Your quote is based on several common factors to give you a clear picture of the cost you can expect, though an independent agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

A farm insurance policy is a very flexible form of protection that can be customized to cover many things, both personal and commercial. It can cover a house, outbuildings and barns, farm equipment, livestock, and liability all related to agricultural and farming activities. For larger agribusinesses, your farm insurance coverage may be extended to include commercial auto and even general business liability, too.

Insurance for livestock is covered under your commercial farm package and can be either added as an endorsement or a separate policy. The policy can provide coverage for the value of your livestock should they need replacing following a covered incident, like: attacked by a predator, caught in a barbwire fence, or stolen.

There are separate policies for your crop insurance. The one that covers multiple claims is called Multiple Peril Crop Insurance, and the other is for hail, specifically called Crop-Hail insurance. Multiple Peril Crop Insurance or MPCI will be the policy that will provide coverage for low yielding crop years due to drought, pests, and so on.

Coverage for your heavy machinery and equipment falls under your farm's package policy. It will typically cover the value of each piece of machinery or equipment that is listed on the policy and will protect against fire, weather, theft, or vandalism that takes place.

Your standard homeowners insurance or commercial insurance policy doesn’t cover farming activities or equipment. So if you own any sort of farm equipment, acreage, or engage in any farming activities, you'll need farm insurance.

Yes. Every state has different laws when it comes to number of employees and when workers' comp is required, but really it's all about protecting you. Farmwork comes with a higher level of risk, so it's important to work with an independent insurance agent who can find a company that specializes in the right workers' comp for the farming sector.

Crop insurance is a very specific type of insurance that’s backed by the federal government. It’s essentially a subsidy that you have to buy that will ensure that you receive a certain amount of income from your crops, even if they fail due to a natural cause, such as flooding or fire. You can’t buy this as part of your farm insurance program. It’s always a separate type of insurance, but it’s available to any farmer.

Agribusinesses are generally large farming operations that may resemble a manufacturing plant, complete with employees and trucks, and they conduct large-scale farming operations. The word farm includes these large agribusinesses, but could also mean small family-run farms or hobby farms, where farming is simply a side activity.

Owning a hobby farm can be a great lifestyle, though it's not exactly a business. But that doesn’t mean that protecting it is any less important. When you begin a hobby farm, coverage may fall under your homeowners insurance policy. However, as you grow and your goals change, you may require further protection, including liability coverage, workers comp, and more.

With access to multiple insurance companies, independent insurance agents are unlike any other type of agent out there. They’ll help find you the best coverage options and most competitive prices, all for free.

FARM INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

Farm insurance is a very unique type of insurance. Because a farm can be both your business and home, farm insurance works like a combo of homeowners, commercial and even liability insurances and includes everything from small family farms and hobby farms, all the way up to large agribusinesses.

Since farm coverage can be fairly complex and requires a thorough understanding of both your farming activities and the insurance options that can cover it, a trusted independent insurance agent is a must-have. We'll help pair you up with an agent who specializes in farm insurance and who can guide you through every step to make sure you are properly covered.

What Does Farm Insurance Cover?

Farm insurance is often a hybrid of personal insurance and commercial insurance. Sometimes it looks a lot like homeowners insurance, while at other times it very closely resembles commercial insurance.

One benefit within farm coverage is that it can be very flexible, tailored, even, to the specific needs of each farm. Most farm insurance policies, however, include dwelling and liability to begin with, adding on additional coverages where they're needed.

Dwelling: AKA, the house. This is typically covered in the same manner as a standard homeowners insurance policy at replacement cost or actual cash value.

Farm liability: This provides liability coverage in case you or your farm are responsible for somebody else’s injuries or property damage. This can also cover multiple locations if your farm uses more than one piece of land.

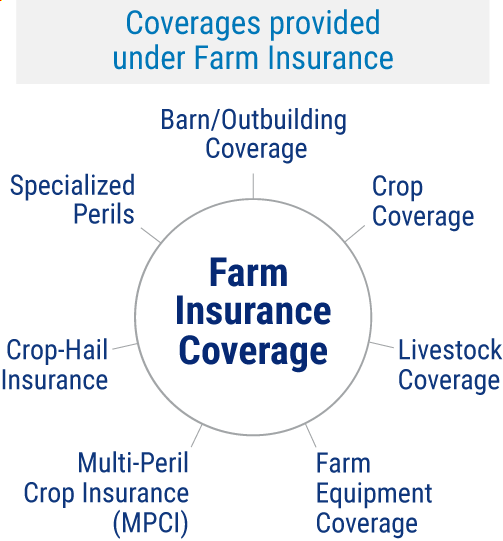

Additional Important Farm Insurance Coverages

After the basics, you and your independent agent will work together to identify your needs and find the right coverages for your farming operation. A few important coverages you should discuss with your agent include:

Barn/outbuilding coverage: Barns and any other outbuildings used for farming are not automatically included in your farm policy and must be listed specifically and covered separately on your policy.

