Pharmacy Insurance

Pharmacies need protection against lawsuits after professional errors, property damage, and more.

Christine Lacagnina has written thousands of insurance-based articles for TrustedChoice.com by authoring consumable, understandable content.

Jeff Green has held a variety of sales and management roles at life insurance companies, Wall street firms, and distribution organizations over his 40-year career. He was previously Finra 7,24,66 registered and held life insurance licenses in multiple states. He is a graduate of Stony Brook University.

Running a pharmacy involves keeping all kinds of risks in mind on a daily basis. From filling customer orders to protecting inventory from spoilage, there's plenty of room for potential mistakes. That's why having the proper pharmacy insurance is crucial.

Fortunately, an independent insurance agent can help you find the best pharmacy insurance for your needs. Even better, they'll get you set up with all the coverage required, long before you need to ever file a claim. But first, here's a closer look at pharmacy insurance and why it's necessary.

Pharmacy and Drug Store Industry Stats

- There are about 44,900 pharmacies and drug stores in the U.S.

- More than 1,136,866 people are employed in this industry

- This industry generated about $550 billion in one recent year

- About 43.7% of the global pharmaceutical market is located in the U.S.

Save on Business Insurance

Our independent agents shop around to find you the best coverage.

The pharmaceutical industry is huge, both in terms of size and revenue. That's why it's helpful for each individual pharmacy to be equipped with the proper protection.

What Is Pharmacy Business Insurance?

Pharmacy business insurance is a special type of coverage designed to protect the owners and operators of pharmacies and prescription drug stores. Often, the basics of coverage are provided in a business owners policy (BOP), which then gets topped off with additional coverages specific to the business niche's needs. An independent insurance agent can help ensure that your pharmacy or drug store gets equipped with each type of coverage it requires to succeed.

What Could Go Wrong at a Pharmacy?

There are a number of things that can go wrong at a pharmacy, and some of these could be financially harmful to businesses that lack the proper coverage. Consider how your pharmacy or drugstore would handle the repercussions in these scenarios:

- A customer falls while on their way to the pharmacy counter and suffers a hip fracture that requires surgery. The customer then sues your business for their medical treatment and lost wages.

- An employee uses their own vehicle to make a prescription delivery to a customer. On the way, they cause a serious collision that injures a family, who then sues your business.

- A pharmacist accidentally mislabels a prescription bottle, and a customer who takes the medications ends up in a coma. The customer's family then sues your pharmacy.

Distributing medications comes with a myriad of risks. Just one mistake could cause major health problems to a third party, not to mention lawsuits against your business. For this reason, pharmacies and drugstores were among the first businesses to have industry-specific, custom-built insurance packages.

Who Sells Pharmacy Business Insurance?

Pharmacy business insurance is available from many different insurance companies, and the best way to find the right carrier for you is through working with an independent insurance agent. They know which insurance companies to recommend to meet your needs and can provide informed suggestions based on company reliability, rates, and more.

While many insurance companies could create a pharmacy business insurance policy for you, finding coverage could also depend on the area you live in. Here are a few of our top picks for pharmacy business coverage.

| Top Pharmacy Business Insurance Companies | Overall Company Rating |

| The Hartford |

|

| SME Insurance |

|

| Hiscox |

|

| Bethany Insurance Agency |

|

| Allstate |

|

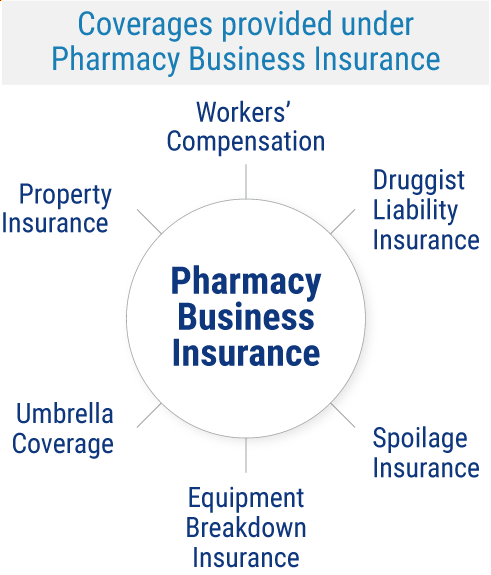

What Does Pharmacy Business Insurance Cover?

Pharmacies need coverage for not just their medications provided to the public, but also for routine business operations. Pharmacy insurance is customizable, so you’ll build your package based on the needs of your specific business.

Your policy will provide the basic protections included in standard business insurance and get topped off with additional, pharmacy-specific coverages. Here are some of these important coverage options for pharmacies.

- Workers’ compensation: Workers’ comp protects your employees if they get ill or injured on the job or die from a work-related incident. Coverage is mandatory for most businesses, depending on the state.

- Pharmacy property Insurance: Property damage coverage protects against damage to or destruction of your pharmacy’s physical building as well as the contents inside (e.g., furniture, carpeting, electronics, etc.) after a covered disaster like a fire, hailstorm, etc.

- Pharmacy liability insurance: Pharmacy liability insurance is a special form of professional liability coverage tailored to pharmacists. If a prescription is filled incorrectly, it can result in a costly lawsuit against your pharmacy.

- Umbrella coverage: Commercial umbrella insurance provides reimbursement for excess liability charges that reach beyond your built-in business insurance liability limits. Up to $100 million in this coverage may be added.

- Equipment breakdown insurance: Equipment breakdown coverage protects against damage to major appliances that may be affected by power outages, etc. Many medications require refrigeration, so this can be a crucial add-on to pharmacy insurance.

