Alaska Hotel Insurance

So you can keep the tourists in and the risks out.

Insurance doesn’t have to be boring. That’s why we hired Sara East to be our BA insurance writer. Maggie specializes in making mundane subjects hella-entertaining.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

Somewhere in the world a traveler is planning on taking a dog sled ride, spotting a grizzly bear, and taking in the pristine beauty of the national parks in The Last Frontier. They’re going to need somewhere to stay when they get to Alaska, and they’re counting on you to provide a safe and bedbug-free place to sleep. But before you can welcome adventure and nature seekers alike, you’ll need to properly equip your business with hotel insurance.

To make it easy, we’ve gathered all the information you need to make sure your hotel is fully covered for the short, but busy, four-month tourism season in Alaska. Even better, our independent insurance agents can help you find exactly what you need. Whether you’re running a boutique hotel, dude ranch or luxury resort, they’ll set you up with great coverage.

What Is Hotel Insurance?

Put simply, hotel insurance is insurance that’s made to protect all the aspects of your hotel, from the property and employees, to guests, services you offer, and amenities. Of course, most hotels offer different amenities, and the risks associated with your hotel will affect your insurance coverage needs.

What Types of Hotel Businesses Need Insurance?

The easy answer is: all of them. Every business should have its property and employees protected. And in your line of work, dealing with as many customers as you do, it’s extremely important to keep your business going strong. Our independent insurance agents can help all types of hotel businesses, including:

- Premier and full service hotels: These hotels require the most comprehensive insurance packages, due to having such high occupancy spread across several hundred rooms, as well as offering tons of different services and amenities.

- Boutique hotels: With much lower occupancy rates, typically fewer than 100 rooms, and the lack of premier services or amenities (e.g., room service and fitness centers), these hotels carry less risk and don't require quite as much coverage.

- Condo hotels: These high-rise properties consist of rooms typically owned as vacation homes that are rented out for short-term stays. Coverage requirements vary, and are determined by the allotted length of guest stays, how the unit is owned (by an individual or group), and the location of the hotel (which is usually a major city).

- Hotel management companies: Employee benefit strategies that help reduce claim costs and risk management are factors in the coverage needed by these companies.

Save on Hotel Insurance

Our independent agents shop around to find you the best coverage.

Top 5 Hotel Insurance Claims in Alaska

Alaska’s preserved beauty is plenty of reason for people to seek a peaceful vacation there, but the state has its fair share of risks faced by hotel owners.

- Fire damage: One in 12 hotels reports a structure fire annually, resulting in more than $60 million in property damage.

- Frozen pipes/flooding: Winter temperatures in Alaska can drop below -50 degrees. A frozen pipe can lead to flooding and some serious insurance claims.

- Liability claims: Most commonly stolen property and minor accidents like slips and falls, but liability claims extend to any injuries or property damage.

- Data breach: The more information you digitally collect from your clients, the more at risk you are for a cyber breach to obtain credit card numbers and other personal information.

- Business interruption: Regardless of a hotel's location, it's always prone to attacks by Mother Nature. Whether your hotel is nestled in an earthquake zone, avalanche area, or anywhere else, you run the risk of losing precious income no matter what type of natural disaster forces you to temporarily close your doors.

What Does Hotel Insurance Cover?

A hotel insurance policy is typically the easiest route to take when it comes to navigating the right coverage for your business. This package offers most of the liability and property coverage you'll need, and your independent insurance agent can hook you up with any additional coverage your business needs, depending on your scope of services.

