First-to-Die Insurance

(A quick guide on everything you need to know)

Christine Lacagnina has written thousands of insurance-based articles for TrustedChoice.com by authoring consumable, understandable content.

Neel Lane is an independent contract paralegal who specializes in Medicaid and VA benefits. He helps people access and maximize the benefits that they're entitled to. He has over 30 years of experience in this area.

There's no question that marriage teaches you how to behave as a team. The two of you do everything together, from taxes to coordinating your outfits for summer picnics. So it only seems logical that the two of you get your insurance together too. And we’re here to help.

Our independent insurance agents are always ready to find the right solution to help secure your financial future as a couple, no matter who ends up checking out first. They’ll walk you through the ins and outs of a first-to-die joint life insurance policy and deliver the best options straight to you.

Before we discuss joint life insurance, here are some statistics to think about:

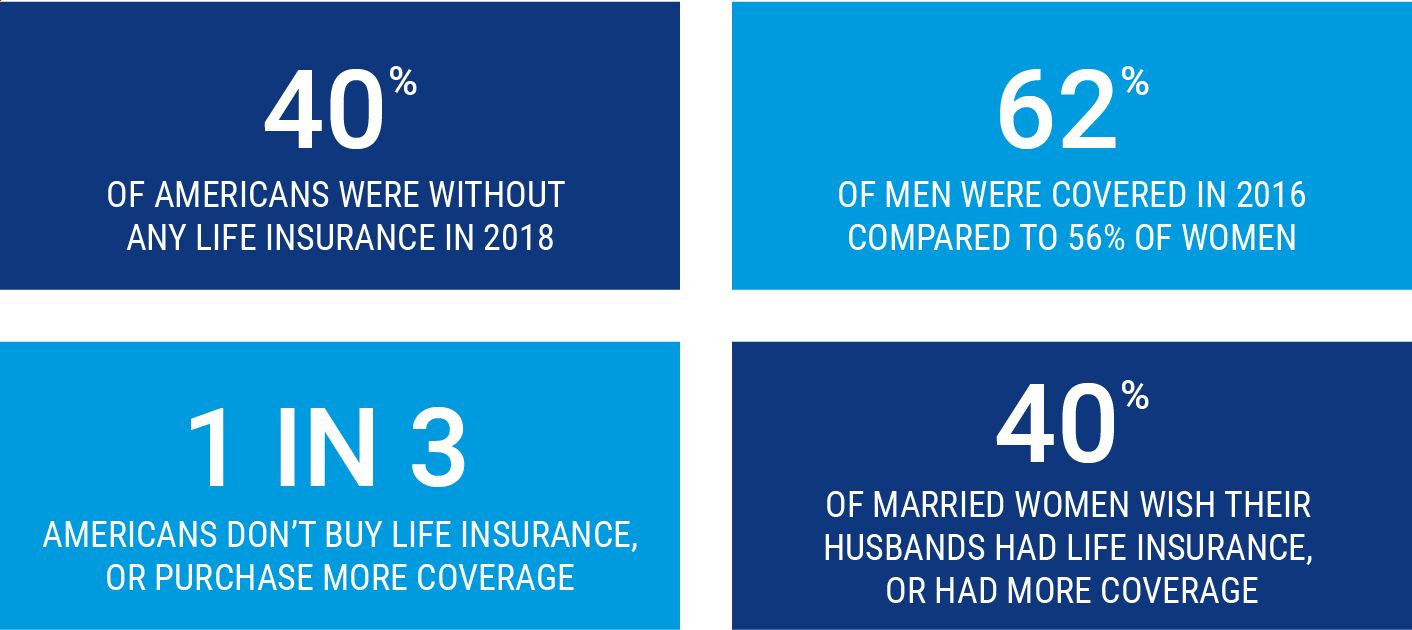

- In 2018, 40% of Americans were without any life insurance.

- Men are more likely than women to own life insurance. In 2016, 62% of men were covered compared to 56% of women.

- Many uninsured Americans think that life insurance costs two or three times more than it actually does.

- Many insured Americans believe that they do not have enough life insurance.

- One in three Americans don't buy life insurance, or purchase more coverage, because they don't like thinking about death.

- Forty percent of married women wish their husbands had life insurance, or had more coverage.

What Is Joint Life Insurance?

Quite simply, it’s for the couple not the individual. When a couple shares joint life insurance, they only have one plan and therefore, one ultimate payout.

In the case of a first-to-die policy, the payout will come when — you guessed it — the first partner dies. The other option would be second-to-die insurance where the payout comes after the second passes.

Like a traditional life insurance policy, first-to-die insurance helps “replace” a deceased partner's income after they're gone and is a popular option for many because it sets up a fund for current and future family expenses.

The last spouse standing can use it to tackle the children's massive college tuition payments or pay off outstanding debts, and it can help them maintain the same lifestyle.

Save on Life Insurance

Our independent agents shop around to find you the best coverage.

What Are the Advantages of a First-to-Die Policy?

For starters, it could end up being cheaper to go for a joint life insurance policy rather than two separate policies. Since the insurance company only has to write one policy for both of you, they face less risk and therefore your premium ends up being lower. Also, you and your partner will only have one premium payment instead of two.

First-to-die policies can really benefit the surviving spouse because they'll receive a payout when their partner dies. The surviving spouse will also have access to the plan's benefits sooner than they would have been able to with two separate life insurance policies. This will establish greater financial security for the surviving spouse.

Are There Any Disadvantages of a First-to-Die Policy?

If a couple separates, it may not be as easy to split the insurance policy as if they were written separately.

Separating a joint policy is often complicated, but asking for an insurance rider — which could amend the coverage to two separate plans in the event of a separation — could prevent issues. Ask your agent about it before you write your check.

Additionally, there might not be sufficient funds to support any children, should both partners die. No benefits will be left to the kids when the last spouse dies.

The surviving spouse may have to buy a new life insurance policy, or start some hardcore budgeting in order to provide for their kids. In such a case, a first-to-die policy might not have been worth it.

What Is the Purpose of a First-to-Die Policy?

Say a married couple own a house, make nearly the same salary, and don't have kids. Their debt will be based on two separate incomes. If one of them dies prematurely, the remaining spouse now has to take on the same financial obligation on half the income. Having a first-to-die policy would avoid this setback, for a small premium.

First-to-die policies are also structured well for business partners who have shared financial obligations. If one partner unexpectedly dies, the surviving partner shouldn't have to shut the business down.

As far as financial benefits, with only one policy fee and one death benefit to be responsible for, a first-to-die policy could have huge potential for cost savings.

Save on Life Insurance

Our independent agents shop around to find you the best coverage.

What's So Great about an Independent Agent?

Insurance policies can be tricky, and let's face it, browsing and discussing first-to-die life insurance policies can be downright depressing. Independent agents exist to simplify the process and save you some grief.

Independent agents are there to make sure you get the absolute best deal, and the one that meets your unique needs. They shop and compare insurance quotes for you, and they'll break down all the jargon so that you understand exactly what you're getting.

Finding and Comparing First-to-Die Insurance Quotes

Our expert insurance agents will review your needs and help you evaluate which type of first-to-die joint life insurance makes the most sense for you.

They'll also compare policies and quotes from multiple insurance companies to make sure you have the best protection out there. They'll hook you up in a comprehensive and affordable way.

- https://www.investopedia.com/terms/r/rider.asp

- www.limra.com