Your quote is based on several common factors to give you a clear picture of the cost you can expect for car insurance, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

Accidents happen, and auto insurance is designed to protect you and your family when you’re on the road. That’s why having the right vehicle insurance is so important. Even more important is understanding all the ins and outs of your policy to make sure you have the coverage you need at the best price. There are lots of options and getting a personalized quote is the best way to start.

In this article, we’ll look at how car insurance works, why you should have it, different coverage options, and how comparing quotes can help you save money.

What Is Car Insurance?

To put it simply, your car insurance is meant to help repair, replace, or compensate anyone or anything involved in a car accident. Damage. Injuries. Legal fees. Those numbers add up fast in a car accident, and insurance is designed to help keep you afloat and get back to life as easily as possible.

CAR INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

Why Do I Need Car Insurance?

First of all, you need car insurance because it's required in nearly every state before you can hit the road. The two states that don’t require auto insurance, Virginia and New Hampshire,have laws that essentiallymake it a must-have, though technically it’s not mandatory.

For example, Virginia requires you to pay $500 a year to legally go without car insurance, while New Hampshire requires proof that you have the financial assets to pay for any damage you would cause, equivalent to other state’s minimum liability coverage.

Second, it's way too costly not to have car insurance. Serious accidents, injuries, and deaths happen every day. Without vehicle insurance, you could be responsible for hundreds of thousands of dollars of injury expenses.

And third, car insurance also helps protect your financial investment in your vehicle. Financed or not, if your vehicle is totaled, you're out the entire investment. With car insurance, you'll get most—if not all—of that money back to replace your vehicle and get back on the road again.

What Does Car Insurance Cover?

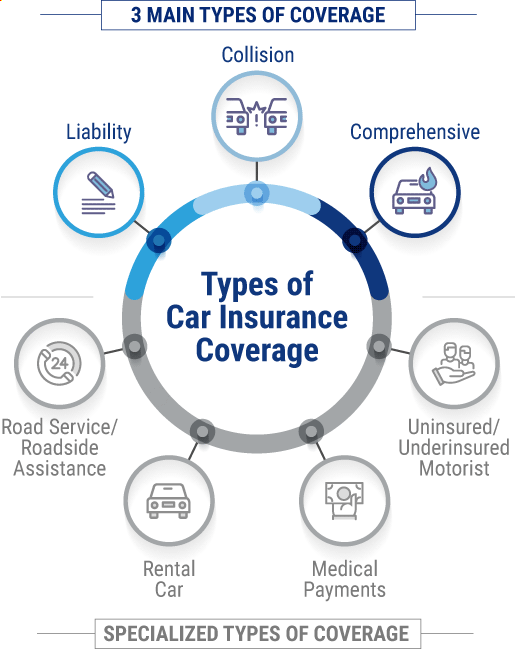

Your independent agent can help give you a clear, personalized picture of the coverage you need specifically for your car based on your unique situation. However, your auto insurance policy will generally come with three main types of coverages.

The most common car insurance coverage

Liability:This covers you if you’re at fault in a car accident. Liability is typically broken down into three key limits: bodily injury per person, bodily injury per accident, and property damage. The liability limits that you choose—say $100,000/$300,000/$50,000 respectively—are basically the maximum the insurer will pay.

Collision: This covers your own vehicle if it’s damaged in an accident. If the accident is ruled the other person’s fault, theirinsurance would pay for your damage. But if you cause the accident, or if you live in a no-fault car insurance state, your collision coverage will pay for the damage to your own vehicle.

Comprehensive: Also known as "other than collision," this covers your own vehicle for almost any other type of damage it could receive, like: theft, fire, hail damage, falling objects, windshield damage, and nearly anything that’s not wear and tear.

Additional car insurance coverage options

Uninsured/underinsured motorist(UM/UIM):Required in some states, this is meant to cover your own injuries and property damage if the at-fault person either has no insurance, or not enough to fully cover your injury expenses.

Medical payments: This is paid out to you and anyone in your vehicle if you suffer injuries in an accident. This is considered no-fault insurance, so it doesn’t matter who caused the accident or how—if you got hurt in your car, you’re eligible.

Gap coverage: Because cars depreciate so quickly (especially immediately after purchase) and insurers only pay current market value, gap coverage can help pay the difference between the purchase price and your remaining loan balance.

