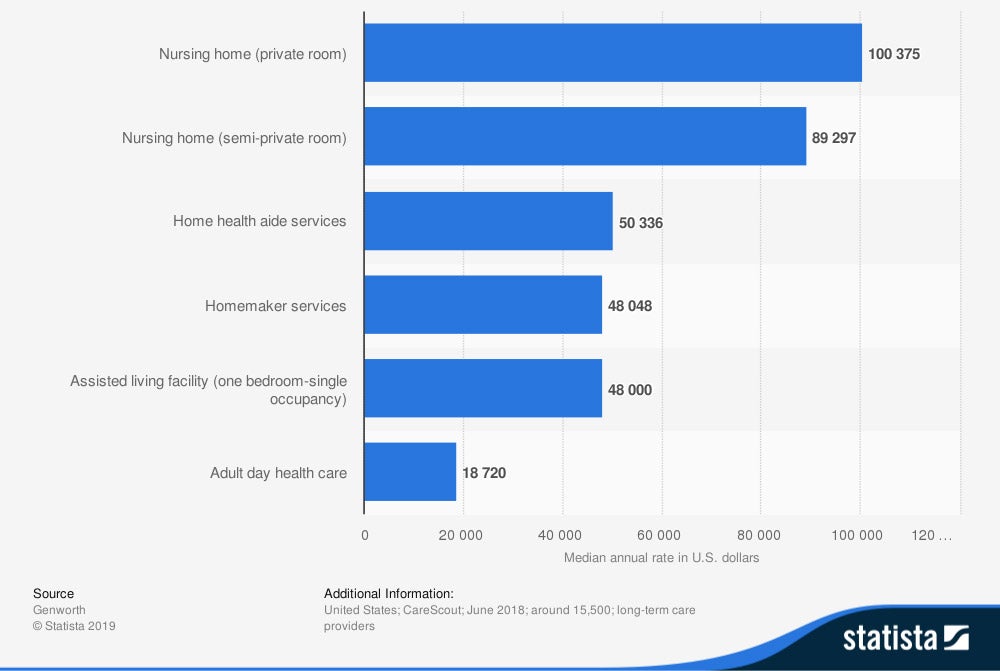

Annual median rate of long-term health care services in the United States as of 2018, by type (in US dollars)

The nationwide average annual cost of a private room in a nursing home topped $100,000 last year. But that’s just the nationwide average. The Northeastern US, as well as Alaska and Hawaii, have much higher costs for long-term care. The Midwest and South tend to have lower costs.

Those costs get folded into the cost of traditional long-term care insurance meaning premiums will be higher in more expensive states (and lower in cheaper ones).

Independent insurance agents are experts in the long-term care insurance options and costs in your state. They’re the definitive source for information about the cost of traditional long-term care insurance state by state.

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Hybrid vs. Traditional Long-Term Care Insurance

There isn’t usually a significant difference in cost between hybrid and traditional long-term care insurance. The difference is in the benefits:

Hybrid long-term care insurance

Hybrid long-term care policies are a new type of long-term care insurance steadily growing in popularity.

Hybrid insurance blends life insurance coverage and annuity options with long-term care insurance. You pay premiums towards a death benefit (just like with life insurance) but can “cash in” that benefit to pay for long-term care if you need it.

This allows you to hedge your bets and guarantee that you’ll get at least some benefit out of your long-term care insurance.

Traditional long-term care insurance

Traditional long-term care insurance is the original type. It’s a stand-alone policy purchased separately and administered separately from other policies like life insurance.

This means it’s more straightforward than a hybrid policy, which makes it easier to understand and plan around. You pay premiums toward the policy and file a claim if you ever need it. That’s it!

The downside of a traditional policy is that you may not ever use it, meaning you paid premiums for no cash benefit — but many find that the peace of mind that this policy offers is benefit enough on its own.

Which one is best?

It all depends on your needs and preferences. Hybrid policies offer flexibility while traditional policies offer simplicity.

| Traditional | Hybrid | |

| Benefits | Long-term care only | Long-term care, death benefit for heirs, cash values |

| Premiums tax-deductible | Yes | No |

| Tax-free benefits | Yes | Yes |

| Partnership plans available | Yes | No |

| Refund for unused benefits | May be available at an extra cost | Yes |

| Can premiums increase? | Yes | On some policies |

Long-term care insurance is an investment so it’s important to make sure you’re making a good one. Many independent insurance agents are also certified financial planners. They’re experts who are well equipped to help you make these big decisions.