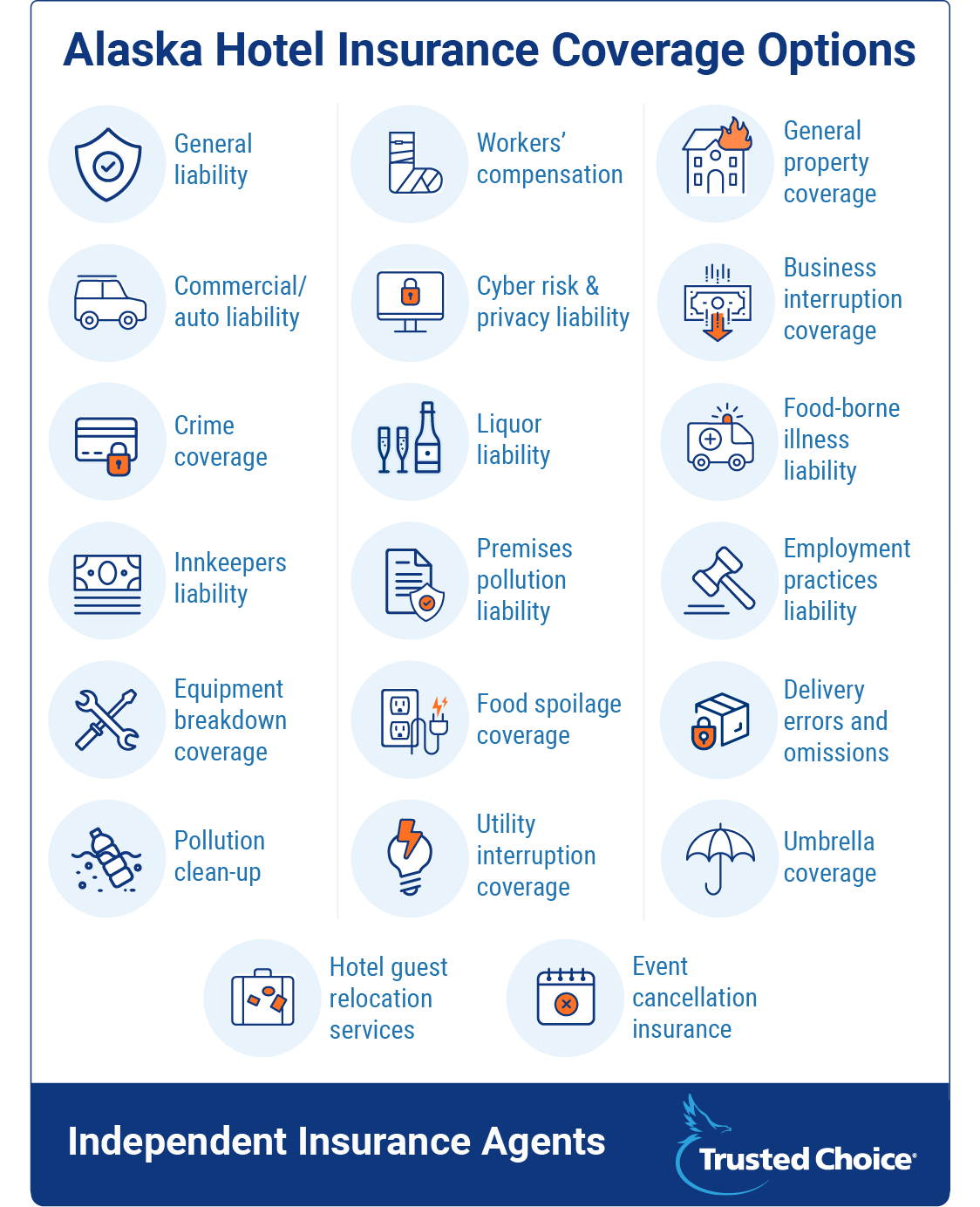

Insurance coverage options for your hotel:

- General liability: If someone gets hurt on your property or damages your property. Experts recommend getting up to $1 million per room in liability insurance coverage.

- Workers' compensation: If your employees become ill, get injured, or die from a work-related incident, this aspect of the insurance will cover the financial ramifications. Coverage is mandatory in Alaska, as well as most other states.

- Property insurance: Protection for the property inside your hotel such as furnishings, electronics, décor, carpeting and amenities. Property insurance limits for hotels are up to $250 million per location.

- Commercial auto liability: Protection for any vehicles that are being used to assist in the daily operations of your hotel.

- Cyber risk & privacy liability: If you have a data breach and your guests' personal information is leaked. Cyber risk and privacy liability insurance limits are up to $2 million.

- Business income/interruption: If your business suddenly has to close, this provides income to help you pay your bills until you reopen.

- Fidelity & crime: Protection if an employee or a guest steals from you.

- Liquor liability: If you serve liquor and a guest gets a little too tipsy from your booze and harms themselves or your property.

- Food-borne illness liability: Protection against food-borne illnesses that guests could receive from in-room or on-property food options.

- Innkeepers liability: Pays for loss or damage to guest property while it is in your possession on the premises of your hotel. Usually the limit is $1,000 per guest.

- Premises pollution liability: If a guest becomes ill as a result of mold or airborne pollutants, this insurance will cover medical bills, fees, and cleanup costs.

- Employment practices liability: Protection against a disgruntled employee taking you to court.

- Equipment breakdown coverage: Funds to repair broken equipment such as kitchen appliances, computers, heaters, etc.

- Food spoilage coverage: If a bunch of your food spoils as a result of an unexpected power outage or equipment failure.

- Delivery errors and omissions: Covers damage caused by failing to deliver or misdelivery of items

- Pollution cleanup: Covers the costs of removing pollutants from land or water on the hotel premises as a result of an event that caused pollution.

- Utility interruption coverage: If you face a major utility outage that results in lost funds.

- Umbrella coverage: Protection for excess liability charges that go above and beyond your policy limits. You can purchase up to $100 million in umbrella insurance.