Convenience assistances

Rental car costs: If your car requires repairs after an accident, this coverage will pay for you to temporarily rent a car, up to a certain limit.

Roadside assistance:If you become stranded on the road, your insurance company will help provide assistance for free.

Towing expense: Different from roadside assistance, this will only reimburse you for towing expenses after the fact, not provide the service.

Situations Car Insurance Typically Does NOT Cover

It’s a good idea to familiarize yourself with your car insurance as much as possible. After all, the more you know about your coverage, the easier it is to avoid the hassle of filing sure-to-be-denied claims.

Car insurance does NOT cover the following:

Certain natural disasters (this includes floods, earthquakes, and mudslides)

Wear and tear damage (generally resulting from poor upkeep)

Damage as a result of hitting an animal in the road (in many cases)

Commercial use of vehicles (for instance, transporting goods for a business, or driving for a service such as Uber or Lyft, which require ridesharing insurance coverage)

Some vehicle modifications and add-ons

Who Is Included on My Car Insurance Policy?

When requesting car insurance, you’ll want to include any vehicle that is titled and could be driven. Car insurance primarily follows the car and not the driver. So if you're pulled over, the police officer is generally looking to see if the vehicle is insured, not if the driver is on the policy.

You can let anybody drive your vehicle and they will be covered under your policy. But insurance companies still want you to list anyone who has regular access to your vehicle as a driver.

WARNING: If you knowingly omit a driver, like your teenage driver who just got their license, you could risk having your claim denied by the insurance company.

How Much Does Car Insurance Cost?

The average cost of car insurance in the US is around $1,300 a year, or about $110 a month. Some states like Michigan and California are known to have higher car insurance rates, whereas South Dakota and Missouri have much lower rates. Your local independent agent will be able to help you understand rates in your area best, but there are a number of factors that go into the process of identifying your rates. You can also use our handy car insurance calculator tool to quickly get a jumping off point for the cost of your car insurance.

Biggest car insurance rate factors

Age: Drivers under the age of 25 typically pay higher rates, mainly because that age group gets into the largest number of accidents.

Location: City drivers pay more than rural drivers due to the increased likelihood of having a claim (traffic jams, thefts, stop-and-go driving).

Gender: Female drivers have lower rates than male drivers due to statistically better driving records.

Driving history: If you’re a safe driver, you’ll have fairly low rates for your vehicle type and location.

Type of vehicle: The more expensive the vehicle, the more it will cost to insure because the insurance company will have to pay more money to replace it.

Current insurance: If you don’t have prior insurance or have a long lapse in coverage, your options will be more limited and you’re likely to pay higher rates.

Credit score: Most states use your credit score as a rating factor, with better credit scores leading to lower rates.

The Best Ways to Save on Your Car Insurance Quote

Car insurance discounts are pretty common, with a number of ways to help you save through certain key behaviors. Each company offers slightly different discount options, but a few of the more common options include the following:

Multi-policy: You can typically knock off 10% to 20% when you bundle your car insurance with a homeowners or renters policy.

Multi-vehicle: If you have multiple vehicles on your policy, you’re likely to receive this discount, making each household vehicle slightly less expensive to insure than separately.

Vehicle safety features: Most new vehicles have advanced safety features, like passive or active restraints and blind spot monitoring. The better the safety features, the lower the risk and rates.

Safe driving record: A safe driving record over the last three to five years is a big indicator that you’re probably very cautious, insurers like that.

Good student discount: Younger drivers can have a dramatic impact on your rates. To help offset this, your child could receive a good student discount if they earned at least a B average last semester.

Defensive driving course: If you don't qualify for a safe driving discount, you can enroll in and complete an approved online defensive driving course and receive a discount.

Telematics: Offered by some insurers, this tracks your driving over a period of time and gives you a discount based on your habits and performance.

There are usually many more discounts available, such as paying for your policy in full, enrolling in automatic payments, quoting well ahead of time, going paperless, etc. Be sure to talk with an independent insurance agent to find out which discounts you qualify for.

How To Compare Car Insurance Quotes

When shopping for car insurance, it’s a good idea to work with an independent insurance agent to compare quotes. Most agencies offer free quotes online.

Here’s what you’ll want to look for when you compare quotes:

Coverage: Be sure to select the same amount of coverage for each quote so you’re comparing apples to apples.

