Your quote is based on several common factors to give you a clear picture of the cost you can expect for homeowners insurance, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

For many people, owning a home is part of the American dream. As exciting as owning a home can be, dealing with risks like fire, theft, and other unexpected disasters can leave a lot to worry about. That’s where homeowners insurance comes in.

To get the most out of your insurance, you need to understand all the ins and outs, as well as what is and isn’t covered. There are lots of options, and you want to be sure you have the coverage you need at a price that fits your budget. Fortunately, an independent insurance agent can help find the right home insurance policy for you. But first, here's a deep dive into home insurance.

In this article, we’ll look at how homeowners insurance works, why you should have it, different coverage options, and how comparing quotes can help you save money.

What Is Homeowners Insurance?

Regardless of whether you live in an oceanfront dream house or a little cottage in the country, homeowners insurance is essentially an agreement between the homeowner and an insurance company in which the insurer agrees to cover financial losses relating to damages and liabilities. Thing is, only the specific events or circumstances – sometimes known as “perils” – stated in the policy will be covered by your insurance company. Homeowners insurance helps protect homeowners from losing their homes following a disaster.

Why Do I Need Homeowners Insurance?

You need homeowners insurance mainly to protect your home and your possessions. No matter how sturdy the walls and beams surrounding you are, they’re still not much of a match against a strong storm or raging fire, or any number of other perils. Without proper coverage, a particularly costly disaster could cause a homeowner to go bankrupt if they don’t have the financial resources necessary to recover from the damage/destruction.

Aside from just losing the structure of your home itself to a disaster, you could also stand to lose your personal belongings. One of the greatest joys of being a homeowner is to fill the place with items you love. Those possessions deserve protection too. Homeowners insurance includes coverage for your home’s contents as well as the physical building.

Finally, homeowners need protection from costly liability issues that could arise within the home. If guests or workers get injured or have their property damaged while at your place, you could get slapped with an ugly lawsuit. Having adequate insurance on your house could seriously help with the financial ramifications in such a case.

HOMEOWNERS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

What Does Homeowners Insurance Cover?

Your home is more than just a collection of walls, ceilings, and floors. Homeowners insurance is designed to cover all the elements within your oasis. This includes your personal property, family, pets, and friends who come to visit. The more complex your home is, the more coverage you're likely to need, such as an umbrella policy or replacement cost home insurance.

Here are the four major coverage areas included in standard homeowners insurance policies:

Structural damage:This coverage is designed to safeguard what insurance companies refer to as the “dwelling” or the structure of the home itself. Damage to or destruction of the dwelling by covered perils falls under this category. Coverage often extends to detached structures such as sheds as well.

Personal property damage: This coverage helps protect your personal belongings like furniture, clothing, electronics, knickknacks, old toy collections, silverware, etc., from perils such as fire or theft. Items stored in the home as well as in external storage units are covered, though property stored off-premises may have a lower coverage limit.

Liability: This coverage can help provide for legal expenses such as attorney and court fees if you are sued for bodily injury or property damage to a third party. Settlements you’re ordered to pay if you lose the case are covered as well. Coverage extends to all members of the family living in the home, including pets. Many incidents that occur away from the home are also covered.

Additional living expenses: Also referred to as “loss of use,” this covers living expenses if your home gets badly damaged or destroyed and you’re forced to live elsewhere while awaiting repairs. Your insurance company provides reimbursement for things like hotel rooms, eating out, extra gas mileage, and more. Additional living expenses cover the difference in spending to maintain your normal lifestyle while living away from the home.

These four components essentially make up the core of homeowners insurance packages. An independent insurance agent can help you find the right amount of coverage in each category for your unique home.

Most Common Claims Covered by Homeowners Insurance

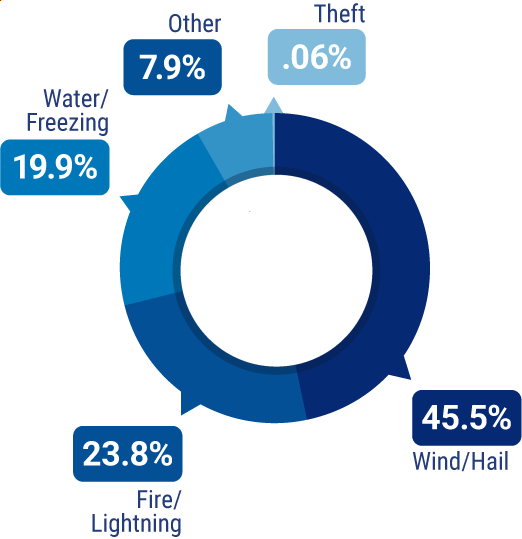

What’s the most common homeowners insurance claim for covered damage? According to the Insurance Information Institute’s 2021 statistics, property damage from wind and hail tops the list, accounting for 45.5% of all claims filed.