- Spoilage insurance: This provides compensation for medications that require refrigeration if an extended power outage renders them unusable.

You may want to list more expensive medications on a separate policy, such as an inland marine insurance policy. Costly products can be cheaper to insure this way. Your independent insurance agent will help you determine which coverages are the most important for you and your pharmacy business.

What Other Types of Pharmacy Business Insurance Coverage Do You Need?

In addition to the basic coverages, there are other protections that may be required or are at least worth considering for your pharmacy or drug store. You may need one or more types of pharmacy insurance from the following list:

- Business income insurance: This coverage provides your pharmacy with a continuation of income and employee wages in the event that a covered disaster forces you to close up shop while repairs are made.

- Flood insurance: Commercial insurance policies exclude coverage for losses sustained due to floods. You will need to add a commercial flood insurance policy to get this protection.

- Employment practices liability insurance: This insurance provides coverage in the event one of your employees sues your pharmacy for breach of contract, wrongful termination, discrimination, or any other illegal business practice.

- Employee dishonesty insurance: This insurance protects your pharmacy from financial losses if one of your employees steals from your business or engages in other illegal practices while on the job.

There are a number of different insurance options available to you, and some may be a good fit for your pharmacy. Be sure to discuss your day-to-day operations with an independent insurance agent who can suggest appropriate coverage.

Additional Coverages for Pharmacies

A lawsuit can be financially devastating for your pharmacy. Even if your store is found to be non-negligent, the cost of your legal defense can be overwhelming.

Fortunately, liability insurance provides your business with a financial safety net. Some coverage types you will want to discuss with your independent insurance agent include the following:

- Premises liability insurance: This protects your pharmacy if a third party suffers property damage or injury while in your place of business.

- Product liability insurance: If your pharmacy sells a faulty product that causes illness or injury to a third party, your business may be named as a defendant in a liability lawsuit.

- Auto liability insurance: If your pharmacy makes deliveries, you will need a commercial auto policy for company-owned vehicles, and hired or non-owned vehicle liability coverage for personally owned vehicles.

- Cyber liability insurance: This coverage is critical to protect your sensitive electronically stored data and information from hackers and data breaches.

An independent insurance agent will ensure your pharmacy business gets equipped with all the additional coverages necessary to maintain smooth and safe operations over time.

What Doesn't Pharmacy Insurance Cover?

Though pharmacy insurance comes with many important coverages, it also comes with a list of exclusions. These are just a few incidents most commonly not covered by pharmacy insurance policies:

- Robbery

- Pollution

- Dishonest acts by staff

- Routine maintenance

- Earthquake damage

- Nuclear reaction and war

- Temperature changes

- Missing inventory

- Flood damage

Your independent insurance agent can provide you with more information about finding coverages necessary for your specific pharmacy business if they're excluded from your main policy.

How Much Does Pharmacy Insurance Cost?

The cost of your pharmacy insurance package isn’t a standard number. A lot of factors go into determining the cost of your coverage. Here are just a few:

- The size of your pharmacy

- The amount of business you do annually

- The value of your inventory

- How many employees your pharmacy has

- The age of your pharmacy’s construction

- Your pharmacy’s specific location

Your independent insurance agent will help you find coverage that fits within your pharmacy’s budget. They’ll also be able to scout out any discounts you qualify for.

Frequently Asked Questions about Pharmacy Business Insurance

Sometimes called “drugstore” insurance, pharmacy business insurance is designed to cover all aspects of pharmacies or prescription drug stores, from professional errors and lawsuits to routine business operations and lost income.

Pharmacy insurance protects your business against lawsuits filed by third parties and also protects many other aspects of your business. Property damage, employee injuries, data breaches, and more can be covered by your pharmacy insurance, depending on which coverages you select, with the help of an independent insurance agent.

Your pharmacy could potentially go bankrupt without the proper coverage. All it takes is one prescription to be filled incorrectly, and you could end up with a hefty lawsuit on your hands. Without the proper liability protection, your business would be stuck paying out of its own pocket for the legal costs.

For the most part, yes, the coverages needed (liability, property insurance, etc.) are similar between bigger and smaller pharmacy businesses. However, larger chains such as CVS, etc. require much higher coverage limits, especially for liability.

Some of the most common protections provided by the right pharmacy insurance are protection against data breaches, protection against costly lawsuits, and protection against business interruptions.

Pharmacist owners need to have coverage for their actions, such as employment practices liability. The pharmacist's employees, however, should be covered by employee dishonesty coverage to protect against incidents of inside crime or professional liability insurance against liability charges, such as professional errors.

Save on Business Insurance

Our independent agents shop around to find you the best coverage.

Why Work with an Independent Insurance Agent?

Independent insurance agents simplify the process by shopping and comparing pharmacy insurance quotes for you. They have access to multiple insurance companies, ultimately finding you the best pharmacy business coverage, accessibility, and competitive pricing while working for you. They'll ensure you walk away with the policy that offers the best possible blend of coverage and cost.

https://www.ibisworld.com/industry-statistics/number-of-businesses/pharmacies-drug-stores-united-states/#:~:text=There%20are%2044%2C900%20Pharmacies%20%26%20Drug,increase%20of%203.5%25%20from%202022.

https://www.ibisworld.com/industry-statistics/employment/pharmacies-drug-stores-united-states/#:~:text=Questions%20Clients%20Ask%20About%20This%20Industry&text=There%20are%201%2C136%2C866%20people%20employed,the%20US%20as%20of%202023.

https://www.zippia.com/advice/us-pharmaceutical-statistics/