Motorcycle Insurance Quotes

(Our actuaries explain the secret formula)

Christine Lacagnina has written thousands of insurance-based articles for TrustedChoice.com by authoring consumable, understandable content.

You’re finally ready to get yourself some legit motorcycle insurance. Awesome. But before you go all-in on the whole process, just know that finding insurance quotes can be tricky. There's a ton of details and tips to remember with lots of rubbish to sort through.

Our independent insurance agents can make finding the right quotes a total breeze. They'll dig deep, shop savvy, and help you compare options from multiple insurance carriers to find the absolute best coverage for you, at the best price.

They’ll even help translate all the super-confusing insurance jargon and break down the fine print into something the average person can actually understand.

How Motorcycle Insurance Quotes Are Born

Before you dive into getting coverage for you and your bike, you should know how insurance companies come up with those quotes.

- They start off by evaluating a series of risk factors that have number values (costs) associated with them, in a rating manual.

- Risk factors may be things like age, gender, location, etc.—things that could increase the chances of you filing a claim.

- The cost of the risk factors is determined either through studies of historical trends, or via analytical models (basically, super-mathy stuff).

- They'll check off those attributes that apply to you.

- The sum total of everything checked off on the list, plus a bit extra factored in for the insurance company's profit margin, becomes your quote. But, due to competition from other companies, they might lower the price a bit.

NOTE: Quotes are subject to change. The insurance company may gradually increase your premium over time to keep up with the financial demands of offering the coverage.

How to Get the Motorcycle Insurance You Want

Step 1: Understanding Motorcycle Insurance and Why You Need It

- The what: In a nutshell, motorcycle insurance is a simple contract between you and an insurance company. It says you’ll pay them a premium and, in return, they agree to protect you financially if your bike is stolen or involved in an accident.

- The why: Every state has different laws, and three of ‘em don’t require any motorcycle insurance at all. But each of the states that do has different coverage requirements, so talk to your agent about what you'll need in your state. Besides, motorcycle insurance is super-important to protect you from bad stuff like:

- Theft and damage: If some rider's envy gets the best of them and they steal or trash your bike (and it does happen), your coverage can help you get financially reimbursed and back to where you were.

- Property liability: If you’re in an accident and you dent, damage or destroy someone else’s stuff, liability coverage will help you get things right again.

- Medical/Legal liability: In an accident, medical and legal bills can get, like, silly expensive. Liability coverage can help you handle all that.

Better Motorcycle Insurance

Our independent agents shop around to find you the best coverage.

Step 2: Gather All Your Info

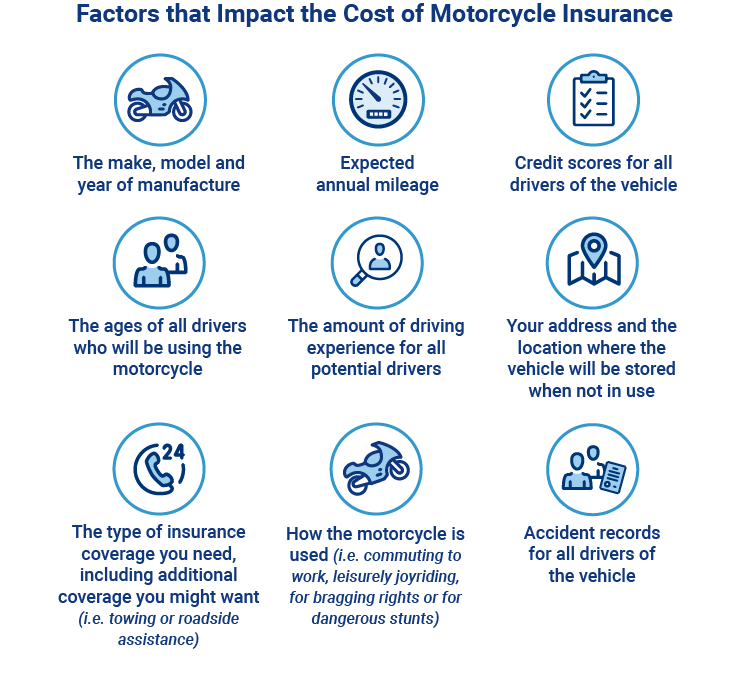

Motorcycle insurance quotes are only as good as the info you provide. Make sure you supply the following deets with franchise QB accuracy (backed up by official documents, of course):

- What kind of bike? You know, the year, make and model.

- How often do you bike? Estimate your annual mileage and how often you ride.

- How do you use the bike? Is it just for work commutes, or do you pop wheelies down the highway at night?

- How old are the bikers? The ages of ALL drivers who will be using the motorcycle.

- How long ‘ya been ridin’? What’s your driving experience like?

- Where’s your bike live? Your address, where ya park it and where you store in the winter.

- What do you need? The type/amount of insurance coverage you’ll need, including additional coverage you might want (i.e., towing or roadside assistance)

- How’s your credit? Credit scores for all drivers of the bike.

- How well do you ride? Accident history for all drivers of the bike.

Step 3: Connect with an Independent Agent

Look, understanding the ins and outs of insurance quotes ain’t easy. And comparing this one to that one and that one over there can be a real mess. You've gotta keep things like pricing, coverages, state requirements, claims process, customer service and reputation in mind.

Here's where an agent can come in and save the day for you, because they do this on the daily and have been through it all, with all sorts of different companies.

An independent insurance agent can make your life a heckuva lot easier during this process. They're not tied down to one insurance company. This means they're free to shop around with multiple carriers to compare and assemble all the pieces of the coverage puzzle for you. How’s that for sweet?

Step 4: Work with Your Agent

Your agent is there just for you. So the more info you can give them about your situation and any concerns you may have will only help you in the end. Here are a few key topics to discuss with your agent to help get the ball rollin’:

- How much coverage you want in each aspect of your policy (e.g., collision, comprehensive, liability and uninsured/underinsured motorist).

- How much you're willing to pay out of pocket towards a deductible.

- Any factors that could “up” the risk factor of your policy (like a history of riding without a helmet, or your tendency to get distracted by shiny objects).

- Ask for any hacks that could help lower your premium (for example, getting a special certification, or storing your bike in a locked garage when not in use).

- Ask for and discuss any deals or incentive payment plans (paying annually vs. monthly).

- How to pick the best coverage for you (this is your policy, after all).

Better Motorcycle Insurance

Our independent agents shop around to find you the best coverage.

Step 5: Tell Them Everything

Absolutely everything. Tell them all the info you might rather gloss over, because inevitably they, or the carrier, will eventually find out. And that won’t be good. Purposely omitting risks to get yourself a lower premium will always come back to bite you in the chaps. So keep these pointers in mind:

- If they do ask, you tell. This honest communication will lead to a perfect premium/risk match in terms of your policy's price (and no biting of any kind).

- If they don't ask, you tell. Don't ignore anything you think is relevant just because it didn't “come up.” The longer your Q&A/confessional segment with your agent, the better your motorcycle insurance quote, and therefore policy, will ultimately be.

The Lowdown on Online Quotes

Look, we know you want quick ‘n easy motorcycle insurance quotes in under a minute. We get it, you want the goods fast so you can move on to other big life thingies. But, choosing supersonic speed could mean sacrificing accuracy and coverage...which could end up costing you a pretty penny in the end.

But wait, there's more. Our competitors might sell your precious info to multiple companies, which could lead to a bunch of unrecognized numbers popping up on your caller ID and a flooded voicemail box.

We turned that whole process on its head, by providing YOU with the info you need to connect with an independent agent when you’re ready.