Minimum Work Comp Premium Policy

(What is it and how does it work?)

Candace Jenkins is a licensed insurance advisor with over a decade of experience. She is also a writer and loves to write on all things insurance. Candace writes for TrustedChoice.com on a continuous basis and is here with the facts about all your insurance inquiries.

There are minimum premium workers' compensation insurance policies, so no matter which way you cut it, you'll owe something regardless of the coverage amount. Knowing exactly what that means for your business is crucial to calculating the numbers on your bottom line.

An independent insurance agent is a key advisor for every business owner when it comes to workers' compensation insurance and how minimum premiums work. Having an agent in your corner with the best options is as good a place to start as any.

What Is Workers' Compensation Insurance?

First things first. You need to know what workers' compensation insurance is before you can know the laws that govern it. Workers' compensation insurance is an insurance policy taken out by an employer or independent contractor that will help pay for medical expenses of an injury or illness that occurred while working or as a result of an employee's job.

This policy will also pay for partial wages, usually up to two-thirds, for any employee, included owners, or independent contractors while they're recovering. An independent insurance agent is the perfect resource to have when it comes to knowing the ins and outs of workers' compensation coverage.

What Is a Workers' Compensation Minimum Premium?

What minimum premium means in workers' compensation terms is it's a minimum premium that is imposed by the insurance companies {and sometimes the states} on a business owner who may have very minimal coverage due to being a smaller business with fewer risk factors than others.

The insurance companies will require a minimum after a certain threshold of coverage. The typical minimum premiums vary and are dependent on carrier guidelines and state laws. But for the most part, the most recent workers' compensation minimum premiums are typically around $750 annually.

What Does Minimum Premium Policy Cover, Exactly?

Understanding what a minimum premium policy covers can be beneficial to know as a business owner. Although your independent insurance agent will and can advise on such matters, having a good knowledge of what your policy covers is just good practice.

In the world of workers' compensation minimum premiums, you are required as the business owner to pay no less than the minimum premium stated on the policy. If something should happen during the course of the policy term and you are no longer in need of the workers' compensation policy, you are still required to pay the full minimum premium amount agreed to.

This "rule" may sound unfair or even annoying, but it's in place for good reason. The amount of money it costs to write a policy, utilize an underwriter, and billing cycle set up all costs money. Money that the insurance company would likely foot if the policy was taken out and then canceled a short time after. The coverage is still pretty standard and is also dependent on carrier offerings, but a good explanation and example of coverage is below.

The basics are like this for a workers' compensation policy:

- Coverage limit amount per occurrence for bodily injury

- Coverage limit amount per employee for bodily injury by disease

- Coverage limit amount policy limit for bodily injury by disease

Put it all together and it looks something like this: $100,000 per occurrence/$100,000 per employee/$500,000 policy limit

By the way, the $100,000/$100,000/$500,000 are the bare minimum basic statutory limits that are typically required by law for every employer or independent contractor to carry.

Save on Workers' Comp Insurance

Our independent agents shop around to find you the best coverage.

What Is Not Covered?

By now you should have a pretty good understanding of what a minimum premium policy is and the typical coverage. You also need to be aware of what it's not going to cover. A good place to start is with a workers' compensation policy as a whole.

What's not covered under a workers' compensation policy:

- Full wages (this is lost income, and it will usually only cover up to two-thirds of regular pay)

- Non-work related injury or illness (this is crossing the line into insurance fraud which is discussed next)

- Coverage more than what is offered on the policy (once your policy limits are exhausted for any one claim, that's it. There is no more coverage and it has officially become a personal problem.)

It's important to remember that even if your policy is canceled shortly after inception (even a day after), the minimum premium due will still apply. What is happening in the industry is some business owners or 1099 workers have been required to provide workers' compensation coverage to obtain a specific job or contract by a third party. Some insureds have taken out a policy and then decided to cancel right after providing proof of insurance to the requestor.

Some ways that the insurance companies and states have safeguarded themselves from losing money is to require the minimum premiums, and most of the time up front. Another way that the third party has protected themselves from obtaining false insurance certificates where the coverage is not active, is to require an endorsement be added to the workers' compensation policy that informs the third party of cancellation within 30 days.

Workers' Compensation Insurance Fraud Laws

Insurance fraud is a big deal. Filing a claim that isn't real or has been manipulated all in an effort to get a large payout from the insurance company should be taken very seriously mainly because it lacks integrity, but also because the consequences could be dire to you, your employee, and your business.

Some insurance fraud consequences:

- Penalties and fines ranging from hundreds to thousands of dollars

- Jail time from one year to thirty years

The result of filing a faulty workers' compensation claim and being caught isn't worth the risk. An employee can file a false claim wanting a payout for an injury or exaggerated illness. An employer can misclassify an employee to avoid them filing a claim in the first place, and a healthcare provider can extend the injury or illness to continue getting payment from an insurance company. As the employer, you set the stage. And by setting up proper safety practices and a clean claims reporting process, you can help curb the chances of false claims being filed.

Cost of Workers' Compensation Minimum Premium Policies

Just like any insurance policy, workers' comp costs vary. It's a vast numbers game when it comes to risk factors and industry types concerning workers' compensation insurance. The only true way to know is to have your agent run the numbers on your business and its specifics. While it's nearly impossible to know what your individual workers' compensation premium will be, here are some determining factors you can look out for.

Workers' compensation price-determining factors:

- Industry: This plays a big part in the cost of your workers' compensation premium. The riskier your business, the more your premiums will be.

- Number of employees: This determines how much your rates will increase. More people equal more money.

