Good employees are the backbone of your business. When an employee gets injured or becomes ill due to a work incident, workers’ compensation insurance (also known as workers' comp insurance) can help cover a portion of their expenses and get your employee back to good health sooner. A workers’ comp insurance policy can also provide financial protection for you and your business in the event of a legal dispute.

Before getting a workers’ comp insurance quote, it may be helpful to better understand how a policy can serve you. Here, you’ll learn about what a workers’ comp insurance policy is, who should have one, and how to save money on one.

What Is Workers’ Compensation Insurance?

Workers’ comp is a very important type of business insurance that not only covers employees’ workplace injuries, but also prevents them from suing their employers after an accident or illness. A workers’ comp insurance policy can protect your business by reducing liability, providing financial support for legal disputes, and minimizing the total financial loss to your business if an employee is injured on the job or gets sick as a result of their duties. Workers' compensation is required by law in most states, and those requirements can vary from state to state.

Workers' comp is a fairly comprehensive form of insurance protection. In addition to paying an injured employee’s medical bills, it can also pay rehabilitation costs, lost wages, disability benefits, funeral expenses, and even death benefits. However, it will only pay for those extra expenses if they’re directly caused by the workplace injury.

Workers’ comp insurance policies are almost always considered a no-fault insurance. This means it will pay the benefit regardless of who is at fault for the accident—as long as it wasn’t intentional. In most cases, this no-fault structure means an employee who accepts workers’ comp benefits cannot file a liability lawsuit against the business.

What Does Workers’ Compensation Cover?

Workers' compensation covers nearly all workplace injuries, as long as they're declared accidental. The full definition is fairly broad, however, with generic wording that defines what’s covered as “injuries sustained during the course and scope of employment.” For an illness or injury to qualify as work-related, it must occur during the employee’s regular job activity.

There could be some gray areas in what that means exactly. If you slip and fall in the parking lot on your way into work, that could be considered a workers' comp claim, though some states have stricter guidelines than others.

Why Do I Need Workers’ Compensation?

Workers' comp insurance is important for business owners to have for two very important reasons:

Financial protection: Workers’ comp can help cover the cost of injured employees’ medical bills and lost wages. Without a workers’ comp policy, your business may be responsible for paying those expenses. Even one serious injury could cost hundreds of thousands of dollars.

Legal protection: In most cases, employees who accept workers’ comp benefits forfeit their right to sue you for a workplace injury. With no workers’ comp policy in place, your business may be at risk for expensive liability lawsuits.

As for employers, workers' compensation insurance can help them provide financial help to injured employees and enjoy a fixed cost, and it also offers protection from lawsuits due to workplace injuries. Beyond protection for your business, workers’ compensation insurance also benefits your employees, giving them peace of mind that lets them stay focused on their job.

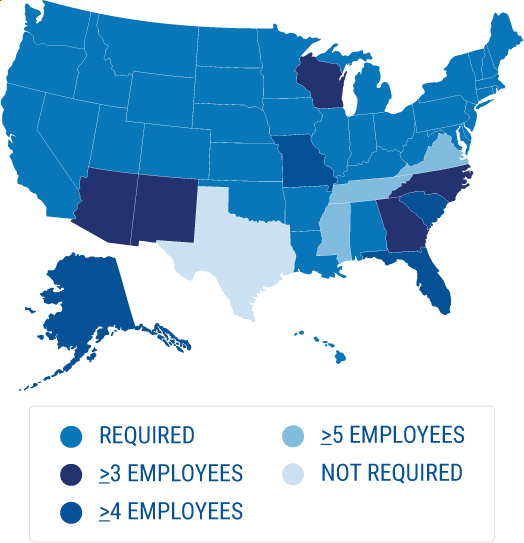

Is Workers’ Compensation Insurance Required?

Workers' comp, among a few other types of insurance, is regulated at the state level. Each state has its own set of workers' comp laws that regulate and govern it, with certain regulations depending on the type and size of the business.

If you're a sole proprietor or partnership, some states won’t require you to purchase workers' comp. Other states won’t require you to provide workers’ comp insurance until you have five employees. Most states require workers’ comp insurance regardless of the number of employees.

