Directors and Officers Insurance

In short, this coverage seriously ramps up your existing business or nonprofit insurance.

Christine Lacagnina has written thousands of insurance-based articles for TrustedChoice.com by authoring consumable, understandable content.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

Whether a business is for-profit or nonprofit, it's vulnerable to all kinds of risks, including legal troubles. Directors and officers insurance is a critically important tool to keep your business or nonprofit thriving for years to come. It shields your organization from hefty lawsuit costs and helps your board make innovative decisions.

An independent insurance agent can help you find the right type of directors and officers insurance for your organization. They'll also get you equipped with all the coverage you need long before you ever need to file a claim. But first, let's take a deep dive into directors and officers insurance.

Save on Business Insurance

Our independent agents shop around to find you the best coverage.

What Is Directors and Officers Insurance?

Directors and officers liability insurance covers legal fees and damages in case a lawsuit is filed against an organization’s board members, officers or other leadership. It’s purchased by an organization on behalf of those leaders, and kicks in when a lawsuit gets filed against the board.

The insurance company pays for legal representation and damages up to the insurance policy’s cap. Coverage limits are usually $5 million or $10 million.

Coverage protects the assets of corporate directors and officers (and their spouses) if they get sued by any of the following:

- Employees

- Vendors

- Competitors

- Investors

- Customers

- Other third parties

Covered lawsuits include those filed with claims of wrongful acts in managing a company. Many insurance companies also provide legal services like free advice to help avoid claims. An independent insurance agent can help you find the right directors and officers insurance for your organization.

Why Is Directors and Officers Insurance Important?

Directors and officers insurance helps fulfill indemnification clauses, or agreements that an organization will pay for any legal fees and damages incurred by a board member or high-level employee. The clause is usually part of a contract created before influential members are hired.

To fulfill this clause, a directors and officers insurance policy can be paid directly to the group dealing with the legal challenge. It can also be paid out to the organization, which in turn pays for the legal costs of its board members and employees.

Who Needs Directors and Officers Insurance?

Directors and officers insurance is important to get as soon as a nonprofit or business develops a leadership structure, especially one that includes a board of directors. Lawsuits may arise from stockholders who are angry about plummeting prices, employees who feel their benefits were mismanaged, or victims of assault by a member of the organization's board.

Coverage can be purchased for nonprofits and for-profit businesses. Churches and other religious organizations also sometimes buy this insurance. The reasons organizations use their coverage varies widely.

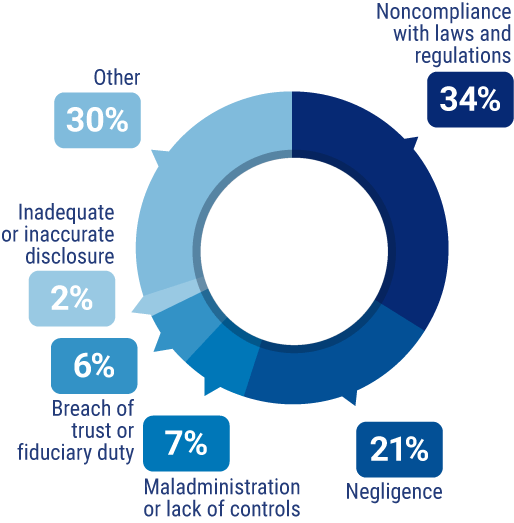

Top reasons companies filed directors and officers insurance claims in recent years:

- Noncompliance with laws and regulations (34%)

- Negligence (21%)

- Maladministration or lack of controls (7%)

- Breach of trust or fiduciary duty (6%)

- Inadequate or inaccurate disclosure (2%)

- Other (30%)

If board members mismanage employee benefits, that can be a cause for a directors and officers insurance claim. Even a small misstep by a CEO or board member can cause major headaches for an organization. Directors and officers insurance is there to cover any legal fallout.

Who Sells Directors and Officers Insurance?

Directors and officers insurance is available from many different insurance companies, and the best way to find the right carrier for you is through working with an independent insurance agent. They know which insurance companies to recommend to meet your needs, and can provide informed suggestions based on company reliability, rates, and more.

While many insurance companies could create a directors and officers insurance policy for you, finding coverage could also depend on the area you live in. Here are a few of the top companies for directors and officers coverage.

