Car Claims FAQ

Get your questions answered by the pros

More than seven million people visit our site every year looking for unbiased information about insurance and other related topics. And with great readership comes great responsibility, which means we’re dedicated to providing honest and accurate information.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

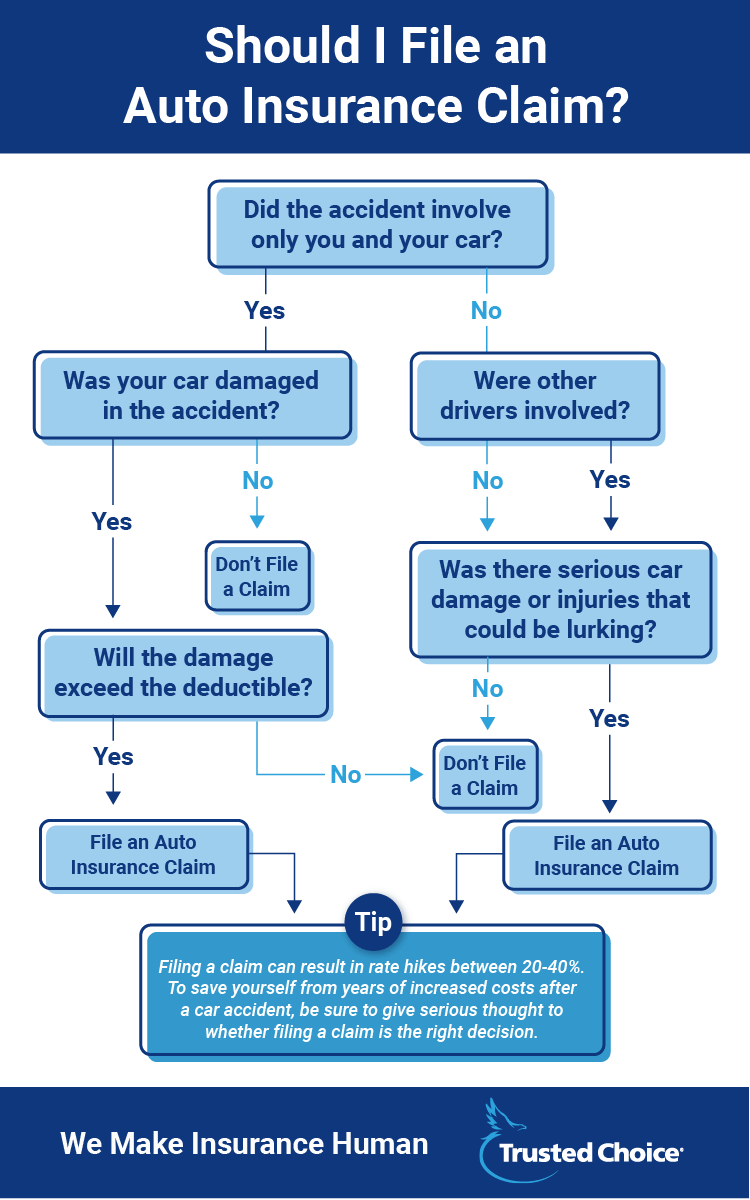

Q. When Should I File an Auto Insurance Claim?

Q. How Do I File an Auto Insurance Claim?

Q. How Does My Deductible Work?

Q. What If I Was in an Accident?

Q. What If the Accident Was a Hit-and-Run?

Q. What If the Other Driver Is Uninsured?

Q. Do I Get a Rental Car While Mine Is Being Repaired?

Q. What If Someone Else Is Driving My Car and Gets in an Accident?

Q. When Is a Car Considered "Totaled"?

Q. Will My Car Insurance Rates Go Up If I File a Claim?

Q. What If I Have More Questions?

Car accidents are a lot like high school crushes. They can come out of nowhere, some you’ll completely forget about, and others may leave you an emotional wreck for a long time. The key, in both cases, is to make sure you handle the incident right from the start.

And that’s why we’ve put together this little Q&A, to help you through the whole auto insurance claim process and get you back on the road.

If there is anything below that does not apply to you, your local independent insurance agent is an absolute pro who would be happy to explain your car insurance coverage, the claims process, and pretty much anything else insurance-related you can think of.

If you find yourself needing to learn more about car insurance claims, click here and find out more information.

When Should I File an Auto Insurance Claim?

Immediately. Well, once you’re in a safe place and your heart rate has steadied, at least. If you wait too long, it could lead to your insurer denying your claim. Plus, don’t you just want to get your life back to normal? So the sooner the better.

Now, if it was just a little fender bender, or someone rummaged through your car and emptied out your coin tray—you might not want to file a claim. Think about it.