Claims for fire or lightning damage came in next at 23.8%, followed by water damage/freezing at 19.9%. At the bottom of the most prevalent types of claims were theft at .06% and a variety of other claims lumped together, accounting for 7.9%.

While homeowners can expect their policies to provide coverage, it’s a good idea to be aware of the kind of damage that insurance can protect against, like:

Wind/hail: Wind and hail can result in damage to the roof and siding, fallen trees, broken windows, broken siding, and other damage to homes.

Water/freezing: Water from inside the house can cause sudden and accidental damage. This includes burst pipes, freezing pipes, and leaking roofs. Other damage may result from ice dams, where water cannot drain properly through the gutters and seeps into the ceiling and walls.

Fire/lightning: In the event of a house fire, homeowners insurance will cover the structure and belongings. You can also file a claim if a lightning strike to your home causes a power surge or a fire.

Theft: This includes theft from your home as well as theft from your automobile.

Other: Miscellaneous property damage and claims related to a variety of incidents (including injuries sustained on your property) make up this category.

Take the time to review your home insurance policy at length so you're familiar with exactly what's covered by it and what's not.

Is Homeowners Insurance Required by Law?

Homeowners insurance is not required by law. But most mortgage lenders are likely to require you to have a policy before they agree to sign off on a loan. Regardless of whether it’s required or not, it’s always better to consider getting coverage because there are numerous risks that could damage or destroy your home or belongings, and, consequently, your bank account.

Additional Homeowners Insurance Coverage Options

Depending on your specific needs, you may want to consider additional coverage for your peace of mind, like:

Jewelry and valuables: Standard coverage for these items is generally limited to between $500 and $2,000. If you have expensive jewelry, things like engagement rings, wedding bands, or diamond bracelets, you can purchase special coverage to protect your valuables.

Water backup and sump pump overflow: During heavy rain, your sump pump may fail, causing a big mess. This coverage provides added protection for water damage that results from failed sump pumps or backed-up drains.

Identity theft recovery: If someone steals your identity and runs up your credit cards or tries to take out loans in your name, the results can be costly. While identity theft may not have a direct impact on your status as a homeowner, many insurance companies offer an identity theft coverage option that can be added to your policy. Identity theft recovery helps cover expenses like legal or administrative fees that you might need to pay to restore your identity.

An independent insurance agent can advise on any additional coverage you may need to add to your home insurance policy.

HOMEOWNERS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

When and Why Would I Need Extra Policies?

Once you’ve got your main homeowners insurance policy that matches your specific home in place, you still may be lacking coverage in a couple of areas. In such a case, you might need to supplement your policy with additional coverages in order to get a fuller blanket of protection for your home. Here are a few of the main supplemental policies that homeowners often need:

Business liability coverage:If you run a business out of your home, even part-time, homeowners insurance policies of all types typically won’t cover any liability-related mishaps. Liability issues such as bodily injury or property damage can be costly, so it’s best to have coverage in all areas.

Flood insurance:Flood coverage is always excluded under homeowners insurance policies. If you live in an area that's beside the water or otherwise prone to flooding, you’ll most likely want to purchase a separate flood insurance policy.

Earth movement insurance: Earthquakes are another natural disaster that are always excluded by homeowners insurance policies. If you live in an area prone to earthquakes, you’ll probably want to talk to your independent insurance agent about adding on an earth movement policy.

Special vehicles coverage: Homeowners policies of all kinds tend to limit liability coverage for certain types of vehicles, including ATVs, aircraft, boats, etc., and also have very specific exceptions for certain powered vehicles like riding lawnmowers.

Riders, floaters, or endorsements: Depending on the kind of personal property you want to be covered by your homeowners insurance, your policy may not come with a high enough built-in limit. If you’ve got expensive property like jewelry or electronics, your agent might suggest special riders, floaters, or endorsements to increase your coverage limits.

Your independent insurance agent can advise you on when you’d need to add supplemental coverages on top of your homeowners insurance policy. They’ll make sure you walk away with all the coverage you need.

Situations Homeowners Insurance Typically Doesn't Cover

It’s a good idea to become familiar with the situations not covered by your policy. The more you know about your coverage, the easier it is to avoid the hassle of filing claims that are likely to get denied.

Homeowners insurance does not cover the following

Certain natural disasters (such as floods, earthquakes, and mudslides)

Maintenance-related losses

Wear and tear damage (typically poor home upkeep)

Insect damage or infestations

Business-related liability

In addition, if you run a business out of your home, your home policy typically won’t cover any liability-related mishaps. It also limits liability coverage for certain types of vehicles, like aircraft, ATVs, and boats. The easiest way to make sure you have the coverage you need is to tell your independent insurance agent all about your home and any related business.

