Rhode Island Work Comp Laws

(What every business owner needs to know for the sake of their employees and their business.)

Candace Jenkins is a licensed insurance advisor with over a decade of experience. She is also a writer and loves to write on all things insurance. Candace writes for TrustedChoice.com on a continuous basis and is here with the facts about all your insurance inquiries.

Knowing the laws and requirements surrounding workers' compensation is essential to running a smooth operation. Rhode Island has its own rules when it comes to workers' compensation, and obtaining coverage when you have just one employee on the payroll is one of them.

An independent insurance agent can help sort through all the facts when it comes to your state-specific laws. All agents have done their market research and are licensed to provide workers' compensation coverage through multiple carriers to make sure you're heading in the right direction.

What Is Workers' Compensation Insurance?

First things first, you need to know what workers' compensation insurance is before you can know the laws that govern it in Rhode Island. Workers' compensation insurance is an insurance policy taken out by an employer or independent contractor that will help pay for medical expenses for an injury or illness that occurred while working or as a result of an employee's job.

This policy will also pay for partial wages, usually up to two-thirds, for any employees, including owners or independent contractors, while they're recovering. Almost every state mandates workers' comp coverage in some form or fashion, and an independent insurance agent is the perfect resource to have when it comes to knowing Rhode Island's state-specific guidelines.

Rhode Island's State Workers' Compensation Insurance Requirements

What Rhode Island requires for workers' compensation coverage could mean the difference in some serious penalties and back-charged premiums from your state government. Not to mention the legal consequences involved if you're found non-compliant. It could also mean a hefty lawsuit from one of your employees if you're caught skimping on the proper workers' compensation protection.

Having the right protection in place is an important part of your business operations, and not having a policy in place could leave you open to financial burdens that no company wants to bear, like:

- Employee medical expenses

- Employee lost wages

- Legal fees

In the state of Rhode Island, workers' compensation insurance is mandatory if you have one employee. An independent insurance agent can get more in the weeds with you when it comes to your state's specifics concerning workers' compensation insurance and any other commercial insurance. Keep in mind that your independent insurance agent will have the most current information as it pertains to your business and the state in which you reside.

Rhode Island's Workers' Compensation Insurance Laws

Each state looks a little different when it comes to workers' compensation coverage and when you are required to obtain it as a business owner. But in Rhode Island, you must acquire workers' compensation insurance once you have just one employee hired with very few exceptions, and harsh penalties if you neglect to get the proper coverage.

Penalties for not having proper workers' comp coverage in Rhode Island:

- Stiff financial penalties

- Being charged with a misdemeanor

- Being charged with a felony

- Being imprisoned

An independent insurance agent can be exactly what you need when you're looking for coverage to help you avoid the trouble of being sued personally by your injured employee. Just call it the cost of doing business and move on fully protected without the burden of a potential lawsuit to worry about.

Save on Workers' Comp Insurance

Our independent agents shop around to find you the best coverage.

Rhode Island's Workers' Compensation Insurance Fraud Laws

Insurance fraud is a big deal. Filing a claim that isn't real or has been manipulated in an effort to get a large payout from the insurance company should be taken very seriously. Mainly because it lacks integrity, but also because the consequences could be dire for you, your employee, and your business.

Some insurance fraud consequences:

- Penalties and fines ranging from hundreds to thousands of dollars

- Jail time of from one year to thirty years

The result of filing a faulty workers' compensation claim and being caught isn't worth the risk. An employee can file a false claim wanting a payout for an injury or exaggerated illness. An employer can misclassify an employee to avoid them filing a claim in the first place. And a healthcare provider can extend the injury or illness to continue getting payment from an insurance company. As the employer, you set the stage. By setting up proper safety practices and a clean claims reporting process, you can help curb the chances of false claims being filed.