How to Buy Traditional Long-Term Care Insurance

Buying traditional long term care insurance is easier than you might think. Here’s how to do it, step by step:

- Research the cost of long term care in your area: Look for the average “per day” cost of care in your area (typically a number in the $100-300 range).

- Determine how much of that cost you’ll be able to pay from savings and other sources: Any shortfall needs to be covered by long-term care insurance.

- Contact an independent insurance agent: They’re experts who can shop around and find you quotes that make the most sense for your situation. If you’re on the fence about buying traditional insurance, they can help you compare hybrid and traditional options.

- Fill out a medical history (and maybe get a medical exam): Your health status will affect the cost of premiums, so the insurance company will need to verify it before giving you a quote. You may be able to get this exam at home — ask your agent.

- Get quotes and compare them: Your agent will round up a series of quotes for you. The cheapest quote may not be the best one so be sure to compare the size of the benefit and years of coverage before choosing to ensure you’re getting bang for your buck.

- Sign on the dotted line! It’s that easy to buy long-term care insurance. Congratulations! You’ve just secured your financial future so your golden years can stay truly golden.

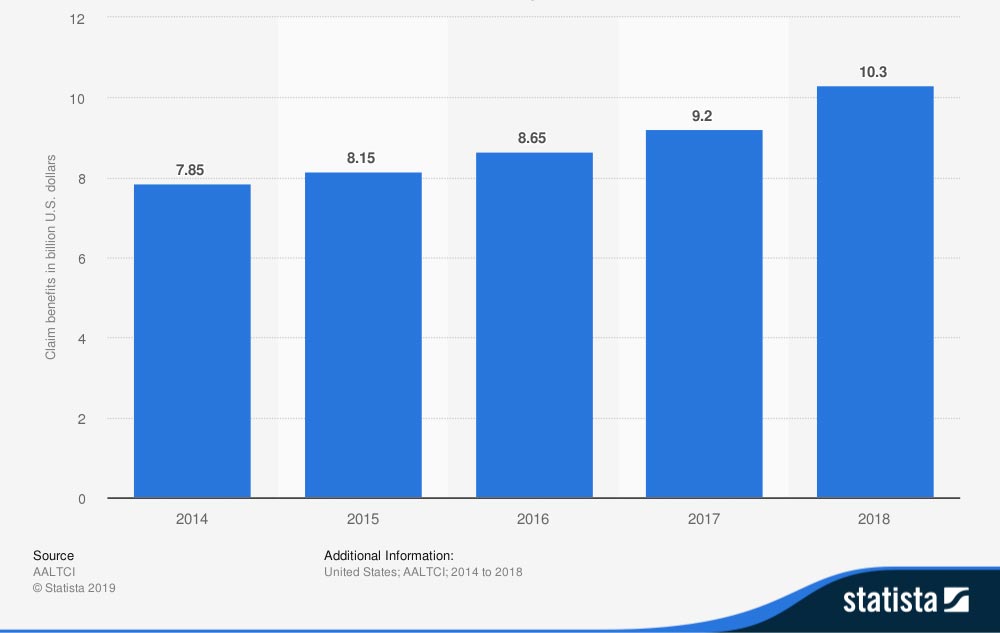

Amount paid in claim benefits to individuals by long-term care (LTC) insurance companies in the United States from 2014 to 2018 (in billion US dollars)

Long-term care insurance companies paid out over 10 billion in benefits to their customers in 2018 alone, and that number is only trending up. Buying traditional long-term care insurance now secures you a piece of the pie — along with peace of mind.

Save on Long Term Care Insurance

Our independent agents shop around to find you the best coverage.

Why Independent Insurance Agents?

Independent insurance agents are unique. While captive insurance agents can only sell insurance from one company, independent insurance agents can shop around between multiple companies to find the real right deal for you, not just one company’s “best” deal.

With an independent insurance agent, you can be sure you’re talking to a real expert who knows traditional long-term care insurance inside and out. Good luck shopping for this critical coverage.

National Academy of Social Insurance (https://www.nasi.org)

Medicare.gov

Medicaid.gov

LongTermCare.acl.gov