Primary liability – this includes bodily injury and property damage coverage

Medical payment coverage

Uninsured motorist coverage

Collision

Comprehensive

Policy limits: This is the minimum and maximum amount the insurer will pay out for a claim.

Deductible amount: Think about how much it will cost to repair your vehicle and how much you’d be able to pay. In general, increasing your deductible lowers your premiums.

Other coverage: You might also ask about windshield replacement and rental car reimbursement.

Discounts: Ask about any discounts you may qualify for.

What Information Do You Need To Get a Car Insurance Quote?

When requesting a free car insurance quote, you’ll want to have the following information handy:

Your name and phone number

Driver’s license numbers for all drivers

The make, model and year of the car or cars to be insured

Vehicle Identification Number (VIN) for each

Safety features, such as anti-lock brakes or passive restraint systems

Anti-theft devices, such as GPS trackers

Roughly how many miles a year the vehicle will be driven

Your ZIP code and where you live

Car Insurance FAQs Answered

Car insurance isn’t always required by law, but nearly every state requires some minimum protection before you hit the road, which is typically liability insurance. That coverage is designed to protect anyone or anything from damage or injuries inflicted in an accident. Some states, however, even require additional coverage, including collision and comprehensive protection.

No matter which state you call home, though, it's important to have some sort of coverage to help cover damage and injuries and get you back to normal as fast as possible after an accident.

Simply put, because every time you get into a vehicle you take a risk. You may be an incredible driver, but you're not the only one on the road. Auto insurance helps provide a safety net when drivers make mistakes.

If you're at fault, you're typically liable for damage to the other person’s vehicle as well as the medical and legal costs of injured victims PLUS the repairs to your own vehicle.

If you're not at fault, and the other driver doesn't have adequate insurance, you'll have to pay for all the damage to your own car PLUS any medical bills if you're badly injured.

It's hard to offer an exact figure without knowing all the details of your vehicle and driving history, but car insurance premiums typically fall between $1,200 and $1,650 annually. Keep in mind, if you drive a high-performance hot rod or have an accident or two under your belt, you can expect that number to increase sharply. The good news is, if you've got a good driving record, you're getting good grades, or you're a part of some affinity group, you could get a nice discount to help lower your rates.

With access to multiple insurance companies, independent insurance agents are unlike any other type of agent out there. They’ll help find you the best coverage options and most competitive prices, all for free.

As you can imagine, the higher the deductible, the lower your premiums. But it’s important to think of your budget both now and later. In terms of now, you want to make sure your premiums fit comfortably into your current planned budget. And as for later, think of what you would be able to pay if the unexpected happened and you had to pay all that amount before your deductible. Is $500 right for you? $1,000? Your agent can help you find the best option for your situation.

If your car is stolen, there are a few things that need to happen for you to be compensated for your loss and get you back on the road. First, you'll need to file a police report and wait while there is an attempt to recover the stolen vehicle. If your car isn't recovered—and you have comprehensive coverage—you can file a claim with your insurance company. After a bit of paperwork, your insurance will compensate you for the value of the vehicle up to the limit of your comprehensive coverage.

When you rent a car, your rental agent will probably try to sell you insurance at an extra cost. Do you need it? In most instances, if you have car insurance that includes liability coverage it will apply to your rental car. However, before you rent a car, it’s a good idea to review your insurance policy to see exactly what coverage you have.

The credit card you use to rent a car may also provide a certain amount of rental car insurance. This is usually secondary insurance. If you get into an accident or your rental car is stolen, the company will bill your car insurance first, and your deductible will apply to the claim. Again. It’s a good idea to call the credit card company and find out what coverage they offer.

High-risk insurance is determined by your driving record, with recent driver history the most important factor. A driver is considered high-risk if they have multiple violations such as speeding tickets or if they’ve been convicted of a DUI/DWI. Other factors include poor driving records, younger or inexperienced drivers, lapses in coverage, at-fault accidents, and vehicles that are considered at higher risk of getting into accidents.

Your Independent Insurance Agent Has Your Answers to Car Insurance Questions

Whatever you need, your agent has your back. With a brief intro into the terms, discounts, and process of your car insurance, you now know the questions to ask. Your agent will ask you about your car, its use, and your goals to help you find the perfect blend of coverage at the right cost.

Best Auto Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.