If an Employee Tips over a Forklift, but Was Never Authorized to Use It, Who's Responsible?

Christine Lacagnina has written thousands of insurance-based articles for TrustedChoice.com by authoring consumable, understandable content.

Jeff Green has held a variety of sales and management roles at life insurance companies, Wall street firms, and distribution organizations over his 40-year career. He was previously Finra 7,24,66 registered and held life insurance licenses in multiple states. He is a graduate of Stony Brook University.

Unfortunately, workplace injuries are common and can be costly for your business if you get sued by the hurt employee. But what happens if an employee gets injured due to their own negligence? Who’s responsible for this mess anyway?

Luckily an independent insurance agent can answer these important questions for you and also get you set up with the right business insurance policy. Here’s how they’d help you get protected against a worker injury that occurred from operating a forklift they weren’t supposed to be using.

Who’s Responsible if My Employee Tips over a Forklift They Weren’t Supposed to Be Using?

If an employee’s injury occurs due to their own negligence, they may be responsible for their own injuries. According to insurance expert, Jeffrey Green, an employee may not be eligible for workers’ comp benefits if they were violating company policy when they got injured on the job.

Workers’ comp laws vary by state. It’s important to be familiar with your own local laws around employee injuries from the very beginning.

Are Employees at Fault for Their Negligence in My State?

To determine if your employees can be held responsible for their workplace negligence in your area, you’ll need to review your state’s workers’ comp laws. Certain states have a “no-fault” system, which allows injured employees to receive monetary compensation regardless of who caused their injury. Your independent insurance agent can help you determine if you live in a no-fault state.

What Kind of Coverage Do I Need to Protect My Business?

To protect your business against lawsuits from injured employees, you’ll need to be equipped with a workers’ comp policy. Workers’ comp guards businesses against being sued by employees who get injured due to job-related activities, or while on the job.

In exchange for forfeiting the right to sue the business, the employee is entitled to monetary compensation for qualifying injuries. An independent insurance agent can help your business get set up with all the workers’ comp insurance it needs to protect itself and its team of workers.

What Does Workers’ Comp Cover?

Beyond protecting your business from strange incidents such as an employee injuring themselves on a forklift they weren’t supposed to be using, workers’ comp provides many important benefits.

Workers’ comp compensates for the following

- Medical costs: For employees who get injured on the job or due to job-related duties, workers’ comp provides reimbursement for treatments, medications, etc.

- Non job-related employee harm: Catastrophes like workplace violence, terrorist attacks, and natural disasters are also covered by workers’ comp.

- Employee wages: If an employee has to miss work while recovering due to a covered injury/illness, workers’ comp can pay to replace their lost salary.

- Employee benefits: A death or disability benefit can be paid out for employees who become disabled or get killed on the job under workers’ comp.

- Funeral costs: Workers’ comp can sometimes also provide reimbursement for funeral planning and related costs if the employee gets killed on the job or due to work activities.

An independent insurance agent can further explain all the important protections workers’ comp offers businesses of all kinds.

Save on Workers' Comp Insurance

Our independent agents shop around to find you the best coverage.

Where Can I Get Workers’ Comp Insurance?

Workers’ comp is sold by many insurance companies nationwide. To find the one that best matches your needs, work together with an independent insurance agent. Until then, here’s a look at some of the current top-performing workers’ comp companies in the US.

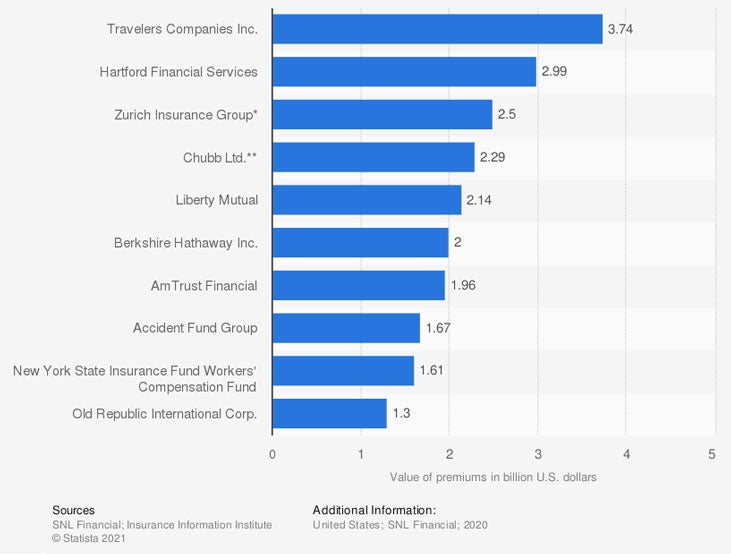

Leading writers of workers' compensation insurance in the United States, by direct premiums written (in billion US dollars)

The current leading workers’ comp insurer is Travelers Insurance, with $3.74 billion in direct premiums written. The second leading insurance company is Hartford Financial Services, with $2.99 billion in direct premiums written. Zurich Insurance Group takes the third spot, with $2.5 billion in direct premiums written.

Your independent insurance agent can help you find the right workers’ comp coverage for you, whether it’s from one of these companies or somewhere else.

Here’s How an Independent Insurance Agent Would Help

When it comes to protecting businesses against employee injuries caused by negligence and all other incidents, no one’s better equipped to help than an independent insurance agent. Independent insurance agents search through multiple carriers to find providers who specialize in workers’ comp insurance, deliver quotes from a number of different sources and help you walk through them all to find the best blend of coverage and cost.

https://www.statista.com/statistics/186480/workers-compensation-insurance-top-us-writers-by-direct-premiums/

https://www.belsky-weinberg-horowitz.com/does-workers-compensation-cover-employee-negligence/