Your quote is based on several common factors to give you a clear picture of the cost you can expect, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

Commercial auto insurance is a type of coverage designed to protect company vehicles, including cars, vans, and trucks, that are used for operations related to the business. This coverage protects company vehicles against costs related to liability, physical damage, accidents, driver injuries, and more.

The right commercial vehicle insurance policy can help ensure that your business vehicles get repaired in a timely manner after an incident. It can help cover the cost of replacing a business vehicle if it gets totaled by an accident, storm damage, etc. Insurance for commercial vehicles is easy to find, and an independent insurance agent can help you shop multiple carriers for the perfect coverage. They'll help you find the right commercial vehicle insurance at the right price, meet your local legal requirements for vehicle insurance and, most importantly, protect your business’s bottom line.

What Is Commercial Vehicle Insurance?

Commercial vehicle insurance covers a business’s vehicles, whether it's a fleet of delivery trucks, catering trucks, or a few 4-door sedans. Each policy provides protection specifically designed for business vehicles, including physical damage and liability coverage.

Some businesses spend a lot of operating time on the road, while others are only driven occasionally. An independent insurance agent can help you find the right protection regardless of how much your business vehicles are used.

What Does Commercial Vehicle Insurance Cover?

Commercial vehicle insurance coverage may vary from one insurance company to the next, but policies can be uniquely tailored to suit your specific needs. Working with an independent insurance agent is extremely helpful in pinpointing the exact coverage your business vehicles need. That coverage can include property damage, liability, bodily injury, personal injury, collision, uninsured coverage, medical payments, and much more.

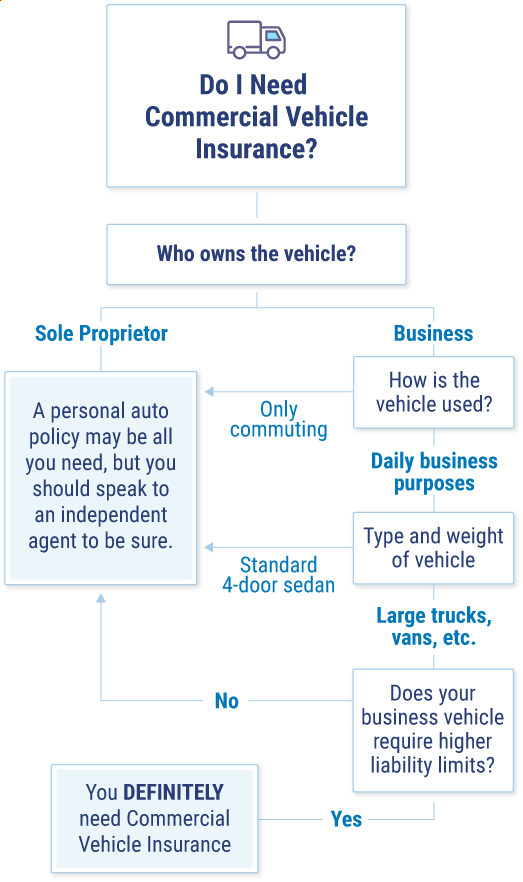

Who Needs Commercial Vehicle Insurance?

If driving is a significant part of your day-to-day business operations, you'll most likely need more comprehensive commercial vehicle coverage than a business that only uses its vehicles occasionally. If you’re a small business owner who uses a personal vehicle regularly for business (e.g., a florist who uses a delivery truck for flowers), you'll probably need commercial vehicle insurance. If your business has dedicated company vehicles, getting a policy is absolutely necessary.

If you employ delivery drivers or couriers who use their own personal vehicles in the line of business, you’ll need to buy special commercial vehicle insurance for them, known as non-owned vehicle coverage.

Why Is Commercial Vehicle Insurance Important?

Driving without insurance is almost always illegal. Personal auto insurance coverage excludes commercial driving, meaning you don't have coverage when driving your car for business purposes. If you fail to get a commercial auto policy, you could face hefty fines and/or other penalties.

Not to mention, if you wrecked an uninsured business vehicle, you’d have to replace it out of pocket, which could cut into your business’s bottom line. If a commercial vehicle got involved in a crash that injured others, the cost could soar even higher when factoring in the costs of injury treatment and possible liability charges.

Is Commercial Vehicle Insurance Required by Law?

Commercial vehicle insurance is mandatory for all your business’s vehicles and is a crucial part of business insurance. Any business vehicle such as a taxi, van, limo, bus, or small truck used for company purposes needs the right protection. A personal auto policy won't cover vehicles when they're used for business purposes.

A commercial vehicle policy protects you and your business from the costs of property damage, injury, and liability claims that may arise from using your commercial vehicles.

For larger commercial vehicles like tow trucks, cement trucks, construction vehicles, tractor-trailers, or semi-trucks, you'll need a commercial truck insurance policy.

