Your quote is based on several common factors to give you a clear picture of the cost you can expect, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

Is your small business protected from the unthinkable? Small business insurance provides thorough coverage for your finances and your company, acting as a safety net when disasters, accidents, and other risks affect your business. Whether it's a mom-n-pop family business, a home consulting business, or a small candle shop business, an independent insurance agent is the answer to finding the right coverage to protect you from whatever may come, all at the right price for your budget.

Each business is different, and yours deserves a small business insurance policy that meets its unique needs. Read on to better understand what insurance for small businesses can cover, who needs it, and how to save money on your policy.

What Is Small Business Insurance?

Small business insurance is a package of coverage designed to help protect small businesses from financial damage caused by lawsuits, accidents, natural disasters, and other events that could impact your business. When a covered event occurs, your policy will help cover some or all of the associated costs, up to the policy’s limits.

Why Do I Need Small Business Insurance?

Insurance for small businesses can help keep your business running or financially support you when something unexpected happens, such as a fire that causes your business to temporarily close for repairs. Without this protection, even one untimely event could bankrupt your business and disrupt your income.

Low-risk businesses still have risks, and even the strongest businesses may struggle to cover the costs of a liability lawsuit, temporary closure, or similar event. Small business insurance may not be required by law, but it helps protect your finances and the stability and longevity of your company.

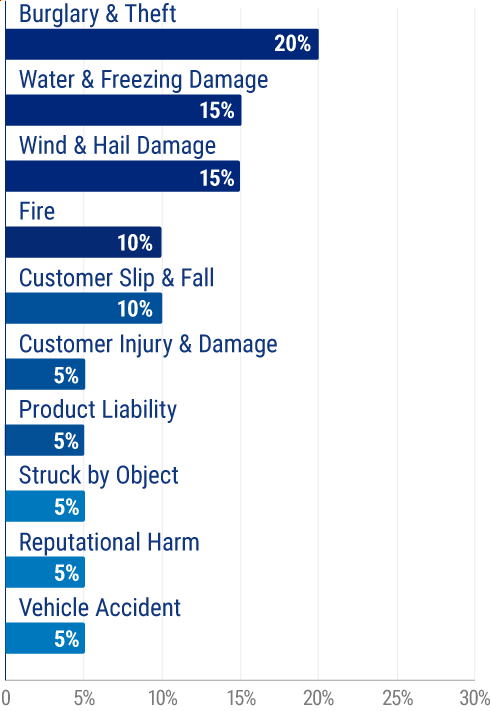

Top 10 Small Business Insurance Claims

How Is Small Business Insurance Different from Standard Business Insurance?

Small business insurance is designed to accommodate the lighter insurance needs of smaller businesses. A large corporation may need an insurance policy to cover its fleet of delivery vehicles, multinational liability risks, and billions in revenue. Small businesses generally have much simpler needs, even when they vary by industry.

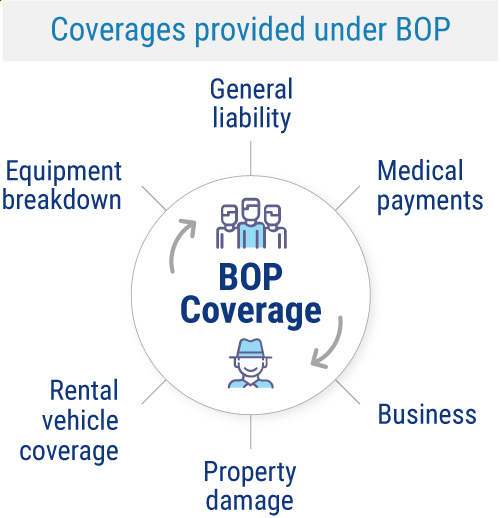

A small business insurance policy means you get the coverage you need without paying for coverage you don’t. It should cover the basic risks your unique business may encounter – bundling options like property, liability, and loss of income insurance into one custom policy.

Property insurance: This covers your business’s property, like buildings, equipment, and inventory from loss or damage due to fire, storms, and covered events.

General liability: This provides financial protection if you face a lawsuit over injuries, damages, or accidents on your property.

Business income insurance: This covers your lost income if your business operations are interrupted.

BOPs are designed to meet the basic needs of small and medium businesses. Generally, businesses with fewer than 100 employees and less than $5 million in revenue are good candidates for a BOP. However, some industries with high or unique risks, such as restaurants, may need to purchase a custom bundle or individual policies instead of a BOP.

Even if your business is a good fit for a BOP, you may still need to purchase standalone policies to cover risks that the BOP does not address.

SMALL BUSINESS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

Additional Small Business Insurance Options

Standalone policies that small businesses may need outside of a BOP include:

Professional liability: In some states, professional liability is required for certain professionals (like doctors or lawyers), but it’s recommended for any business that provides guidance or services that may result in losses for clients. Also known as errors and omissions insurance, it can help cover claims that you’re liable for. For instance, if you’re a doctor and a mistake causes a patient to undergo more extensive surgery than they would have otherwise, professional liability insurance can help cover your legal costs if the patient sues and pay for damages if you’re found liable.

