How to File for Work Comp

(And why you need to know)

Candace Jenkins is a licensed insurance advisor with over a decade of experience. She is also a writer and loves to write on all things insurance. Candace writes for TrustedChoice.com on a continuous basis and is here with the facts about all your insurance inquiries.

As an employer, it is your duty to obtain workers' compensation insurance to better protect you and your employees. But knowing how and when to file a workers' compensation claim can be tricky if you've never done it before.

Your independent insurance agent is a fountain of knowledge when it comes to workers' compensation claims. They know just how to handle them and how to keep handling them once the claim is filed. There are a few things you should really be aware of as an employer when it comes to workers' compensation. Diving in has been a great motto for many.

What Does Your Workers' Compensation Policy Cover?

What your workers' compensation policy covers is a big deal. The answer is medical expenses arising from the following:

- Physical injury

- Mental illness as a result of problematic working conditions

- Illness as a result of problematic working conditions

Who pays the employee's wages while they're out?

You may be wondering if you, as the employer, are responsible to cut your injured employee a paycheck while they are out on a workers' compensation claim. Your workers' compensation policy usually covers two-thirds of employee wages when they are on leave. If you decide to make up the difference as the employer, well that's up to you.

How the Claims Process Works, Exactly

When filing a workers' compensation claim, it's important to know how the process will take place. A good independent insurance agent will already be ahead of the game and will have gone over this with you prior to a claim taking place. But just in case you haven't found your agent yet, here's how it goes.

- Report claim to an independent insurance agent

- Agent reports to the insurance carrier

- Insurance carrier assigns an adjuster

- An adjuster gathers all the facts from all parties

- The adjuster reports facts to insurance carrier

- The insurance carrier makes final decision if the claim falls within their policy form

- Insurance carrier either approves or denies the claim

- If claim is approved, the claimant will be given funds to pay for medical expenses associated with the claim along with lost wages and even disability if applicable

Where to Get Answers for Filing a Claim

So glad you asked! Filing a claim doesn't have to be a horrible experience. In fact, it's what insurance is for, and it should really be your agent's and your insurance company's time to shine. That being said, the best place to get answers well answered is through your independent insurance agent. When dealing with the claim, they are the go-between and know how each party operates. Thus they can smooth things over and present claims in a good light.

An independent insurance agent is your knight in shining armor when it comes to claim time, and they are prepared to answer your questions. No business owner wants to be handling a claim through a 1-800 number or dealing with an insurance adjuster by themselves. It's time to bring in the experts, and your agent is just that.

Save on Workers' Comp Insurance

Our independent agents shop around to find you the best coverage.

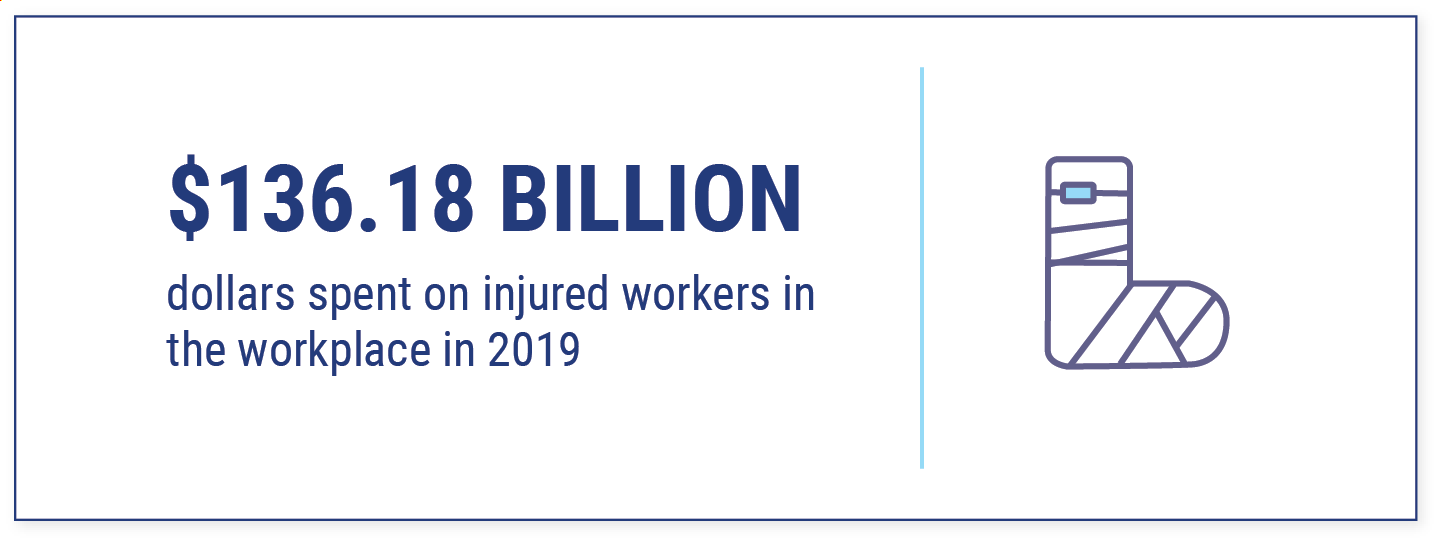

Number of Workers' Compensation Claims

In the USA alone there were $136.18 billion dollars spent on injured employees in the workplace in 2019 according to a recent study. That's billion with a "b." Talk about a lot of Benjamins, and unless you want to be on the receiving end of that bill, adequate coverage is a must. Your independent insurance agent can help, so let them.