Crop coverage: Traditional crop insurance is not an option on your farm insurance policy, so you’ll need to buy protection separately if you need it. You can, typically, add peak season storage of your crops to your farm insurance policy.

Livestock coverage: You can choose to insure your livestock on either a blanket or a scheduled basis. Blanket coverage means that all of your livestock are covered under one limit, while scheduling lets you pick and choose which livestock you’d like to insure.

Farm equipment coverage: Not automatically included, you’ll need to add coverage to your policy for everything from tractors and harvesters, to farm tools and drones. You can also choose whether you want to have blanket coverage or scheduled coverage.

Multi-peril crop insurance (MPCI): This program offers coverage for inescapable crop loss and covers nearly all available crops against a decrease in crop yield or a significant loss due to natural disasters, disease, and even market disasters.

Specialized peril: Many crop insurance companies also offer coverage for specifically defined perils excluded from an MPCI or crop-hail policy, like: grain fire, rainfall, citrus freeze, and more.

Understanding the Business Side of Farm Insurance

Many larger farms are called agribusinesses and operate similar to fully fledged businesses, and require similar insurance. These larger farm businesses should speak to their independent agent about:

Business income coverage: Helps keep the money coming in if your farm temporarily shuts down due to a covered loss, like a fire or certain natural disasters. This coverage will help you pay bills, employees, and continue operating while your building is repaired.

Workers’ compensation: Very few states require farms or agribusinesses to have workers’ compensation, though it can really help provide valuable insurance coverage if an employee gets hurt on the job in a profession that does carry quite a bit of risk.

Commercial auto: If you’re hauling your grain or livestock, you'll need a commercial auto insurance policy. Even if you just use your pickup truck occasionally on the farm, your insurance company may rate it as a farm-use only vehicle, which typically has better rates.

How Much Does Farm Insurance Cost?

If you have an agribusiness, you may already know that the cost of insurance can be pricey. So how do you find the right cost without sacrificing your coverage? Your first step is to understand the factors that affect your premium cost the most:

Acreage: How much land you have will affect your cost. The more you have to insure, the more premium you will pay.

Barns and buildings: The number of barns and other structures you have, in addition to their size and quality, will factor into your cost.

Production: What you grow, harvest, produce, and sell will also impact premiums.

Farmhouse: Size, quality, and features of your home on your agribusiness will also impact your pricing.

Equipment and machinery: Both motorized and unmotorized property like tractors, threshers, and other equipment will need insuring, and the replacement cost on some of those pieces could be high, which will impact rates.

Workers: The farmhands and workers of any kind that you hire to run your farm will impact rates because you'll not only have more liability employing people, but you'll also need to add a workers' compensation policy.

Average farm insurance costs

In general, it's safe to say that under normal circumstances, a small farm will cost you between $50 and $100 per month to insure.

Finding the Best Discounts and Savings on Farm Insurance

Fortunately for farmers, you can find farm insurance discounts nearly anywhere you look. Each insurer offers different cost-saving discounts and qualifications, but an independent agent can help you zero-in on the right discounts for you, starting with the following:

Good credit discount: Depending on the state you live in, your insurance company may run your credit as part of your application. People with good credit generally receive a discount on their premiums.

Multi-policy discount: Most insurance companies allow for a multi-policy discount on farm policies, which means you could save money by having both your farm and your personal auto with the same insurer.

Alarm system discount: Similar to homeowners insurance, this reduces your premium if you have a central station alarm system connected to your house.

Roof or structural discount: This discount may be more of a rating adjustment than a technical discount, but if you have a new roof, particularly if it’s metal, or if your home is built of a strong material such as brick, you may get lower rates.

Farm credit discount: Potentially the largest discount, farm insurance companies have the ability to put credit on a policy, which reduces the premiums that you pay. Speak with an independent insurance agent to see if your farm qualifies for at least a little bit of credit.

Your Independent Insurance Agent Has Your Answers

Whatever you need, your agent has your back. With a brief intro into the terms, discounts and process of your farm insurance, you know the kinds of questions to be asking. Your agent will ask you all about your farm, its use and your goals and help find the perfect blend of coverage at the right cost for you.

Best Farm Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What Our Customers Are Saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.