Workers' Compensation Insurance Companies in Rhode Island

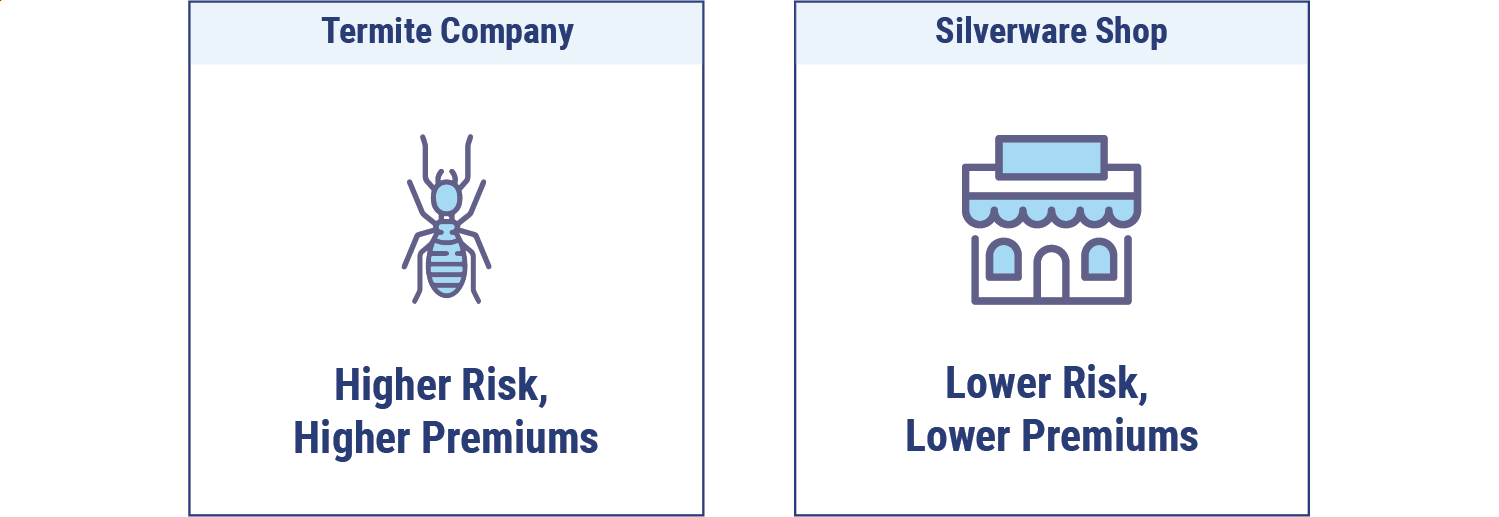

Rhode Island has a number of different insurance companies that would be more than happy to write a workers' compensation policy for your business. The real deciding factor is what industry you are in. The riskier your business operations, the fewer carrier options you may have and the higher premiums will be.

If you have a termite extermination company and your employees are spraying chemicals all the livelong day, your workers' compensation premium will be one of the highest premiums in the business. Because your chances of filing a claim are high and the claims payout for this industry is also high, the insurance companies charge more moolah to insure.

If you own a silverware shop and your employees are selling fine dinnerware and greeting customers, then you will have one of the lowest workers' compensation premiums on the market, because your business just isn't that risky. All in all, the selection of insurance companies in your state is plentiful. But it may be a different story in your industry, depending on the insurance carrier's appetite.

Some states are monopolistic in their ruling, meaning they require you to obtain insurance through their state programs and only their state programs. The four states that adopted this state-funded workers' compensation program are: North Dakota, Ohio, Washington and Wyoming.

Self-Insured Workers' Compensation in Rhode Island

Some states allow a business owner to self-insure. All this means is that you, as the business owner, agree to file an exemption through the state channels that declares you're insuring any and all workers' compensation claims internally.

This is a risky move even if you have deep pockets. It puts your business in jeopardy of financial ruin if a claim gets big enough. And in a world where you're only as good as your worst employee, taking on that kind of gamble is something to consider carefully.

Luckily, your independent insurance agent is an expert at these types of things, and can tell you if your state will allow self-insurance and discuss the repercussions of such a move. All in all, it should be discussed with a trusted adviser before making any long-term commitments.

Rhode Island's State Workers' Compensation Benefits

Benefits in Rhode Island are determined by the employer, independent insurance agent, and carrier offerings. State minimum limits for workers' compensation are pretty universal.

| Workers' compensation state minimum limits: |

| $100,000 per occurrence for bodily injury: This coverage is for any one employee. |

| $100,000 per employee for bodily disease: This coverage is for any one employee. |

| $500,000 policy limit for injury by bodily disease: This coverage is the total per policy term for all claims in a policy term. |

Most independent insurance agents agree that you should always go with higher limits than the statutory minimum. $100,000 can be blown through pretty quickly when a decent-sized injury is involved, especially when hazardous chemicals are involved. And the person responsible for the medical care after those limits are exhausted is you, the employer.

How Long Can You Collect Workers' Compensation in Rhode Island?

