High profits, customer satisfaction, and technological development are all top-of-mind for business owners and managers. However, business protection should be on that list, too. No matter how successful your company is, business insurance can provide you with a safety net and peace of mind against the potential of a financial crisis.

Learn about the basics of insurance for business – including what it is, why it matters, what coverage options are available, and how to save money on your business insurance coverage.

What Is Business Insurance?

Business insurance refers to a full package of policy options designed to protect businesses from financial loss after unexpected events. A business insurance policy should be tailored to your business’s individual needs, providing coverage for identified risks.

Business insurance policies commonly cover property damage, liability, and employee accidents or injuries. However, additional coverage options are available. Factors like the size of your company, your industry, and related assets (such as company vehicles) will determine the specific coverage you need to mitigate risk and adequately protect your company’s financials.

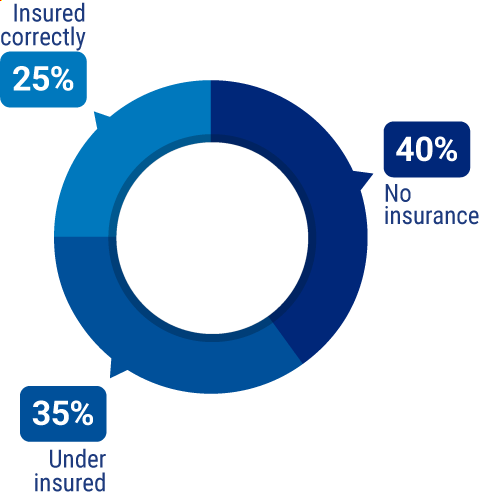

Surprising percentage of underinsured and uninsured businesses

Having inadequate or (worse yet) no business insurance coverage leaves your organization vulnerable to financial risk from events like employee accidents, natural disasters, or cyberattacks that can easily cost your business thousands of dollars. An independent insurance agent can help you identify your coverage needs and find a policy that meets them.

Is Business Insurance Required?

States regulate insurance requirements to protect you, your employees, and your customers in the event of an accident or event. These legal requirements for business insurance focus on a few key forms of coverage, including:

Unemployment insurance: This state-run insurance program may require you to pay unemployment insurance taxes that are used to cover lost wages for former employees under qualifying conditions. If you have employees, you must register your business with the state workforce’s agency.

Workers' compensation insurance: This insurance protects employees and the business in the event of a workplace injury or illness. If you have employees, you are required to carry workers’ compensation insurance in every state except Texas, though requirements vary based on the number of employees.

Professional liability insurance: Some states require specified professionals to carry professional liability insurance, which covers client losses for which you may be found liable. Legal and medical malpractice policies are examples of this type of business insurance.

Disability insurance: Several states require businesses to have partial wage replacement insurance coverage for eligible employees experiencing non-work related injury or illness.

A local independent agent can help you better understand your state’s business insurance laws and help you obtain the coverage you need.

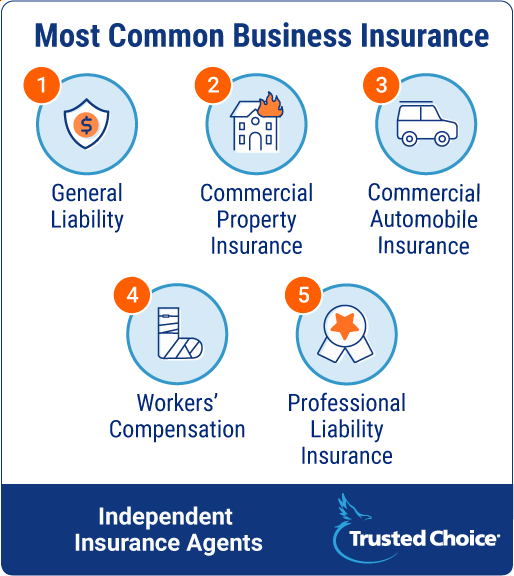

What Does Business Insurance Cover?

