Vocational Rehabilitation

(And why every workers' compensation policy needs it)

Candace Jenkins is a licensed insurance advisor with over a decade of experience. She is also a writer and loves to write on all things insurance. Candace writes for TrustedChoice.com on a continuous basis and is here with the facts about all your insurance inquiries.

Understanding all aspects of a workers' compensation insurance policy including vocational rehabilitation is essential to you, your business, and your employees.

An independent insurance agent is a key advisor for every business owner when it comes to workers' compensation insurance and how vocational rehabilitation works. Having the agent in your corner with the best options is a pretty good place to start.

What Is Workers' Compensation Insurance?

First things first, you need to know what workers' compensation insurance is before you can know the laws that govern it. Workers' compensation insurance is an insurance policy taken out by an employer or independent contractor that will help pay for medical expenses of an injury or illness that occurred while working or as a result of an employee's job.

This policy will also pay for partial wages, usually up to two-thirds, for any employee, included owners, or independent contractors while they're recovering. An independent insurance agent is the perfect resource to have when it comes to knowing the ins and outs of workers' compensation coverage.

What Is Vocational Rehabilitation Coverage?

Vocational rehabilitation is a workers' compensation benefit that can include tuition reimbursement or training to prepare you for another career. Vocational rehabilitation coverage can be used if your employee becomes incapable of doing their regular job duties because of a permanent restriction, either mental or physical, due to a work-related injury or illness.

In some cases, you as the employer may be required to provide vocational rehabilitation to help your employee or former employee back to gainful employment. Your employee still may be able to stay with you as an employer but receive training through vocational rehabilitation coverage to do something different within your organization.

What Does Vocational Rehabilitation Coverage Cover, Exactly?

There are a number of different items that vocational rehabilitation benefits cover. And the ultimate goal of this coverage is to get each employee as closely back to like, kind, and quality as possible, meaning gainfully employed in their current state.

Some vocational rehabilitation expenses it may cover are as follows:

- Schooling: Tuition reimbursement to learn a new skill set may be covered.

- Training: If there is any licensing, certification, or paid training needed to get an employee back to gainful employment, this would fall in line with coverages.

- Job placement: Coverage can extend to helping an employee find a new job, if applicable.

- Resume writing: Assistance with writing an updated resume can also be under the lists of coverages.

- Career assessment: Assessing where an injured employee goes from here can be tricky, so making sure all skills new and old are assessed is crucial.

- Career counseling: Figuring out where an employee fits in after an injury or illness can be daunting, so having a third-party non-biased counselor to help facilitate the process is also a coverage provided.

Save on Workers' Comp Insurance

Our independent agents shop around to find you the best coverage.

What Is Not Covered?

By now you should have a pretty good understanding of what a vocational rehabilitation benefit will cover. What you need to know is what it's not going to cover.

What's not covered under vocational rehabilitation benefits:

- Disability: This is through the other coverages on a workers' compensation policy.

- Medical expenses: Again, this is another coverage on a workers' compensation policy.

Cost of Workers' Compensation and Vocational Rehabilitation Coverage

Policy costs vary. It's a vast numbers game when it comes to risk factors and industry types concerning workers' compensation insurance. The only true way to know is to have your agent run the numbers on your business and its specifics. While it's near impossible to know what your individual workers' compensation premium will be, here are some determining factors you can look out for.

Workers' compensation price-determining factors:

- Industry: This plays a big part in the cost of your workers' compensation premium. The riskier your business, the higher your premiums will be.

- Number of employees: This determines how much your rates will increase. More people equal more money.

- Gross annual payroll per employee type: Each employee is given a classification code that classifies their job duties and then charges the premium according to how risky or not risky their tasks are. The amount of money you pay them will determine the amount of premium per classification code. The more payroll, the more premium you pay.

- Experience modification rating: If your business has had workers' compensation insurance for a total of three years or more, and you are paying over $5,000 in annual premium, then you'll be assigned an experience modification rating, aka "mod." This mod will adjust throughout the years depending on the number, length, and frequency of claims turned in. The better the mod, the better rate you will receive. It's kind of like a credit score for your workers' compensation policy.

The cost of vocational rehabilitation within a workers' compensation policy is included in the premiums and is not a separate or individual coverage. Typically, vocational rehabilitation is used by the insurance company when they are trying to make sure the injured or ill employee is able to continue working. If there is a way for said employee to still work with their injury or illness, and gainfully at that, then the insurance company will find a way through the vocational rehabilitation benefits.

What Is the Benefit of Having Enough Vocational Rehabilitation Coverage?

The benefits of good coverage far outweigh the costs involved. Having a knowledgeable independent insurance agent who can properly advise on how much coverage you should obtain will determine how much coverage your injured employees can get for medical expenses as well as for vocational rehabilitation.

Think about it, if your injured or ill employee is disabled now because of a workplace event that could have been avoided by proper safety precautions and risk management, then who are they more likely to come after when they are out of a job permanently? Best play it safe and discuss proper workers' compensation coverage all around.