If you’ve got a $500 deductible and the damage or loss totals only $550, do you really want to risk your premiums increasing to get that extra $50 after you pay the deductible?

Whenever an accident or theft occurs, ask yourself if filing a claim is worth it. If the out-of-pocket cost without insurance is minor, we say skip the claim. But it’s your call.

How Do I File an Auto Insurance Claim?

So you’ve carefully thought through your decision about whether to file a claim. Now what? If you’ve decided that filing is in your best interest you can do so by phone, in person or online. Some insurance companies even have a mobile app that you can use to begin the claims process. How slick is that?

When you contact your insurance company, make sure you have the following information ready:

- Your car insurance policy number

- The date and location of the incident

- The names, addresses and insurance information of all others involved in the incident

- A description of what happened

- If applicable, the name of the police department that responded

- If applicable, the police report number or a copy of the police report

Save on Car Insurance

Our independent agents shop around to find you the best coverage.

How Does My Deductible Work?

Your deductible is the amount that you are responsible for when you file a claim. Car insurance deductibles typically range from $500 to $1,000, though they can be higher or lower .

If your deductible is $500 and your damages come to $15,000, your insurance company will reimburse you $14,500. Note that you only need to pay the deductible if you are the at-fault driver.

What If My Car Was Stolen?

First and foremost, does your insurance policy have comprehensive coverage? If it does, good. If it doesn’t, uh-oh. Regardless of your coverage, your first step is to call the police. They’ll send an officer to the scene, ask you a bunch of questions and fill out a report. Don’t throw that report in the recycling, you’ll need it when you call your insurer.

What If I Was in an Accident?

Priority number one: safety. Is everyone okay? If there are injuries, call 911 immediately so that medical and law enforcement professionals can help.

If the vehicles involved in the accident are a hazard to other drivers, take pictures of the scene from multiple angles and then move the vehicles out of the way if you can. If you can’t, don’t fret, leave them where they are and a tow truck can help you out when it arrives.

Exchange super-detailed information with the other drivers, including names, addresses, and insurance information. BUT, DO NOT admit fault or apologize for what happened. Determining who’s at-fault is up to the authorities at the scene.

What If the Accident Was a Hit-and-Run?

If the other driver flees the scene without giving you their information, wait for the police to arrive and then explain everything that happened. Then call your insurance company and they’ll take you through the next steps.

Save on Car Insurance

Our independent agents shop around to find you the best coverage.

What If the Other Driver Is Uninsured?

If your policy includes uninsured motorist coverage (which is required in some states but optional in others), then you don’t need to worry. Likewise, if your policy includes collision coverage, you may still be covered.

If you do not have uninsured motorist insurance or collision insurance, you will probably have to take the at-fault driver to court. Now, be aware that collecting the money owed to you can be a long, drawn-out process, but it’ll totally be worth it in the end.

Do I Get a Rental Car While Mine Is Being Repaired?

This depends entirely on the policy you have. Policies that do include rental reimbursement coverage will cover rental fees while your car is being repaired. If your policy doesn’t provide coverage, you will have to pay the cost out of pocket.

If you rent your vehicle through an approved provider, they can bill your insurance company directly so you have no upfront costs. But if you choose to go through an unapproved rental company with way cooler cars, you’ll need to pay the costs upfront and then submit a claim to be reimbursed.

What If Someone Else Is Driving My Car and Gets in an Accident?

With car insurance, the coverage is attached to the vehicle, not the driver, so your auto insurance would cover the accident. If there are liability costs that exceed your policy limits, however, your friend’s insurance policy can step in to cover the difference. After all, isn’t that what friends are for?

Save on Car Insurance

Our independent agents shop around to find you the best coverage.

When Is a Car Considered "Totaled"?

The definition of what is considered “totaled” varies from state to state. But, in most states, if the damage exceeds 75% of the vehicle’s value, it’s typically considered a total loss. Time to go shopping!

If your car is totaled, you can only be reimbursed for its actual cash value at the time of the accident. Keep in mind that new cars depreciate at a faster rate than older cars—they just don’t make ‘em like they used to.

If your car is only a couple of years old and you still have several years of payments left on your auto loan, it is likely that your vehicle’s actual cash value will be lower than what you still owe on it. So unless you purchased gap insurance with your vehicle, you may be making payments on a car you no longer own.

Will My Car Insurance Rates Go Up If I File a Claim?

This depends on your insurance company. Some companies offer accident forgiveness for your first accident. In most cases, however, an accident will increase your risk profile and can result in higher auto insurance rates—sorry.

What If I Have More Questions?

That’s a pretty safe bet—we can’t cover every unique car insurance claim question out there. But your local independent insurance agent is an absolute pro who would be happy to explain your car insurance coverage, the claims process, and pretty much anything else insurance-related you can think of.