Failure to File a Workers' Compensation Claim

But what if you forget? Well, don't, just don't. Failing to file a workers' compensation claim could result in consequences you may not be prepared to deal with. Denial of a claim for filing too late, a lawsuit between you and your injured employee, and even dropped workers' compensation coverage can result if you fail to file a claim.

Now if you misfile or misrepresent an insurance claim, that's on a whole other level. That can cross the line right into insurance fraud and you don't want to be responsible for that. Considering fraud is a legal offense, you will now have the government to deal with, and that's just not worth the risk.

Workers' Compensation Insurance Fraud Laws

Insurance fraud is a big deal. Filing a claim that isn't real or has been manipulated all in an effort to get a large payout from the insurance company should be taken very seriously mainly because it lacks integrity, but also because the consequences could be dire to you, your employee, and your business.

Some insurance fraud consequences:

- Penalties and fines ranging from hundreds to thousands of dollars

- Jail time from one year to thirty years

The result of filing a faulty workers' compensation claim and being caught isn't worth the risk. An employee can file a false claim wanting a payout for an injury or exaggerated illness. An employer can misclassify an employee to avoid them filing a claim in the first place, and a healthcare provider can extend the injury or illness to continue getting payment from an insurance company. As the employer, you set the stage. And by setting up proper safety practices and a clean claims reporting process, you can help curb the chances of false claims being filed.

How to File a Workers' Compensation Claim

There's nothing that can throw a hitch in your giddy-up more than when an employee gets injured and you don't know what to do next. Having a step by step process for claims handling can be your saving grace and something your trusted advisor can help you put together. Going over the steps is, well, smart.

Steps for filing a workers' compensation claim:

Step 1: Get your injured employee the medical treatment they need. If it is an emergency, call an ambulance, if it's a visit to the ER or minute clinic, let them go be tended to right away.

Step 2: Secure the area where the claim occurred to avoid any future injuries.

Step 3: Call your independent insurance agent and report the date, time, employee name and social security number, and what took place.

Step 4: Wait for the assigned adjuster to call you and your employee within a 24-hour period of time. If you have not heard from an insurance adjuster within 24 hours, call your agent and have them handle this with the carrier.

Step 5: Be in constant contact with your independent insurance agent and your employee to make sure the claim is progressing, and to stay apprised of the employee's medical condition.

Step 6: Have you and your agent go through your safety practices to avoid any future claims throughout your company, and be proactive in risk management.

Step 7: If your injured employee cannot come back at full capacity but they can do light-duty work around the office until they are back up and running, then get a return-to-work program in place ASAP.

What's Covered under a Workers' Compensation Policy?

It's good to know the basics of what's covered under a workers' compensation policy. The more you know, the better off you are. Leaning on your independent insurance agent as a resource is also very beneficial, but as a business owner you should also know the gist and it goes something like this.

The basics are like this for a workers' compensation policy:

Coverage limit amount per occurrence for bodily injury

Coverage limit amount per employee for bodily injury by disease

Coverage limit amount policy limit for bodily injury by disease

Put it all together and it looks something like this: $100,000 per occurrence/$100,000 per employee/$500,000 policy limit

By the way, the $100,000/$100,000/$500,000 are the bare minimum basic statutory limits that are typically required by law for every employer or independent contractor to carry.

What Is Not Covered?

By now you should have a pretty good understanding of what a workers' compensation insurance is and how to file a claim. But you should also be aware of what it's not going to cover. A good place to start is with a workers' compensation policy as a whole.

What's not covered under a workers' compensation policy:

- Full wages (this is lost income, and it will only cover partial usually up to two-thirds of regular pay)

- Non-work related injury or illness (this is crossing the line into insurance fraud which is discussed next)

- Coverage more than what is offered on the policy (once your policy limits are exhausted for any one claim, that's it, there is no more coverage and it has officially become a personal problem)

Benefits of an Independent Insurance Agent

Independent insurance agents have access to multiple insurance companies, ultimately finding you the best coverage, accessibility, and competitive pricing while working for you. And as your company grows and your needs change, they'll be there to help you adjust your coverage, up or down, to make sure you're properly protected without overpaying. Find an independent insurance agent in your community here.

https://www.statista.com/statistics/711311/direct-costs-of-top-disabling-workplace-injuries-in-the-us/