Pit Bull Prejudice: Why You Need Pet Liability Insurance

Pippa Elliott is a veterinarian with 27 years of experience, a freelance writer, and an all-around animal nut. The proud owner of five cats, two guinea pigs, and a bearded dragon, she is never happier than while writing with a cat on her lap.

Is Your Dog the Subject of Prejudice?

Do people cross the road to avoid your canine companion? Do insurance agents hem and haw when it comes to bite liability coverage? If the answer is "Yes," then chances are you own a bully breed dog. The trouble is that this (unjustified) prejudice runs more than fur deep and could cost you money.

Many cities and states have a legal requirement for dog owners to have liability insurance for their pet. Why does this matter? If your dog injures someone (accidentally or otherwise), you are liable for covering that person's medical, surgical, and legal bills, plus any loss of earnings. With over 4.7 million dog bites occurring annually in the US, it's not hard to understand why state laws require dog owners to make financial provisions to cover those costs.

Once upon a time you could be reasonably confident your homeowners insurance policy covered the liability if your dog injured someone, but times have changed. Many carriers now make a point of excluding certain breeds, typically bully breeds, which could leave you in the doghouse and financially liable if there is an unfortunate incident.

Survey Says...Most Dog Owners May Not Have Adequate Coverage

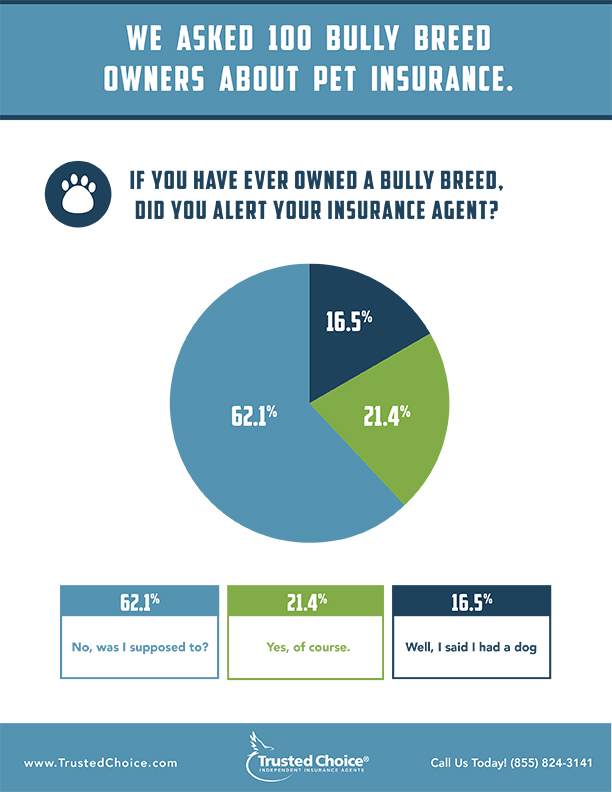

A survey by TrustedChoice.com found that nearly two-thirds of dog owners were unaware that it is usually necessary to tell your insurance company if you own a bully breed. Only one in five of our respondents had acted correctly and done this, which means that four-fifths of respondents may have invalid insurance policies.

Your bully may be the softest creature on the planet, he allows kittens to play on his back and licks away children's tears, but in the eyes of the law (because of breed prejudice) none of that matters. If your dog knocks over a visitor in the rush to give the visitor a kiss and that person sustains an injury and sues you, the first question your insurance company will ask is "What breed is the dog?" If you haven't declared his true identity, the company may be within their rights not to honor the claim.

But even when you do the right thing and tell an insurer at the outset that your dog is a bully breed, things may not go smoothly. Some insurers may refuse to take on breeds with a reputation for aggression or else may hike up their premiums.

So should you play truth or dare with dog bite liability coverage? No.

Withholding vital information will end with your tail between your legs. While you may believe you are covered, in the event of a claim your policy may become invalid and you may have no financial protection.

The Dirty Dozen: Which Breeds are Bully Breeds?

Before we go any further, it needs to be said that not just bully breeds are marked out for prejudice. Many states require liability insurance for dogs described as:"Dangerous, aggressive, vicious, or potentially dangerous."

In some states dogs from the following breeds automatically fall into this category: Akitas, Alaskan Malamutes, Chows, Doberman Pinschers, German Shepherds, Great Danes, Pit Bulls, Presa Canarios, Rottweilers, Siberian Huskies, Staffordshire Bull Terriers, and wolf hybrids.

So if you own such a dog, how do you get covered?

Honesty is the Best Policy

The first thing is to be upfront when investigating potential policies. Hiding the facts only backfires in the end. Not only will you not be covered in the event of a claim, but you may be blacklisted when taking out future policies.

Many insurance agencies share data about previous claims, using a system called CLUE – a similar idea to a credit rating, but linked to insurance. If a company perceives that you tried to deceive them (innocent as the explanation may be), they may flag this deception on CLUE for other companies to see, who might then refuse to do business with you, making it difficult to get homeowners insurance or other policies.

Two options to consider for bite liability are coverage on your homeowners policy that includes your dog (if you can get it), or taking out a specific liability policy for accident or injury caused by your canine companion. Bear in mind that coverage for dogs known to be aggressive is mandatory by law in the following states: Delaware, Georgia, Michigan, Minnesota, New Jersey, New York, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina, Texas, Virginia, and Washington.

Finding Coverage

Phone around and start by saying you have a bully breed – it might be a short conversation! Some carriers just don't want to take on the perceived risk and either refuse or make the premiums unreasonably high. But don't take it personally. Remember, rejection of your dog is not a rejection of a member of your family, but a business decision on their part.

However, there are companies out there prepared to spread a little bully breed love. These are the enlightened carriers who recognize facts. And the facts are that it is not breed that makes a dog aggressive, but factors such as being poorly socialized, unneutered, or in a pack situation. Statistics show that fatal attacks are almost unheard of (regardless of breed) in neutered dogs belonging to responsible owners that are raised in a family home – some insurers know this and ask the right questions.

So how do you find these insurance companies? The answer is to call your Trusted Choice® independent agent, who is able to write policies for multiple carriers and will be able to compare policies to find you the right coverage for you and your pet. The agent can guide you towards a policy that meets your needs, which means you can sleep easy knowing your canine companion has liability coverage.