Business insurance coverage for a commercial operation typically focuses on the following five key forms of protection:

Commercial property insurance: This covers loss and damage to your commercial business property due to fires, storms, and other causes.

Commercial vehicle insurance: Similar to comprehensive personal vehicle insurance, this policy covers commercial vehicles and drivers for collision, liability, property damage, personal injury, and comprehensive coverage (also known as "other than collision").

Workers' compensation: As noted above, this covers your employees if they get ill or are injured while working on the job.

Depending on your business and its needs, you may require additional business insurance coverage, including:

Product liability insurance: This policy protects you from legal liability regarding faulty products and damage, illness, injury, or death that may occur from using a faulty product.

Loss of income: This policy covers business expenses like rent and employee wages if you can’t operate your business.

Key person insurance: This policy covers loss of income that may result from the head of the business or other key personnel becoming incapacitated or passing away.

Cybercrime insurance: This coverage protects against loss from cyber risks due to Internet use and online communications.

Records retention policies: This is coverage for the loss of important data and financial records.

Specialty coverage: This is targeted coverage that protects against more specific business risks, like those of landlords, farmers, and commercial operations that put on one-day events, like seminars or concerts.

BUSINESS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

How Much Does Business Insurance Cost?

The cost of business insurance varies from one organization to the next. Factors like the type of work performed, the value of assets covered, the number of employees, coverage needed, and your past claims history may impact your rates. Insurance underwriters will also consider your risks in relation to the following:

Fire & natural disasters: The lower your risk of natural disasters like fire, earthquakes, floods, and tornadoes, the lower your premiums may be. Reinforcing your building, relocating to a safer area, and taking proper safety precautions may help reduce your rates.

Theft: If your business deals with valuable items or you're located in a high-crime area, your premiums will go up. Having security features like cameras and guards may help offset this risk.

Hacking: Your business's cyber security is becoming more important every day. Keeping your servers secure and protecting customer data may help you save.

Legal liability: Industries like food service, cosmetics, law, medicine, and travel are particularly vulnerable to lawsuits. Making sure waivers and similar paperwork are in order can help offset costs.

Employee injury: Dangerous employee conditions raise insurance costs, especially for liability and workers' compensation policies. Providing proper safety equipment and implementing crystal clear safety procedures may help lower those costs.

Office and retail businesses aren't as safe as you might think. Consider providing ergonomic equipment and taking steps to prevent repetitive motion injuries.

Customer injury: Do you offer risky experiences like skydives and trail rides to your customers? Those risks raise premiums. Make sure your safety procedures are airtight, such as enforcing helmet and health requirements.

Equipment: If your business's equipment is expensive, dangerous, or difficult to replace, that raises premiums. Well-maintained equipment and clear safety procedures lowers them.

On average, a typical business insurance policy costs around $200 per month. However, different businesses will have different needs and thus, different business insurance expenses. A large construction company with expensive machinery may pay more for its business insurance than a small salon.

If you’d like to save on your business insurance, look for the four main types of discounts and check with your local insurance agent to see if you may be eligible:

Safety discounts: These may be applied if the insurance company sees that you take good care of your commercial property and have special features to help keep your assets safe. This includes installing burglar alarms, sprinklers, a high-quality roof, and more.

Workers' compensation can be an expensive portion of your business insurance, so providing a safe environment for your employees can really save you money. That includes things like ergonomic desks and high-quality personal protective equipment.

Bundling discounts: These are discounts you may get if you buy multiple types of insurance with the same company. Say you need to insure your personal car and your business. If you purchase both insurance policies through the same company, they may offer you discounted rates.

Group discounts: These discounts may be offered to businesses in a specific sector or industry that the insurance company specializes in, such as farming or construction.

Loyalty discounts: Insurers reward customers who stick around. You might also get discounts for referring friends, family, and colleagues to your insurance company.

Ultimately, business insurance discounts are given at the discretion of the insurance company. Insurers may be more likely to offer discounts to businesses in low-risk industries that have a positive claims history.

Business Insurance FAQs

Business insurance refers to a suite of insurance coverage options that are designed to protect businesses from financial loss due to adverse events, such as workplace injuries or natural disasters.