- Hotel guest relocation services: If you have to relocate your guests because of an on-site hazardous event.

- Event cancellation insurance: If you hold a lot of events and one gets unexpectedly cancelled, this will cover lost revenue.

The limits associated with some of the coverages is the maximum amount an insurer will pay to repair or replace the property. That’s an important thing to keep in mind when building your hotel insurance package.

How Much Does Hotel Insurance Cost in Alaska?

Short answer? It depends. On a lot. An older inn near the coast might pay around $5,000/year. But a fancy high-rise hotel just a few miles away might pay as much as $1,000,000/year.

To make things even more interesting, if these same two hotels were located just 10 miles further inland, their premiums might drop by half. In another state altogether, further away from the coast, the tiny one might pay $1,200/year, while the big one might pay $150,000/year. Really, it all depends on a (large) number of factors, like:

- The age of the hotel: The older a property is, the more of a risk it is to an insurance company. Newer hotels will get more slack with their premiums. Also, the type of construction, as well as whether the building is up to current state codes, may have been influenced by the time period the hotel was constructed in.

- The location of the hotel: If the hotel is located in a region of the country prone to a certain type of natural disaster, the premium will be much higher. But costs are determined down to the specific community surrounding the hotel (if it's in a safer neighborhood, this will present less risk). Also, every state has marked flood zones in it, and these high-risk areas will have higher premiums.

- The hotel's last update/renovation: The status of the building, as well as its furnishings and security systems, will really influence the cost of coverage. The more up-to-date and up-to-code everything is, the more lenient the cost.

- The number of safety/security features: The more security/safety features a hotel has, the less risk it presents to an insurance company. Hotels with current security systems, as well as safety features like sprinkler systems and handicapped-compliant features, will be favored by an insurance company.

- The age/condition of the roof: Older/more decrepit roofs are a higher risk to the hotel guests and the building itself, and therefore more of a risk to an insurance company.

- The size of the hotel: The square footage of the hotel, as well as the number of rooms, will influence coverage costs. Obviously, more rooms means more guests, which increases liability risk, and therefore means a higher premium.

- If rooms are rented out by other companies: If the hotel has community rooms that get rented out for meetings by other companies, this will increase the liability risk, and therefore costs, as well.

- If there is cooking on the premises: Hotels with kitchens present a risk for fire damage, and hotels with cooking equipment in the guest rooms further increase that risk — by a ton. However, fire safety features in the rooms and kitchen can help to decrease this risk (and cost).

- The parking lot's security: More security features in the hotel's parking lot can reduce the risk of claims filed by guests who experience damage or theft of their vehicles.

- If there is valet parking: Valet parking is another unique feature that increases liability needs, since the guests' vehicles are literally being driven by hotel staff.

- The experience level of the management: Insurance companies are interested in all kinds of details, including how experienced the hotel's managers are. Managers with more extensive training in risk prevention/crisis response can greatly reduce claims made by the property.

- The type/number of recreational features: If a hotel has a pool or a gym, obviously the risk of injury (or even death) increases, creating a need for more coverage.

- If the hotel serves/sells alcohol: If there is alcohol on the premises, liquor liability coverage will be necessary.

- If the hotel has any existing/past claims: Just like with any other type of insurance, if a hotel has any existing/past claims, the cost of coverage will increase.

Save on Hotel Insurance

Our independent agents shop around to find you the best coverage.

Top 5 Ways to Score Hotel Insurance Discounts in Alaska

Preparation and knowledge are a killer mix for saving money on your hotel insurance. Here are just a few ways you can lower the cost of your premium.

- Prepare for risk: Create a risk management plan for your guests and staff and provide this plan to your insurance agent when they’re shopping for your quotes.

- Maintain your roof: A faulty roof can be a massive expense. Keep your roof in top-notch condition and it can save you some bucks on your premium.

- Update your hotel: Old things are more likely to break and more costly to insure. Keep your hotel up to date and within county and state codes.

- Keep safety in mind: Install proper smoke alarms, access points, and elevators, and always strive for proper food handling processes and general organization. These efforts to keep your business and guests safe can save you money.

- Add an indoor sprinkler system: Seeing as fire is one of the top insurance claims for hotels, equipping your hotel with an indoor sprinkler system can reduce your premium.

Compare Hotel Insurance Quotes in Alaska with an Independent Insurance Agent

Whether you need a basic package of general and property liability or add-on policies to cover unthinkable risks, our helpful independent insurance agents can help you put together a hotel insurance package that’s right for you. They’ll compare quotes from a variety of companies and find the most affordable and top-notch coverage available.

https://alaskaserviceagency.com/hotel-motel-insurance/

http://www.alaskajournal.com/2017-06-14/hotels-spring-visitor-numbers-keep-climbing

https://budgetalaska.com/motel-insurance-68.htm