Independent contractors aren’t typically considered employees, but they may pose risks for your business. If they don’t have their own coverage and are injured at work, your business may be liable.

WORKERS' COMPENSATION INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

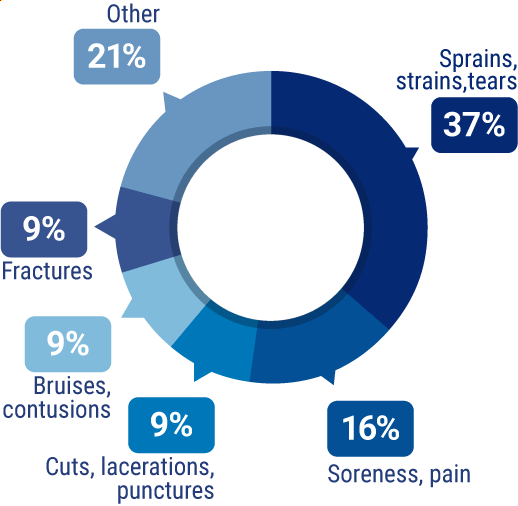

The Most Common Workers' Compensation Claims Include:

Workers' Compensation Insurance Benefits

If there is a workers' comp claim, the insurer will pay all medical costs related to the injury and include rehabilitation expenses and compensation for lost wages while the employee is unable to work. As you can imagine, in the case of a serious long-term injury, lost wages can be paid out all the way to retirement.

The exact amount that’s paid out in lost wages depends on whether the disability is total or partial, as well as permanent or temporary.

If the workplace injury leads to death, workers’ comp insurance can pay death benefits, such as funeral and burial expenses, and financial support for a person of the employee’s choosing, similar to an employer-based life insurance policy.

Top Workers' Compensation Considerations You Need to Know

It’s important to note, however, that employees can still sue employers for other types of workplace events, including harassment, bullying, discrimination, etc.

If a business chooses not to carry workers' comp, it could face a number of consequences, such as the following:

Criminal charges: If a business is required to carry workers' comp and doesn’t, it could be shut down, heavily fined, and possibly faced with jail time for breaking the law.

Legal costs: Without workers' comp coverage, businesses would face the full legal costs of any lawsuits brought against them.

Financial ruin: Without workers' comp coverage, businesses would face the full cost of any workplace injuries, lost wages, and lawsuits, which could easily put a company out of business.

Workers’ Compensation Laws by State

Each state has its own laws and regulations for workers' compensation insurance, including the following:

Size and type of businesses that require it.

What type of injuries are covered.

How long benefits are to be paid.

Because of these differences, a multi-state business will probably need to buy a separate workers' compensation policy for each state it operates in. Alternatively, the business owner could purchase a workers' comp policy that applies to all states, though these policies aren’t available in every industry and may be more expensive.

How Much Does Workers’ Compensation Cost?

Workers' comp costs vary widely, with three main factors affecting your premium:

The state your business operates in

The size of your business

The industry your business is in

For example, a large roofing contracting company will likely pay more for a workers’ comp policy than a large accounting firm due to the increased risk of the work. By contrast, premiums for a solo hair stylist could be a few hundred dollars a year, while a large manufacturer could pay hundreds of thousands of dollars each year.

Another factor that can affect your premium is your workers' comp claims history, expressed as a number, also known as an experience modifier, or just a 'mod,' for short. A business’s experience modifier is a formula that illustrates whether that business has had greater or fewer workers’ comp claims than others in the same industry. An experience modifier above 1.00 means your business has filed more claims than average, which may result in higher rates.

How Can You Get Lower Workers’ Comp Insurance Rates?

There are three key things you can do to lower your workers' comp rates, though it typically takes at least one year, if not three to five years, to earn a better claims history with a lower rate.

Ensure your workplace is a safe environment: Lower risks mean lower premiums, so use signs if there's a wet floor, make sure there are proper railings in place on any steps, and don’t leave any dangerous tools or materials in areas that could cause injuries.