Different businesses have different risks. Business insurance policies should be tailored to meet each organization’s unique risks and coverage needs.

The cost of business insurance varies from one business to the next. Factors like the size of the company, the number of employees, the value of covered assets, and the risk of the work being performed can influence insurance costs. The average business insurance policy costs around $200 per month.

Business insurance is tax deductible, as long as the coverage is for the purpose of operating a business, profession, or a trade. Businesses may not deduct their business insurance premiums if the coverage is for the purpose of a self-insurance reserve fund or a loss of earning insurance policy. Your tax professional will be able to help answer any tax-related questions you may have.

Business insurance is regulated at the state level, so requirements for coverage will vary across states. Required coverages tend to focus on liability and employee-centered policies, including:

Unemployment insurance: If you have employees, you may be required to pay unemployment insurance taxes to the state, which will be used to cover lost wages for former employees under certain conditions.

Workers' compensation insurance: This policy protects employees and the business in the event of workplace injury or illness. This business insurance is required in most states.

Professional liability insurance: Some states require specified professionals, such as lawyers and doctors, to carry insurance against professional liability.

Disability insurance: Several states require businesses to have partial wage replacement insurance coverage for eligible employees who experience non-work related injury or illness.

In order for your business insurance to cover flood damage, your company must carry a separate flood insurance policy or endorsement. A typical commercial property insurance policy covers specific water damage situations but excludes flooding.

Business insurance can help cover lawsuits, as long as you have the appropriate business liability insurance for the situation and enough coverage to pay your legal costs.

General, professional, directors and officers, product, and property are just a few liability coverage options that your business may need. A local independent agent can help you identify liability risks in your business and obtain the appropriate coverage for them.

To ensure that enough liability coverage is in place for extreme circumstances like a lawsuit that exceeds $1 million in damages, many businesses buy a commercial umbrella liability policy.

A business owners policy, or BOP, is insurance coverage designed specifically for small or mid-sized businesses. A BOP combines several types of insurance coverage in a packaged format, and it can be customized to suit a particular business. Generally, this type of policy includes both property and liability protection, which may cover events like property claims, equipment breakdown, loss of income, libel, and more.

Errors and omissions insurance, or E&O, is a form of professional liability insurance. It covers a business when services didn't end up as promised, or if those services lead to personal injury, damages or losses. Engineers, stockbrokers, accountants, insurance agents, and lawyers may be covered by E&O.

Malpractice insurance is also a form of professional liability insurance and covers physicians, dentists, pharmacists, and others.

Forming an LLC may keep your personal and professional liabilities separate, but it does not absolve your business of all liability or loss. Appropriate business insurance coverage can help protect your business from financial damage due to employee accidents, natural disasters, or legal liability lawsuits.

Because businesses have differing needs and risks, not all businesses require the same insurance coverage. However, there are essential coverage options that virtually all businesses should have, including:

General liability insurance: This insurance covers customer and pedestrian accidents and injuries that occur on your business’s premises, plus negligence claims.

Product liability insurance: This coverage protects your business from legal liability regarding defective products and any lawsuits, damages, injuries, or losses that stem from them.

Professional liability insurance: This policy protects professionals from liability if their services lead to client injuries or losses. Malpractice and E&O policies fall under the professional liability insurance category.

Commercial property insurance: This business insurance covers eligible damage to your business property, such as from a fire or a severe storm.

Business interruption insurance: Also known as business income coverage, this policy can help cover operational expenses if you cannot conduct business due to restorations from significant damage.

Because insurance for businesses needs to be tailored to each business’s unique needs and risks, it is critical to work with an agent to help make sure that you have adequate, appropriate coverage to minimize the impact on your business if an adverse event occurs.

Your Independent Insurance Agent Has Your Business Insurance Answers

Business insurance isn’t a one-size-fits-all product, but having the proper coverage can save your business from the unexpected. At Trusted Choice, our independent insurance agents will take the time to get to know your business’s risks so that we can find the right policy for you and your budget.

Best Business Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.