In order to protect your home against flood or earthquake damage, you’ll need a flood insurance or earth movement policy. Homeowners who live in areas prone to flooding may want to seriously consider getting a policy.

How Much Does Homeowners Insurance Cost?

Many factors influence the cost of a homeowners insurance policy, including the size and location of your home, the value of the structure, the contents inside, and any upgrades you’ve made. Homeowners located in areas prone to severe weather or other risks like crime will be required to pay more for their insurance policies than those who live in calmer, safer areas.

It's hard to offer an exact figure without knowing your unique situation and the specs of your individual home, but this year homeowners insurance premiums tend to average $1,211 annually. The fewer risks associated with your specific home, the closer you're likely to find yourself toward the lower end of the spectrum. An independent insurance agent can help find more exact quotes for you.

HOMEOWNERS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

What Are the Benefits of Homeowners Insurance?

You’ve worked hard to afford a home you love, so regardless of what kind of home you live in, it deserves to be protected. Having adequate insurance coverage can prevent a homeowner from going bankrupt and losing their home following a particularly costly disaster. Standard homeowners insurance packages provide coverage for many common threats to the home.

Standard homeowners insurance typically provides coverage for the following perils:

Theft

Vandalism

Explosions

Fire and smoke

Water damage

Aircraft or vehicle damage

Riots

Falling objects and trees

Certain natural disasters (e.g., windstorms, hail, lightning, and blizzards)

Your independent insurance agent can help you review your homeowners insurance policy to answer any remaining questions about your coverage. They’ll also be able to help you figure out whether you’ve got enough coverage, or if you should purchase more.

What Other Types of Homeowners Policies Are Available?

Since there’s not just one type of home, there’s also not just one type of homeowners insurance coverage available. While the core of many different types of homeowners policies often remains consistent as far as the coverages included, your insurance will be tweaked a little to meet its unique protection needs depending on your specific home and its correlating policy.

Here are a few of the most common types of homeowners insurance policies:

Townhouse insurance:Designed for owners of townhouses. Pretty self-explanatory. If the townhouse is also a condo, coverage will include protection for the owner’s share of the “common areas” within the community.

Mobile home insurance:Designed for owners of homes constructed in a factory and then taken to the property to be set up. These homes may be on wheels, but not necessarily. Coverage still looks very similar to standard homeowners insurance.

Modular home insurance:Designed for owners of homes that are constructed in factories and then shipped in sections to be assembled on the property. Again, coverage looks very similar to standard homeowners insurance.

Houseboat insurance:Designed for owners of watercraft, such as yachts, that also double as homes. Coverage includes elements of watercraft policies and mobile home policies.

Condo insurance:Designed for owners of condos. Coverage includes protection for the condo owner’s percentage share of the “common elements” within the main building as well as any structural elements or fixtures within the unit that the owner is responsible for.

Vacation home insurance:Designed for owners of cabins, lake houses, etc., that serve the specific purpose of being used for recreational activities and are not the primary residence.

Secondary home insurance:Designed for owners of more than one primary residence. Coverage for the second home will be practically identical to the first.

High-value home insurance:Designed for owners of very expensive homes like luxury estates. Coverage limits are much higher than in traditional homeowners insurance, and policies may include add-on coverages such as kidnap and ransom insurance for high-profile individuals.

Depending on the type of home you live in, your homeowners insurance policy will be tailored to match it. An independent insurance agent can help you get set up with the right policy for your needs.

The Best Ways to Save on Your Home Insurance Quote

To start, combining other policies and raising your deductible are two of the easiest ways to drive down your cost. When you work with an independent agent, they'll help you find the most discounts based on what you qualify for, including the following:

Safety discounts: These discounts can apply when your home features upgraded special safety features like burglar alarms, sprinklers, or a high-quality roof.

Bundling discounts: If you have multiple homes or any vehicles, bundle your coverage together with the same carrier for a discount.

Group discounts: Certain associations and professions, like service members, teachers, farmers, and dentists, get group discounts.

Loyalty discounts: Customers who stay with the same insurance company for a long time are rewarded with discounts.

Located near a fire hydrant/fire station: The closer you are to a fire hydrant, and also your local fire station, the faster fires can be put out, earning you a discount.

New home: New homes typically are built with stronger safety innovations, making claims less costly and helping to lower coverage costs.

High-quality roof: Hail and wind damage are among the top reasons homeowners file a claim. A sturdy roof can lower your premiums.

Few recreational hazards: A home without a pool or trampoline is at much less risk of a claim, earning you a discount on your coverage.

An independent insurance agent can help you find any home insurance discounts you qualify for to reduce the cost of your premiums.

How to Compare Home Insurance Quotes

Prices for similar home insurance coverage can vary dramatically, so work with an independent insurance agent to find the best price for the coverage you need. Most agencies offer free quotes online.