Raise your workers' comp deductible: You could raise your workers' comp deductible to a higher number, such as $5,000 or so. While this would mean you would have to pay for injuries under your deductible amount, it would also help reduce the number of claims you have.

Lower your experience modifier: Having fewer claims with low dollar amounts will help your claims history. Having a better than average workers' comp modifier can give you better rates, but insurers will want to see more than one year of your claims history.

Workers' Compensation Insurance FAQs

Requirements for workers’ compensation insurance vary depending on the state. If your business operates only in one state, you will only need to be familiar with the rules, regulations, and requirements for the sole state in which you operate. However, if you operate in more than one state, you will need to navigate the rules and requirements for every state where your business maintains a presence. Your state’s regulations will dictate whether workers' comp insurance is offered by a private insurance company, a state-run agency, or the state itself.

Although requirements vary from state to state, most states do not require sole proprietors and partners to carry workers' comp insurance until they have employees who are not owners.

Workers' compensation insurance helps protect you and your employees if a job-related incident leaves them injured or ill. One of the most important coverages a business can have, workers' comp helps cover employees' medical bills after an accident, replaces a portion of lost wages, and even helps protect a business owner from being sued or paying expenses out of pocket.

In most cases, workers' comp insurance will pay 66% of lost wages while the employee is unable to work due to the covered event. The employee’s medical bills can also be covered. Every state has different laws when it comes to workers' comp, including when it's required, what’s covered, and how it's paid out. An independent agent can help you understand how it applies to your business more clearly.

Any employee who is hurt on the job or as a result of doing work for your business can file a workers' comp claim against the policy. An insurance adjuster will then be assigned to check the validity of the event and report back to the insurance company for a final decision.

As long as the employer is properly covered with a workers' comp insurance policy, the employee can file a claim against it. Once that has been done, an adjuster will be assigned to investigate the event and determine if it’s covered by the policy. A final decision will be made by the insurance company and, if legitimate, medical expenses will be paid for and reimbursed according to the terms of the policy.

Each state has its own laws that regulate and govern workers' comp insurance. While it may not be required for all businesses, it is likely to be required for most. The larger your business, the more likely it is that workers’ comp is required. Be sure you know the workers’ comp laws for each state your business operates in.

As you can probably guess, workers' comp isn't just a one-cost-for-all type of coverage. [Worker's Comp Costs] vary quite a bit, and several factors can influence the cost of your premium, including where your business operates, its size, and its industry. A large business in a risky industry, such as manufacturing, may pay significantly more for workers’ comp insurance than a small accounting firm.

Possibly. With workers' comp insurance, any type of work-related illness or injury may entitle an employee to receive benefits. This includes emotional and mental stress injuries that a worker suffers as a result of their job.

Embrace safety practices to reduce your business’s risk level. Since workers' comp offers protection against injuries, the best way to lower your risk is to be as safe as possible. A company culture of safety with common safety meetings, seminars, and proper precaution installations will show the insurance company that you mean business. They will typically give you a more favorable rate because you are minimizing their risk by being proactive and reducing the likelihood that you’ll file numerous high-dollar claims.

Independent contractors are typically not considered employees. However, if they get injured on the job and don’t have their own insurance, you as their client could be responsible for paying their medical bills or lost wages.

With access to multiple insurance companies, independent insurance agents are unlike contracted agents. They can help find you the best coverage options and most competitive prices by comparing policy options from different carriers. Find a local independent insurance agent.

Every business comes with its own share of risk. Whether you're running a large fireworks warehouse or a small bubble wrap shop, accidents can happen in all environments and businesses. As a business owner, having the right workers' comp insurance policy in place can help protect you, your business, and the employees who help you keep your operation running.

Your Independent Insurance Agent Has Your Answers for All Questions about Workers Compensation Insurance

Whatever you need, your independent agent has your back. They can help you understand the terms, discounts, and processes of workers' comp insurance. Your agent will ask about your business, its employees, and your goals to help you find the best workers' compensation option.

Best Workers' Compensation Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.

June of Medina, NY

June of Medina, NY