- Gross annual payroll per employee type: Each employee is given a classification code that classifies their job duties and then charges the premium according to how risky or not risky their tasks are. The amount of money you pay them will determine the amount of premium per classification code. The more payroll, the more premium you pay.

- Experience modification rating: If your business has had workers' compensation insurance for a total of three years or more, and you are paying over $5,000 in annual premium, then you'll be assigned an experience modification rating, aka "mod." This mod will adjust throughout the years depending on the number, length, and frequency of claims turned in. The better the mod, the better rate you will receive. It's kind of like a credit score for your workers' compensation policy.

What Is the Benefit of Having Enough Coverage?

The benefits of enough coverage far outweigh the costs involved. With minimum premium policies, you may have statutory minimum limits or less coverage than you actually need. Having a knowledgeable independent insurance agent who can properly advise on how much coverage you should obtain is essential to running a protected operation.

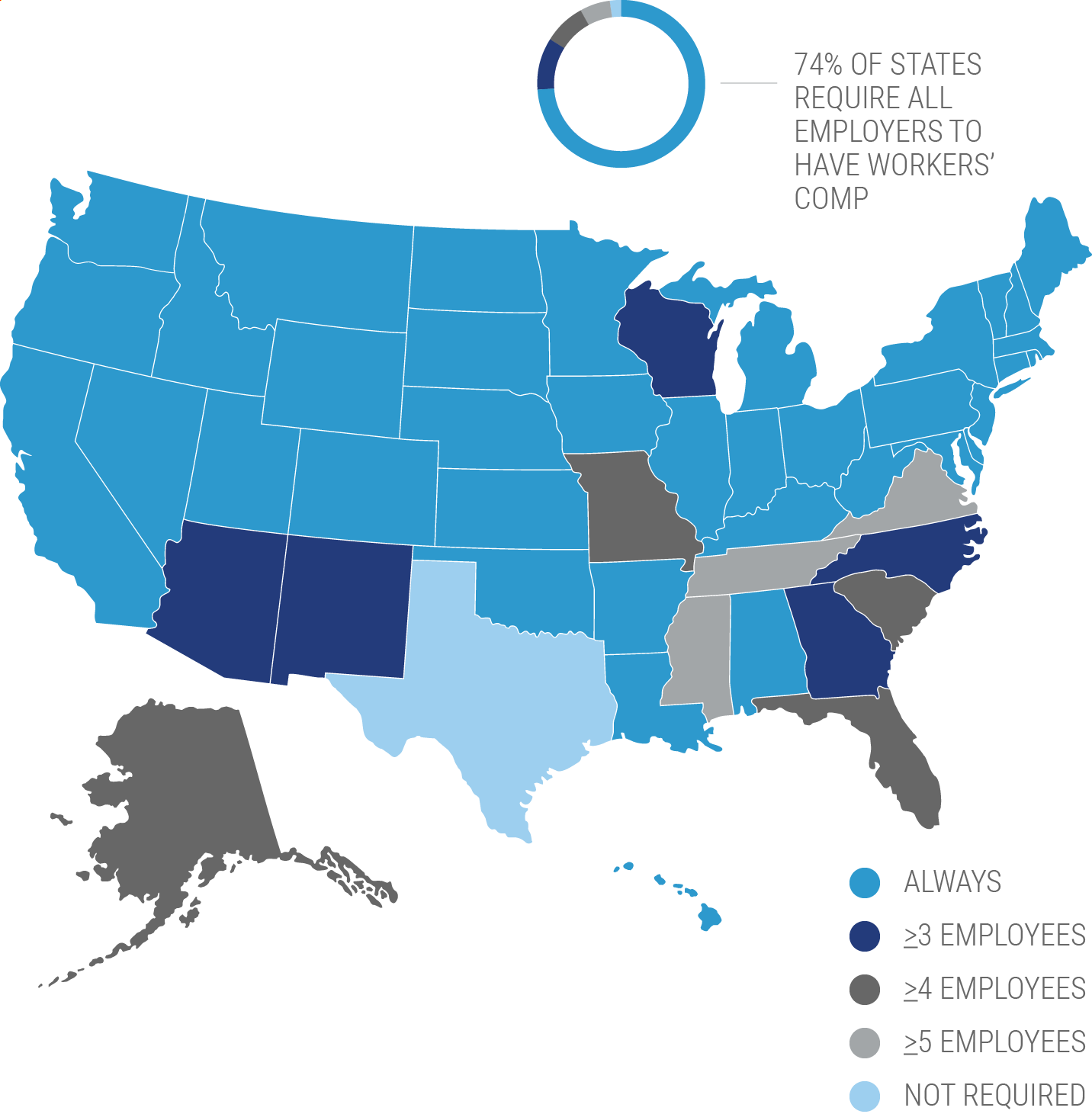

Is Minimum Premium State-Specific?

Minimum premium policies can be state-dependent, meaning it depends on what the state allows in its workers' compensation laws and guidelines. Each state has its own rules when it comes to workers' compensation insurance and thus they have their own state minimum premium requirements. If you obtain your policy from a private sector like an independent insurance agent, then the insurance companies set the minimum premium requirements.

Usually there are not additional forms or endorsement add-ons associated with a minimum premium policy because the coverage is minimum most of the time and pretty basic. But to be sure, checking with your agent on your state specifics will set you on the right track.

Benefits of an Independent Insurance Agent

Independent insurance agents have access to multiple insurance companies, ultimately finding you the best coverage, accessibility, and competitive pricing while working for you. And as your company grows and your needs change, they'll be there to help you adjust your coverage, up or down, to make sure you're properly protected without overpaying. Find an independent insurance agent in your community here.