Here’s what you’ll want to look at when you compare quotes:

Dwelling protection: This would cover the replacement cost of your home. A quick way to figure out the replacement cost is to use the price you paid for the home or the current market price. Keep in mind that this may or may not adequately cover the cost of rebuilding. Investigate local construction costs to get a more accurate figure of what you’d actually pay to rebuild.

Contents protection: This covers your belongings. The amount your insurance will cover is typically 50% of your dwelling coverage, which may or may not be enough. To determine how much coverage you need, do a thorough inventory of your belongings. If you need more coverage, ask about higher limits for personal possessions.

Liability protection: Typical coverage is $100,000. You may opt for higher coverage of at least $300,000 or enough to cover your net worth.

Additional living expenses coverage: This coverage would typically help pay for expenses if your home is damaged and you have to find temporary lodging elsewhere. Covered expenses could include those for a hotel, food, clothing, pet boarding, and more. Coverage is typically 20% of your dwelling coverage.

Remember, flood and earthquake coverage are not included in standard homeowners policies. If you need coverage, be sure to ask about it when getting a quote.

HOMEOWNERS INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

What Do You Need to Start a Home Insurance Quote?

Be prepared when you start looking for a homeowners insurance quote by having some information on hand first. You’ll need information about your home, yourself, and how much insurance you want. Keep all of the following in mind:

Your date of birth

Your Social Security number. If you own the home with your spouse, their date of birth and Social Security number will be needed, too.

The address of the home you want to insure

The year the home was built

Any repairs or renovations

The age of the roof

The number of people who live in the home

If you run a business out of your home

The date coverage should start

Any existing homeowners insurance policy

Coverage needs, including your dwelling, contents, liability, and additional living expenses

An appropriate amount for your deductible, or how much you're willing to pay out of pocket before receiving any reimbursement

An independent insurance agent can also advise you on what you need to know before obtaining a home insurance quote.

Homeowners Insurance FAQs

Homeowners insurance isn’t required by law, but nearly every lender will require a policy in order to give you a loan. At a minimum, they’ll want your policy to cover the amount you owe on the loan. It’s just their way to protect their investment in you.

Simply put, you need homeowners insurance to protect your home, finances, and livelihood. You’ve worked hard to afford a home you love, and it deserves to be protected. Having the proper insurance coverage can prevent you from going bankrupt and losing the things you love after a costly disaster. Standard homeowners insurance packages provide the protection you need from a number of common threats to your home.

It's hard to offer an exact figure without knowing your unique situation and all the details of your home. Our research found that the current average cost of home insurance is $1,211 per year. Just remember, the fewer risks you have to worry about, the less insurance will cost. Use our homeowners insurance calculator to estimate your costs today.

With access to multiple insurance companies, independent insurance agents are unlike any other type of agent out there. They’ll help find you the best coverage options and most competitive prices, all for free.

It’s important to think of your budget both now and later. In terms of now, you want to make sure your premiums fit comfortably into your current planned budget. Also, think of what you would be able to pay for if the unexpected happened and you had to pay the amount before your deductible. Your agent can help you find the best option for your situation.

While homeowners insurance provides a lot of important coverage, sadly it can’t cover absolutely everything. Disasters like hurricanes, floods, and earthquakes typically aren’t covered by your home insurance and require additional coverage to help protect you. It’s a good idea to become familiar with what's not covered in your specific policy so you’re not expecting coverage when you don’t have it.

While they may sound similar, flood damage is not the same as water damage. Flood damage is caused by water from a natural disaster, storm, or heavy rain. On the other hand, water damage is typically caused by a plumbing issue, like a broken pipe, an overflowing washing machine, or a backed-up toilet.

Here are a couple of examples:

If a pipe bursts in your home and floods your living room, that would be considered water damage.

If an overflowing river causes your home to flood, that would be flood damage.

It can be a little confusing, so be sure to speak with your independent agent about coverage. If you’re in an area prone to flooding, consider purchasing flood insurance.

As the name implies, an umbrella policy offers extra protection from a variety of risks and provides coverage over and above your standard homeowner liability policy limits.

Why might you need an umbrella policy? Let’s say you have a party at your home, and someone falls, severely injuring themselves. If they successfully sue you for $1 million, but your liability coverage limit is $250,000, your umbrella policy would cover the other $750,000 in damages.

An umbrella policy also protects you against damage you cause to someone else’s property, and also against lawsuits involving slander or libel. Talk with your independent insurance agent to find coverage that best fits your needs.

Your Independent Insurance Agent Has Your Answers to Homeowners Insurance Questions

Independent insurance agents have access to multiple insurance companies, ultimately finding you the best home insurance coverage, accessibility, and competitive pricing while working for you. They can shop and compare tons of different policies and present you with only the best options.

Best Homeowners Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding home insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed homeowners insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for homeowners insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get homeowner's insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for homeowner's insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.