Workers’ compensation: This insurance can help cover an employee’s income and medical expenses if they’re injured or fall ill at work. It may also limit their ability to sue your business for the injury. Workers’ comp is regulated by states and is commonly required, though not always. If one of your employees trips at work, injures their back, and needs time off to recover, workers’ comp can help cover their medical expenses and lost income. If an employee suffers a fatal injury while working, workers’ comp may pay benefits to their designated recipients.

Commercial vehicle: Also known as business vehicle insurance, this can help cover injuries and damages caused by auto accidents involving vehicles your business owns, rents, or leases. Most states require you to carry liability insurance for bodily injury and property damage, plus underinsured/uninsured motorists. Say that one of your employees is rear-ended in your company’s vehicle while on a service call. Your commercial vehicle insurance can help cover that employee’s medical bills and the repairs to your company’s vehicle.

Group insurance or employee benefits: This coverage bundles health, life, and short- and long-term disability coverage for your employees into one package. Some of these benefits are required by law, like disability and health insurance, but it varies by the number and classification of your employees. If one of your full-time employees suffers an injury that prevents them from working for three months, the short-term disability offered by your business can help cover part of their salary until they’re able to work again.

How Much Does Small Business Insurance Cost?

The cost of your small business insurance depends on factors like the size of your business, its location, and materials used in your business, plus the level of coverage you want.

A strip mall bakery might only pay $200 a month, whereas a chainsaw-carving wood sculpture operation could pay $2,000 a month. Basically, the safer and smaller your company, the more affordable your small business insurance is likely to be.

How Can I Save With Small Business Insurance Discounts?

Discounts for small business insurance can help lower your ongoing costs, and can generally be divided into four major types.

Safety discounts: These may be applied if you take steps to help keep your employees and assets safe. This includes things like installing burglar alarms, upgrading your fire alarm system, and providing ergonomic equipment and quality safety gear for your employees.

Bundling discounts: If you buy multiple types of insurance from the same company, they may offer a discount for those policies.

Group discounts: It’s common for an insurance company to specialize in a business niche, like farms or grocery stores. If your business is part of that niche, that insurance company may offer you special discounts.

Loyalty discounts: Insurers reward customers who stick around. You might also get discounts for referring friends, family, and colleagues to your insurance company.

Discounts are given at the insurer’s discretion. If you operate in a risky industry, it may be harder to find discounts.

Small Business Insurance FAQs

Insurance requirements often vary by state, industry, and the size of your business. Workers’ compensation, health insurance for full-time employees, and commercial vehicle insurance are some policies that are commonly required. A local independent insurance agent can help ensure you have all the coverage you need.

A serious accident, lawsuit, or even fire could cause significant financial damage to a small business. The right insurance acts as a safety net, minimizing the damage from a covered event. Without it, you could pay out of pocket for major events, potentially bankrupting your business and disrupting your income.

With the right blend of liability and property coverage, you can help make sure your small business continues to thrive.

Hazard insurance may not be legally required by state law, but it could be required by your mortgage lender. Even if it’s not, it may be worth purchasing to help cover costs from frequent risks.

A business owners policy, or BOP, is insurance coverage designed specifically for small businesses. A BOP combines several types of insurance in a convenient package and can be customized to suit any particular business. Generally, this policy includes property, liability, and loss of income coverages.

The cost of small business insurance varies from situation to situation. Different factors like your industry, business size, and desired coverage limits affect your small business insurance rates. For example, a gift and stationary shop in a strip mall would likely pay less than a firework store off the highway. The typical cost for BOP is around $100 per month.

In general, forming an LLC helps protect your personal assets from being tied to your business, but it doesn’t protect your business assets and personal income from being affected if a fire, lawsuit, or natural disaster occurs. The right coverage can help protect you and your business from financial damage.

Some of your property may be covered under your home insurance, but it's limited. If you're running a home business, you'll need business equipment protection, liability coverage, and more.

Every state has its own requirements for workers' comp. Even if it’s not legally necessary in your state, if you have a workforce on the payroll, you should protect yourself, and your employees, with workers' compensation insurance.

With the general liability coverage provided by a BOP, your business will be protected from most common lawsuits, like customer property damage, injuries, and copyright complaints. If you have employees, vehicles, or offer services that can harm a client if done incorrectly, you may need more coverage. Your independent agent can help identify any important liability coverage gaps.

Yes, small business insurance is generally tax deductible, as long as the coverage is deemed ordinary and necessary for your business. Businesses may not deduct their insurance premiums if the coverage is for the purpose of a self-insurance reserve fund or a loss of earning insurance policy. Your tax professional will be able to help answer any tax-related questions you may have.

Owning your own business can be an exciting and rewarding venture, but that doesn't mean it's easy. The key to long-term success, growth, and independence is having the right protection in place. An independent insurance agent can help you find the best business insurance coverage to protect you from whatever may come, all at the perfect price for your budget.

Your Independent Insurance Agent Has Your Answers for All Things Related to Small Business Insurance

Last year alone, insurance providers in the U.S. covered $184 billion in claims for businesses. With an independent insurance agent, you can find the right small business insurance policy to make sure you’re covered, too.

At Trusted Choice, our agents take the time to discover your business’s unique risks and needs, matching you with a policy that works for your business and your budget.

Best Business Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.