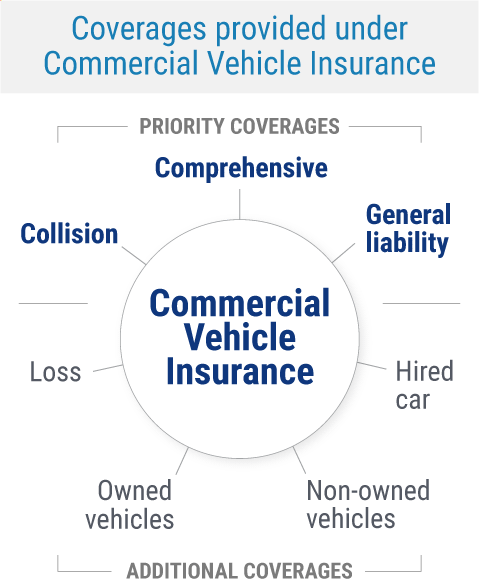

Commercial Vehicle Insurance Coverage Types

Your business's coverage will depend on your unique operations and needs. Together with an independent insurance agent, you can tailor your commercial vehicle insurance policy based on your specific company vehicles and your business’s size and niche. Commercial vehicle insurance often includes the following:

Collision: Covers costs related to a collision, including physical damage repairs to a company vehicle.

General liability: Covers damage to property or injury to others involved in a collision with a business vehicle.

Comprehensive: Covers damage unrelated to a collision, including fire, vandalism, or fallen objects like trees.

Theft: Covers replacement costs if a company vehicle gets stolen.

Owned vehicles: Covers all aspects of vehicles owned under a business's name.

Non-owned vehicles: Covers vehicles not owned by the business but driven by its employees, like a salesperson's personal car.

Hired car: Covers vehicles that are rented by a business.

An independent insurance agent can help ensure that you walk away with a commercial auto insurance policy that incorporates every aspect of coverage your business needs.

COMMERCIAL VEHICLE INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

Who Sells Commercial Auto Insurance?

Commercial auto insurance is available from many different insurance companies, and the best way to find the right carrier for you is through working with an independent insurance agent. They know which insurance companies to recommend to meet your needs, and can provide informed suggestions based on company reliability, rates, and more.

While many insurance companies could create a commercial auto insurance policy for you, finding coverage could also depend on the area you live in. Here are a few of the top companies for commercial auto coverage:

Frequently Asked Questions about Commercial Vehicle Insurance

You need commercial auto insurance for any vehicle used for business purposes, with a commercial license plate, or registered as a commercial auto.

You may also be required to get commercial vehicle coverage if your vehicle is used for any of these purposes:

Carrying equipment

Transporting flammable or hazardous materials

Transporting housekeeping equipment for business use

Carrying or transporting cranes, winches, or plows

Towing other vehicles as a service

Delivering goods, like pizza, or wholesale or retail products

Delivering newspapers

Transporting products

Transporting people as a chauffeur, limousine service, or taxi service

Business auto usually covers non-owned vehicles used for the business. Personal use of a vehicle is covered for a company-owned vehicle as long as the company has commercial auto coverage. If you're driving your own vehicle to and from work, not for business purposes, it should be covered under your personal auto policy.

Suppose you use your personal vehicle occasionally for commercial purposes. An employee using their personal vehicle for business purposes would be covered under that provision rather than their personal insurance.

The cost of commercial auto insurance depends on several things, including the size of your business, the type and number of company vehicles, your business's risks, and the amount of coverage you need.

Generally, a passenger auto vehicle will cost much less to insure than a heavy-duty vehicle like a dump truck. However, insurance carriers also offer fleet insurance, and these policies are often available at a bulk discount.

The cost of commercial auto insurance also depends on the driving records of the employees who will be operating business vehicles. Employees with bad driving records will cost more to insure, so it's critical to perform a driving record background check on prospective employees. Drivers between the ages of 30 and 65 are typically given better insurance rates.

In most cases, yes, commercial auto insurance is typically more expensive than a personal auto insurance policy. The cost depends, however, on the vehicle type, all drivers' records, vehicle use, coverage options chosen, and other factors. An independent insurance agent can help you compile and compare several quotes for both commercial auto coverage and personal auto coverage to get exact rates for each.

If your commercial auto insurance policy includes comprehensive coverage, yes, it will cover the theft of a business vehicle listed on the policy. If a business vehicle gets stolen, there are a few things that must happen to get compensated for the loss and get your company drivers back on the road.

First, a police report must be filed while the business owner waits for the police to attempt to recover the stolen vehicle. If the vehicle isn't recovered and you have comprehensive coverage, you can file a claim with your insurance company. After some paperwork, your insurance should compensate you for the loss up to the limit of your comprehensive coverage.

Your Independent Insurance Agent Has Answers to Your Commercial Vehicle Insurance Questions

Whatever you need, your independent insurance agent is there for you. With a brief intro into the terms, discounts, and process of your commercial vehicle insurance, you know the kinds of questions to be asking. Your agent will ask you all about your business vehicles and their use to help find the perfect blend of coverage and the right cost for you.

Best Commercial Auto Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What Our Customers Are Saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.