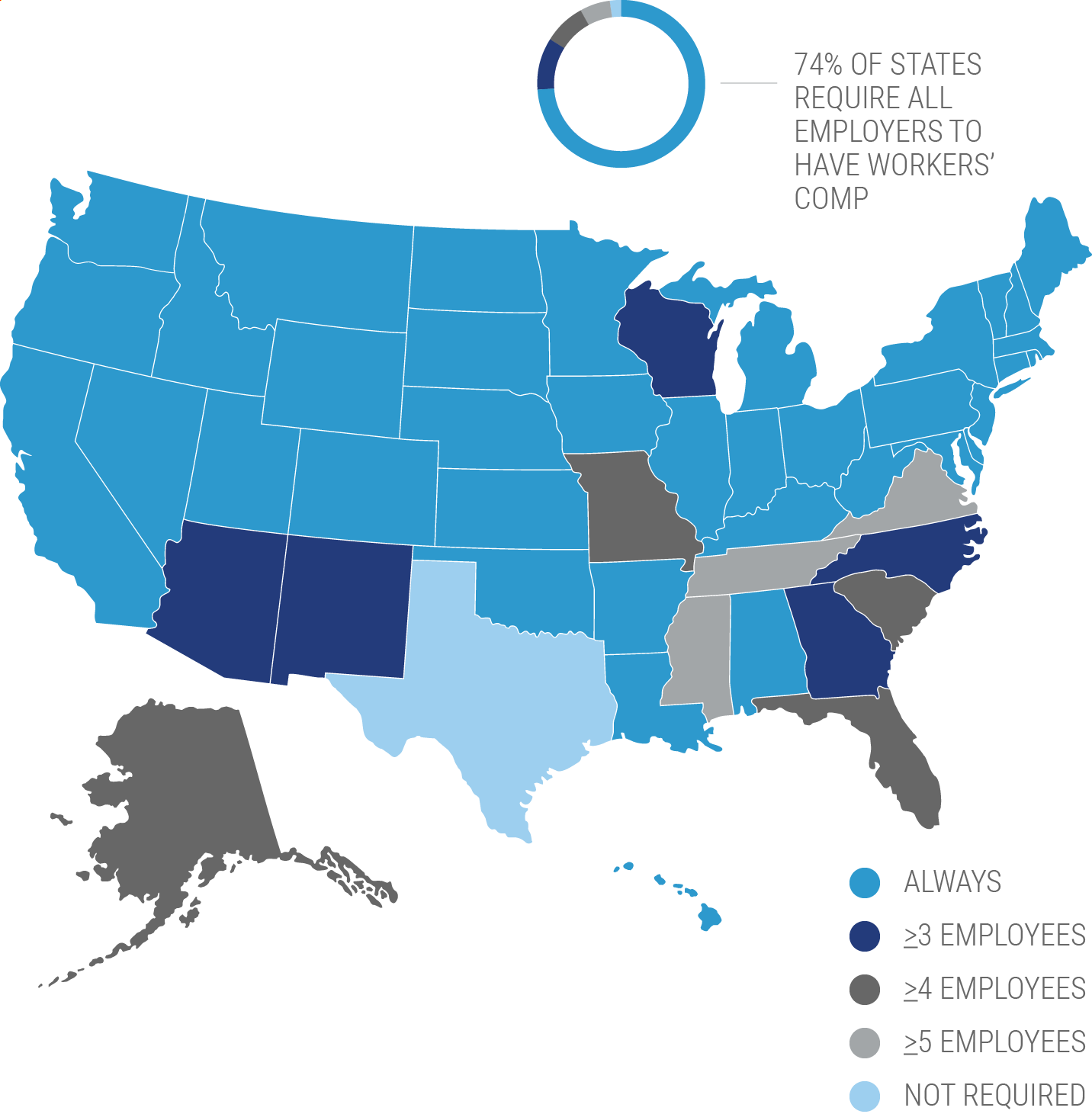

Is Vocational Rehabiliation Coverage State-Specific?

Each state has its own rules when it comes to workers' compensation insurance because each state {except for Texas} has mandated workers' compensation coverage in some form or another. Vocational rehabilitation coverage can be state-mandated and state-funded because the state and commissioner are all about making sure the consumer and employee are rightfully treated as they should be.

Usually, there are no additional forms or endorsement add-ons associated with vocational rehabilitation coverage through the insurance provider because it's an included coverage within the workers' compensation policy. But to be ultra sure, checking with your agent on your state specifics will set you on the right track.

Benefits of an Independent Insurance Agent

Independent insurance agents have access to multiple insurance companies, ultimately finding you the best coverage, accessibility, and competitive pricing while working for you. And as your company grows and your needs change, they'll be there to help you adjust your coverage, up or down, to make sure you're properly protected without overpaying. Find an independent insurance agent in your community here.