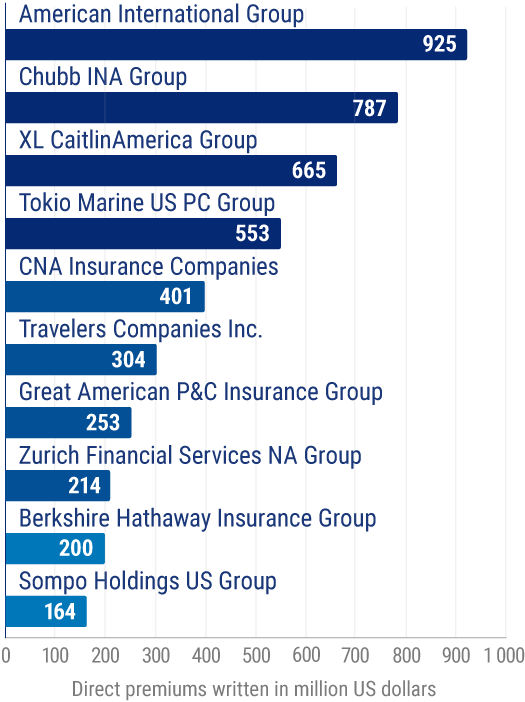

Leading writers of D&O insurance in the US in 2017, by premiums

Recent leading directors and officers insurance companies include American International Group, Chubb, Travelers and W.R. Berkley . An independent insurance agent can help you decide if one of these insurance companies is the best carrier to meet your organization's needs.

Save on Business Insurance

Our independent agents shop around to find you the best coverage.

Common Directors and Officers Insurance Claims

Directors and officers insurance protects against many types of lawsuits filed against the board of an organization. Some of the most common directors and officers insurance claims are:

- Breach of fiduciary duty

- Failure to comply with workplace laws

- Theft of intellectual property

- Misrepresentation

An independent insurance agent can provide even more examples of common claims filed under directors and officers insurance and how this important coverage can benefit your specific organization.

What Doesn't Directors and Officers Insurance Cover?

While directors and officers insurance provides a lot of important coverage for nonprofits and for-profit organizations alike, it also comes with its own set of exclusions. Some of the most common coverage exclusions are:

- Personal profiting

- Fraud

- Illegal compensation exclusions

- Accounting of profits

- Late claim notice

- Bodily injury and property damage

- Criminal or malicious acts

Claims of bodily injury and personal property damage are covered by a business insurance policy's commercial general liability coverage section. Crime insurance is a policy designed to cover against criminal acts and dishonesty by employees. An independent insurance agent can help you find any additional coverages your organization requires.

How Much Does Directors and Officers Insurance Cost?

The cost of your directors and officers insurance will depend on several factors. In general, low-risk organizations might pay only $250 annually for their coverage, while corporate giants might pay more than $10,000 a year for $1 million worth of protection. The national average cost of this coverage amount is $600 annually.

| Business Type | Annual Coverage | Protection |

| Low-Risk Organization | $250 | $1 million |

| Corporate Giant | $10,000 | $1 million |

| National Average | $600 | $1 million |

Factors determining the cost of directors and officers insurance include:

- Size of the organization

- Annual revenue of the organization

- Risk level of the organization

- Location of the organization

An independent insurance agent can help find exact directors and officers insurance quotes for your area and specific organization.

Frequently Asked Questions about Directors and Officers Insurance

No, directors and officers insurance is designed to protect organizations against claims filed against their board of directors or leadership panel. Professional liability insurance protects organizations against claims of damage or injury caused by the work performed by the company.

Yes, board members and officers of nonprofits can be held personally liable for the organization, meaning their personal assets, and their spouses' assets, are at risk. That's why having the right directors and officers insurance is critical, to protect these assets.

A director or officer of a nonprofit organization often can be held personally liable for their actions. In a for-profit business environment, however, often these members cannot be held personally liable.

Yes, directors and officers insurance typically comes with a deductible. Working with an independent insurance agent is a great way to select a policy that works best for you, including its deductible and coverage amounts.

Volunteer immunity law details vary from state to state. To be sure of whether or not you're covered against claims while serving on a nonprofit board, double-check your local volunteer immunity laws ahead of time.

Save on Business Insurance

Our independent agents shop around to find you the best coverage.

Why Are Independent Insurance Agents Awesome?

It’s simple. Independent insurance agents simplify the process by shopping and comparing insurance quotes for you. Not only that, but they’ll also cut the jargon and clarify the fine print, so you know exactly what you’re getting.

There’s no business too small for our gifted independent insurance agents. They have access to multiple insurance companies, ultimately finding you the best directors and officers coverage, accessibility, and competitive pricing while working for you.

https://www.statista.com/statistics/947791/top-writers-of-directors-officers-insurance-by-premiums/#:~:text=American%20International%20Group%20was%20the,approximately%20925%20million%20U.S.%20dollars

https://smallbusiness.chron.com/can-officer-corporation-held-personally-liable-54650.html#:~:text=Limited%20liability%20protects%20shareholders%2C%20directors,cannot%20be%20held%20personally%20liable.

https://www.nolo.com/legal-encyclopedia/nonprofit-directors-personal-liability-32357.html