Workers' compensation in Rhode Island can normally be collected and paid out until the patient is recovered and discharged from medical care. This is based on the physician's recommendations for the patient's care and recovery. An independent insurance agent can help with the claims process and make sure all parties are communicating so there is a timeline for treatment and care.

Who Is Exempt from Workers' Compensation in Rhode Island?

If your business is just you, you really shouldn't have to worry about getting workers' comp coverage. In fact, most owners exclude themselves and simply use their health insurance if they get injured on the job.

However, if you have one or more employees on staff, workers' comp is mandatory. But there are a couple of exceptions to the rule. And some industries are exempt from having coverage, like:

- Domestic or household workers

- Musicians

- Employees who are federally covered

- Railroad workers

- Dusting or spraying airplane workers

- Non-profit uncompensated workers

- Real estate brokers or agents

- Land workers

Exempt or not, the bottom line is that it just makes good, plain sense to protect yourself and your business from a potential lawsuit. And, unfortunately, they do happen. Discussing your options and whether you're exempt with an independent insurance agent is a good place to start, since they know all the ins and outs of workers' compensation laws and regulations.

What's the Cost of Workers' Compensation in Rhode Island?

Well, it varies— just like any other state or insurance policy, for that matter. It's as vast as the number of industries in the world, and the only true way to know is to have your agent run the numbers on your business and its specifics. While it's nearly impossible to know what your individual workers' compensation premium will be, here are some determining factors you can look out for.

Workers' compensation price-determining factors:

- Industry: This plays a big part in the cost of your workers' compensation premium. The riskier your business, the more your premiums will be.

- Number of employees: This determines how much your rates will increase. And more people equals more money.

- Gross annual payroll per employee type: Each employee is given a classification code that classifies their job duties and then charges premium according to how risky their tasks are. The amount of money you pay them will determine the amount of premium per classification code. The more payroll, the more premium you pay.

- Experience modification rating: if your business has had workers' compensation insurance for a total of three years or more, and you are paying over $5,000 in annual premium, then you'll be assigned an experience modification rating, aka "mod." This mod will adjust throughout the years depending on the number, length, and frequency of claims turned in. The better the mod, the better rate you will receive. Kind of like a credit score for your workers' compensation policy.

How to Apply for Workers' Compensation Coverage in Rhode Island

As a business owner, knowing who to get workers' compensation insurance from can be a bit confusing if you're not familiar with your state requirements. Sure, you can just Google it, or ask around, but who knows what you're going to get? With an independent insurance agent, you get a local Rhode Island state expert who shops multiple companies to bring you the best coverage and rates for your business. It's really as simple as it gets.

Getting workers' compensation coverage with an independent insurance agent goes like this:

Step One: Find a trusted independent insurance agent.

Step Two: Go over your business details such as employee demographics, payroll and daily operations for proper classification of workers on your workers' compensation policy.

Step Three: Your independent insurance agent will take your information to several insurance carriers and let the offers pour in on coverage and rates.

Step Four: You and your independent insurance agent decide on your best option as it applies to your specific situation and go with a carrier that you decide upon.

Step Five: Enjoy the freedom of working with a trusted adviser and having them handle all your workers' compensation insurance needs.

Following these five simple steps will ensure that you're on the road to a more protected future as a business owner, giving you appropriate coverage quickly and when you need it.

Rhode Island's Workers' Compensation Claim Eligibility Requirements

In order to be eligible for a work comp claim, you need to be able to prove the facts. As a business owner, having proper safety protocols in place for your employees is the first step. The next is to have a clear-cut workers' compensation claim reporting process that both you and your independent insurance agent agree upon.

To determine if a claim will process and pay out benefits, the insurance companies like to make sure they aren't being taken for a ride, so to speak. Having a streamlined process will help make for a faster, and more accurate, claims result. In the end, it's down to the adjuster assigned to the claim and the insurance company to determine if a claim fits into their policy form. Time is of the essence, so be sure to report any claims activity within the first 24-hour period.

Benefits of an Independent Insurance Agent

Independent insurance agents have access to multiple insurance companies, ultimately finding you the best coverage, accessibility and competitive pricing while working for you. And as your company grows and your needs change, they'll be there to help you adjust your coverage, up or down, to make sure you're properly protected without overpaying. Find an independent insurance agent in your community here.

Rhode Island Department of Labor and Training. (2019). http://www.dlt.ri.gov/wc/